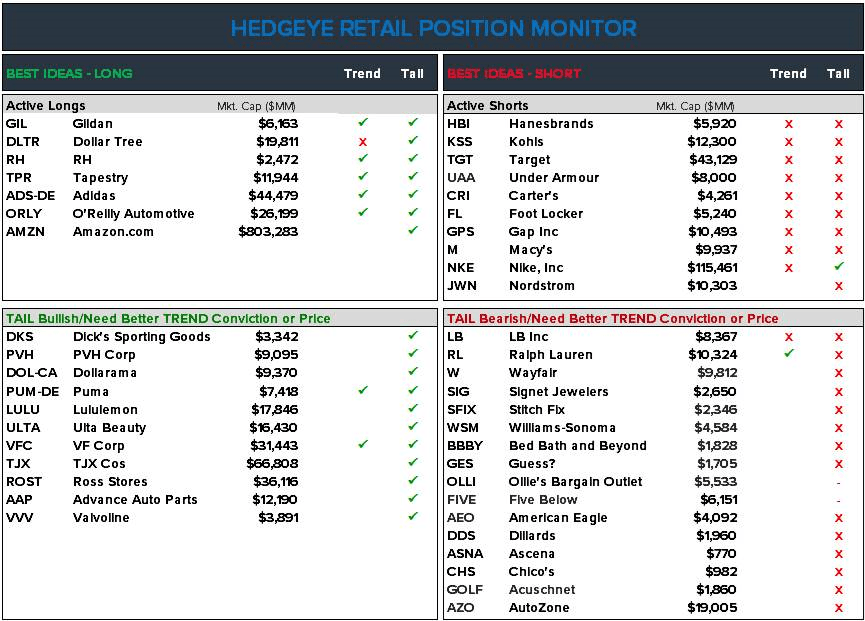

CHANGES ON BEST IDEA LONG LIST

- GIL: Now top name on Best Ideas list. Supplanted TPR. The reality is that there’s $800mm in high margin revenue that’s on its way – but not in consensus estimates. EPS goes from $1.90 to $3.00 over 2 years. Powerful TAIL call with TREND visibility. I like this idea a lot.

- DLTR: Went from #5 to #2 on idea list. Still concerned about Family Dollar comps, but likelihood of management getting ousted is building momentum, which paves the way to fix/sell FDO and simultaneously Break the Buck at DLTR: Great late-cycle name to own given counter-cyclical nature of comps. Huge upside potential with strong downside support.

- RH: #3 long…The most transformational business model in retail, with a CEO who has the authorization (and the guts) to repo 30% of the float …fast.

- TPR: Taken down to #4 from #1. Still a very big TAIL idea, with TREND earnings catalysts. Though the tightening gap between its multiple and the higher-quality European lux names like Kering and LVMH will cap valuation near-term while we fight the tape in China (20% exposure).

- ADS-DE: Moved Adidas up two notches to #5 on the list. Though I’m concerned about top line on this week’s print – so is the HF community that’s short it for the wrong reasons. Earnings should be fine (modeling 4% upside) due to Gross Margin upside.

- AMZN: Now dead last on my Best Ideas list. Business model shifting to GM$ model from top line growth over next two quarters. Perhaps already in stock, but near term set-up still bearish on the margin.

CHANGES TO LONG BENCH

- DKS: Moved to the top of the bench. Excellent candidate for Best Idea Long. Improving real estate profile, getting better allocations by vendors, golf bottoming. Hunt still an eyesore – but only 8% of biz. Trades at 40% discount to KSS, which is ridiculous. More Sears exposure (i.e. benefit) than people think.

- VVV: Added Valvoline to the long bench. Hybrid Energy/Industrial/Retail name – that arguably operates the highest 4-wall margin retail concept in the US.

- DOL-CA: Added Dollarama to vetting bench w strong Long bias. Stock got clocked – lost 1/3 of its value – as comps slowed. But I think the company will offset with better merchandise buys due to US tariff situation routing product through Canada, and will also take up price point yet again to stimulate top line. Stock still expensive, but it should be.

- PVH: Moved up to #2 on my Long Bench. Only thing holding me back is waiting for rate of growth to end bottoming process – which might take another quarter or two. Retail longs don’t work when top line is slowing – even if it’s in Street estimates.

- ULTA: Still sitting on long bench, but this thing is binary. After this Thursday’s analyst meeting it likely gets moved up, or goes to Short bench. Its game-time on this one.

- KORS: Booted from bench. This Vercase deal was simply bad, and I don’t like the strategic direction of the portfolio. We’re likely looking at a really solid print this week – especially on the Gross Margin line. But this name is turning into a poor-man’s Tapestry. I want no part of it.

CHANGES ON BEST IDEA SHORT LIST

- HBI: the notable callout here is that despite the fact that the call has worked, its’ STILL our top short. If our model is right this thing is en route to being a $5 stock, while the consensus view is that it is getting too cheap to short. Cheap on what numbers?

- KSS: I contemplated moving this one down the list given that 3Q is likely shaping up to be ok (note CEO press blitz 2 days before quarter end). But this is one where if everything works out to KSS’ plan its an $81-$83 stock – with it currently at $77. If anything goes wrong – and I mean ANYTHING – then downside is 5x. Downside is 50% over a TAIL duration.

- UAA: Moved up to #4 on short list after the parabolic run after 3Q EPS beat. Now it’s game time. At $16 the cost cutting call had teeth long-side. At $23 it has to prove it can grow, and that’s where I think UAA will face-plant.

- CRI: Moved a notch higher on Best Idea list. Just entered a period where a series of guide downs will prove that earnings have peaked – setting up for 2-3 years of flat earnings. That’s not in a $97 stock at 16x pe.

- GPS: Moved one notch higher on short list. 2H numbers are not doable, and setting up for a round of store closures.

- JWN: Moved from Short bench to Best Ideas. Stock at 3-year highs. 50% above level where LBO couldn’t get done. Trading at 20x stretch guidance.

CHANGES TO SHORT BENCH

- LB: moved to top of the bench. Core VS brand – what was one once one of the most defendable brands in apparel – has been perma-cheapened to the point where now Bath and Body Works is core profit center. That’s over-earning at 23% margin. LB is the hardest hit from lease capitalization accounting rules that change in ‘19.

- RL: Moved to #2 behind LB. Timing is critical here. RL’s numbers look good into this print. I’m at $2.29 vs Street at $2.16. Also, this is the second quarter in a row where top line will actually grow. Kind of like the inverse of PVH – short won’t work while Rev is getting better on the margin. I’m waiting for print-euphoria before putting this on Best Ideas list. Not enough in the stock right now. This story is absolutely broken. It’s the next Abercrombie. Though I need to be patient before getting heavy.

- GOLF: Added to Short Bench. Golf names have been en fuego due entirely to cyclical factors, while the secular story is as broken as ever. GOLF the better short than ELY due to the latter’s stake in Top Golf – good growth engine.

- SFIX: Moved to the bottom of the bench after recent sell off. But staying on…its running out of TAM faster than even a $27 stock thinks.

- W: Took this one higher on bench. The selloff after the quarter was not enough. Management is better at selling its stock than it is at selling furniture at a profit. This is a 23% GM% business with no hope for up upside, and a 27% opex structure that needs to stay elevated to keep the top line intact – not to mention that it needs physical stores $$$. There’s no road to profitability here, and yet it has 3x the EV of RH.

- JCP: Finally took this off the bench. No more call here. This has been fun since going against Ackman at $42. Will just watch and wait now while this company ultimately files.

- AZO: Took to the bottom of the bench. Though it’s a loser in the Auto Parts Retail space, the reality is that the space is one that I’m comfortable owning in 4Q as the replacement cycle continues to inflect positive.

- ASNA: Added to the bench for first time. This is a levered name that has 4,600 stores in concepts that should – for the most part -- not exist. It’s going the way of JCP.

- CHS: Comping down in perpetuity and won’t survive the next downturn. Take-under candidate.