In the "Cyclical Peaks" Section of our Q4 Macro Themes Deck we asked the rhetorical question of what drives corporate sales, earnings, and margin growth past Q3 of 2018 given our view on economic growth. Well into the back nine of Q3 earnings season with 328 of 500 companies having reported, sales & earnings growth for S&P 500 companies in aggregate is tracking +8.0% & +23.6% YY. Some conclude earnings growth is "good" and corporates are "resilient". We would say that those Q3 line items are rate-of-change slowdowns from Q2 if earnings season ended today. We're confident that debate and its implications will continue indefinitely...

From an expectations standpoint we know that a wall of steepening base effects has taken out-quarter expectations lower. As of now, the aggregate Q4 consensus Bloomberg estimate for YY sales & earnings growth for S&P 500 constituents is ~6% & ~17% Y/Y.

Here are some simple sine curve realities from Q3 reporting season to date as well as a few takeaways on "actuals" vs. "estimates".

Chart 1: This is one of the first charts in "Cyclical Peaks". Q2 of 2018 marked the 8th consecutive quarter of GDP growth, Earnings Growth and Margin expansion and ended with the steepest top-line rate of growth for S&P 500 companies (+9.4% YY) since Q3 of 2011 and the steepest bottom line rate of growth (+25.3% YY) since Q3 of 2010.

Chart 2: "Growth" is broad-based across sectors and indices within the deceleration backdrop. As mentioned consensus is expecting the deceleration to get more drastic in Q4.

Chart 3: Should Q3 end here, the conclusion is a "top-line growth slowdown"

Chart 4: Should Q3 end here, the conclusion is an "earnings growth slowdown"

Those are trivial realities to set up a few tidbits on how expectations have fared...

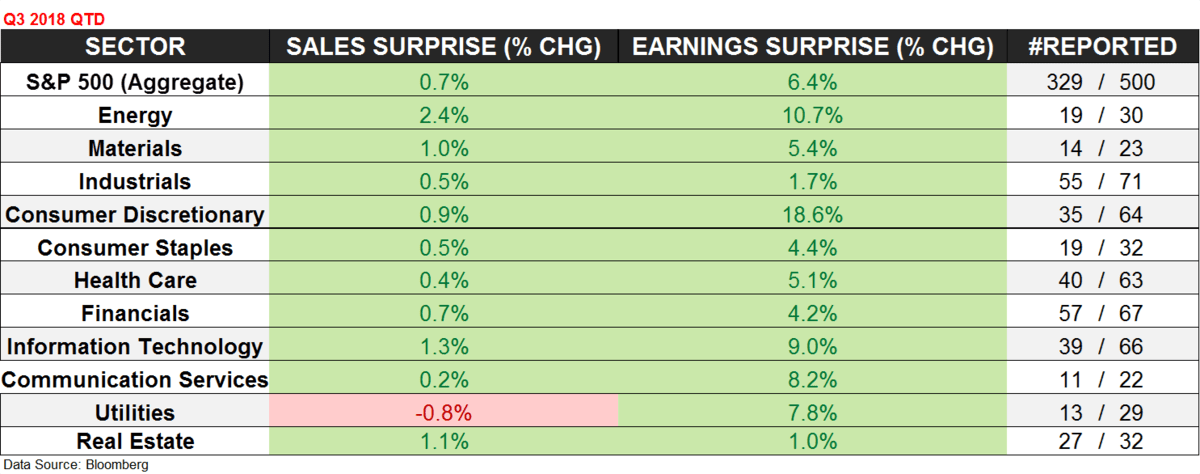

Chart 5: Every sector with the exception of Utilities has "beat" top-line estimates. If we look at the S&P 500 in aggregate, it has beaten top-line estimates by 70 bps which is almost exactly in line with its 5Yr average beat rate of 60 bps. However, the beat-rate gap (actuals vs. estimates right before earnings) is smallest since Q1 of 2017 and much less than the 1.5% beat rate in Q2. Conclusion: the surprise "growth" factor on top of estimates hasn't been nearly as helpful this quarter.

Chart 6: A time-series chart of top line "beat rates" for the S&P 500

Chart 7: Bottom-line Earnings beat rates have so far aggregated to a +6.4% gap in actuals vs. estimates, which 1) is positively much wider than the average beat rate of +4.6%; BUT 2) A tightening margin from Q1 of 2018 (6.9%). Similar conclusion.

Chart 8: One positive to counter beat rate trends is that NTM earnings revision trends were positive throughout Q3, increasing +3.2% from the beginning to end of the quarter with economic growth surprises. Therefore, the tightening in line item "beat" rates did not come on the back of eroding expectations. With that being said, the intra-quarter Q3 NTM EPS revision was a slowdown from +4.0% in Q2 and +9.1% at the peak in Q1 of 2018.