|

Below is a complimentary excerpt from a research note written today by Hedgeye Energy Policy analyst Joe McMonigle. Email sales@hedgeye.com for access to our institutional research. |

OPEC+ Cuts Start & Demand Uptick Signs Support Price. Big Red Engine Light Warning on WTI Remains.

Both Brent and WTI oil prices were on the rise Tuesday in large part due to restarting OPEC+ production cuts and reopening economic activity in some US states and countries.

President Trump and OPEC are working together again to support higher oil prices. Saudi Arabia led unprecedented OPEC+ cuts of 9.7 million barrels per day (b/d) that took effect on May 1, and we see a possibility of additional measures at the June 10 OPEC meeting.

For his part, Trump is shifting from epidemics to economics, and more specifically, the Cheerleader-in-Chief for reopening the US economy.

On Tuesday, Trump hailed the double-digit hike in prices in a tweet:

Trump is referencing the 27 states that have begun to reopen some parts of their economies and ease lockdown orders. Governing.com has an excellent summary of state’s specific reopening orders and it is updated daily.

Since the March national emergency order, transportation fuel demand has crashed in the US and around the world. According to the US Energy Information Administration (EIA), gasoline consumption declined 5.1 million barrels per day (b/d) in the week ending April 3 - marking the lowest amount of gasoline supplied since EIA began tracking the data in 1991.

However, there are signs that we may have possibly seen the bottom in the demand declines at least for gasoline. Last week’s EIA Weekly Petroleum Status Report for the week ending April 24 showed refinery runs increased slightly by about 300,000 b/d. The market will be closely watching for a trend in uptick demand EIA releases data Wednesday on refinery run and storage levels for the week ending May 1.

While signs of an uptick in demand are welcome news for oil prices this week, there remains a mountain to climb to regain normal levels of demand that may be months or even years away. See EIA chart showing refinery runs far below the normal range.

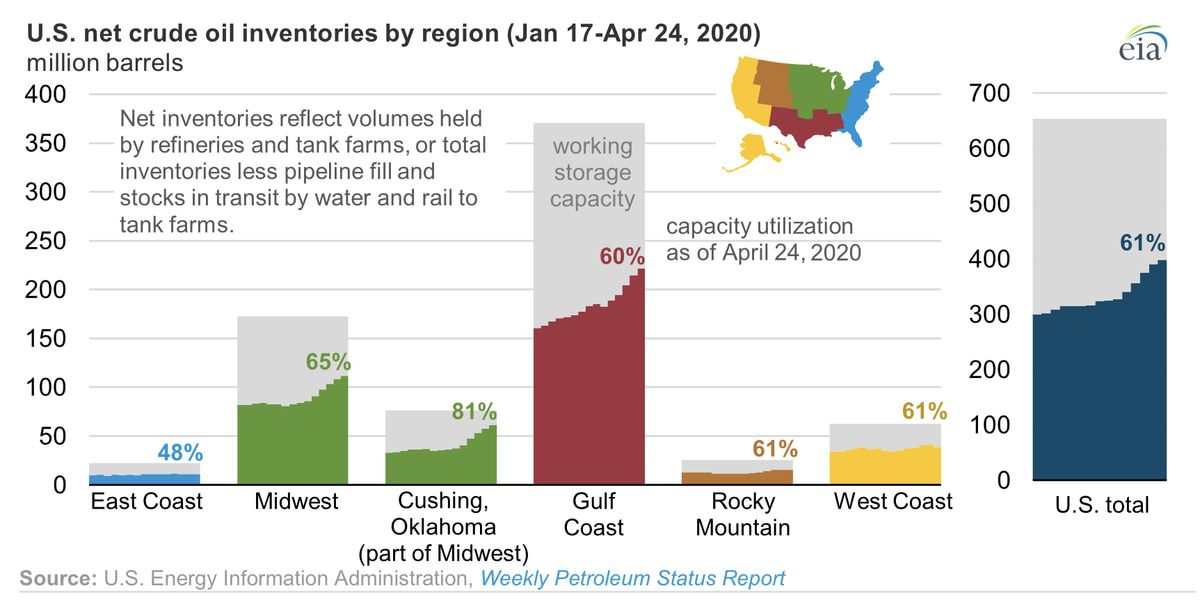

WTI was up 20 percent Tuesday for the June contract but we see a big red engine warning light for WTI prices short term. Because WTI contracts require physical deliveries of crude by June 30, prices should head lower as rollovers to the July contract begin and the contract closes on May 19. We think it’s unlikely there will be another repeat of negative prices but weakness in WTI will continue due to limited Cushing storage with inventories near full tanks.

Based on fundamentals and the unique physical delivery requirement for WTI, we see oil prices lower on the June contract over the next two weeks. Moreover, due to Quad4 deflation risk, Hedgeye’s Macro team also sees more downside to WTI with the low-end of the risk range at $9.75/barrel.

Brent prices settled near $31 on Tuesday and will enjoy the benefits of upticks in demand as well as the OPEC+ production cuts now also being augmented by non-OPEC private sector producers.

The Trump Administration is now putting greater focus on the economy at least from a messaging standpoint. Instead of reading statistics of new COVID-19 cases, the White House will begin highlighting successful measures to reopen the economy while simultaneously promoting social distancing.

More states will continue to follow with easing restrictions. While Governor Cuomo in New York is taking the most cautious approach in the country, he has also begun to describe metrics for reopening the state’s economy. There is a northeast regional reopening strategy taking form that will likely see parallel timelines in New York, New Jersey, Connecticut and perhaps other states that could begin in late May or early June. We think this northeast US reopening may serve as another catalyst for an increase in oil prices similar to today.

Saudi Arabia is optimistic that oil prices will steadily rise over the coming months. Based on our reporting, we believe senior Saudi officials see Brent prices in the mid-30s range in May and June and rising to around $40 by the end of the summer and early September.

The optimistic view is based on the record OPEC+ cuts that started this month as well as announced lower production levels in the US and other key non-OPEC producing countries. According to EIA data last week, US production is down 1 million b/d over the last six weeks and likely to fall much further and faster closer to 3 million b/d.

Adding these non-OPEC production cuts to the OPEC+ cuts, we think total production cuts are closer to 15 million b/d and approaching the 20 million b/d goal announced at the OPEC+/G20 meetings. The market was skeptical at the time about these numbers but now it is hard to ignore. April appears to have been the bottom in the demand decline from COVID-19 and production cuts are catching up.

OPEC will meet again on June 10 by videoconference to review the compliance and the oil market. While it will likely be too early to assess compliance after just one month but we believe the lack of demand will ensure strong compliance to production cut levels.

The OPEC+ cuts of 9.7 million b/d for May and June under the agreement will be reduced to 7.7 million b/d for the rest of 2020 and then 5.8 million b/d starting January 2021 to April 30, 2022.

We believe there is a possibility of stronger OPEC+ action if necessary at the June meeting. One option that we are hearing is under consideration is just extending the highest level of cut at 9.7 million b/d for the rest of the 2020 (instead of the current plan to reduce cuts to 7.7 million b/d starting in July). Not only would this be another welcome sign by oil markets, but it would also help to reduce global crude inventories faster than anticipated.

Another positive factor for prices this week is that, with the exception of Cushing, global storage levels appear to be slowing. Even in the US, total storage capacity reported by EIA is only about 60 percent (as of April 24).