Below are key European banking risk monitors, which are included as part of Josh Steiner and the Financial team's "Monday Morning Risk Monitor". If you'd like to receive the work of the Financials team or request a trial please email

------

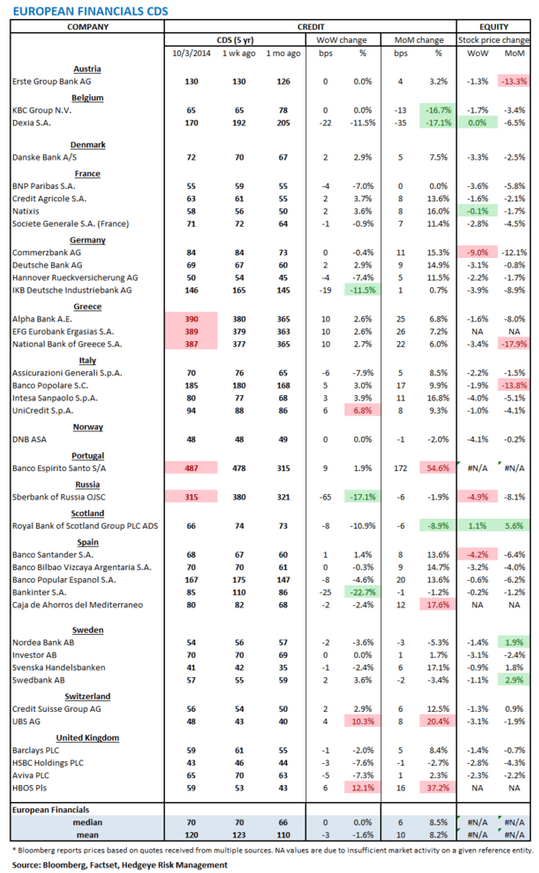

European Financial CDS - Swaps were mixed in Europe last week, but little changed overall. We've been keeping a close eye on Sberbank as our proxy for overall geopolitical risk. After rising steadily for several weeks, it cooled off notably this past week dropping 65 bps w/w to 315 bps.

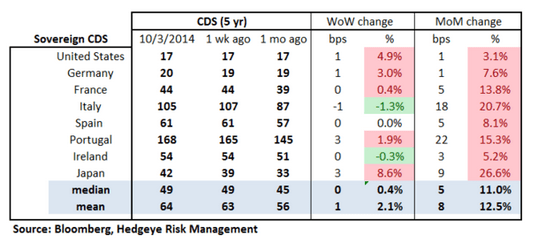

Sovereign CDS – Sovereign swaps were little changed on the week with most countries moving 0-1 bps. Portugal and Japan were the outliers at +3 bps each.

Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread tightened by 2 bps to 11 bps.

Matthew Hedrick

Associate

Ben Ryan

Analyst