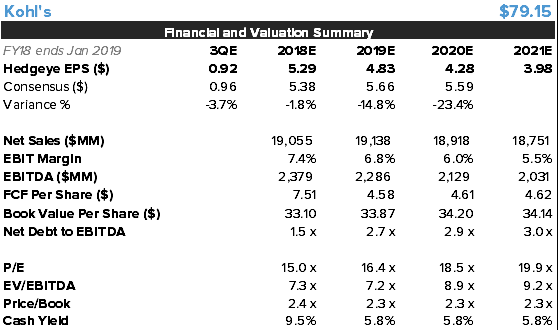

Tops are processes, not points – and the end of the 12-month KSS financial model acceleration and subsequent stock rip to new all time highs is nearly complete. You just saw the best KSS has to offer, and it still did not even outcomp Wal-Mart. Now we’re in the back half, top line compares get meaningfully more difficult starting this month, cost pressures just accelerated, it’s gonna miss 2H EPS, and and we’re looking at the last time KSS is likely to earn over $5 per share ever again.

It’s sitting at a peak P/E of 16.5x our ’19 number and a sub 6% FCF yield (note that KSS has traded over 15%). Bullish narratives around real estate optionality and ‘shrinking to grow’ are just as weak as the ‘JCP is going bust’ bull call (KSS sales did not budge when JCP hemorraged $6bn in sales six years ago – TJX is your beneficiary there). Adding new brands like 9 West – which went bankrupt in April – will hardly be a traffic driver, and the Amazon partnership sounds great but is too early, too small, too non-exclusive, and too dilutive to matter.

Ultimately, you have to believe that KSS is a growth company again with $7 in EPS power to be buying this today. I think that this confluence of narratives around KSS being a retail growth company again will unravel as violently as it did in April 2015 when it went from $60 to $80 in a quarter, and two quarters later was a $35 stock. If our model is right then this story should begin to unravel in 3Q – getting you paid this year. Then when our sub-$5 EPS power call plays out in 2019 we’re looking at a 10% FCF yield – or revaluation to $50 (at a time when the cash conversion cycle no longer drives 50% of incremental cash flow growth) and that’s without any negative hit from credit reversing course (then sub $4 EPS comes in play and we’re back to $35 again). Search the transcript for the word ‘credit’…it can’t be found. No one cares. In the end we’re looking at $30 downside if we’re right, and $5-$8 upside if the consumer landscape is strong enough to allow KSS to come out ahead in 3Q – or if it beats the quarter by accident. Tough to find that kind of asymmetric downside on a short in retail today.

--McGough

Here’s McLean’s Take on the Model

Print Quick Take

- 7% EPS beat in-line with our model. Management didn’t quite flow the whole beat through into FY guidance. Taking up the low end by 10 cents and the high end by 5 cents to $5.15 to $5.55

- Comp better than expected at 4.3%, with 120bps of calendar shift benefit. The acceleration was expected, but it’s still impressive to see “shifted” comps accelerate nearly 300bps on a tougher comparison.

- Gross margin was up 42bps on an easier compare after +50bps last Q.

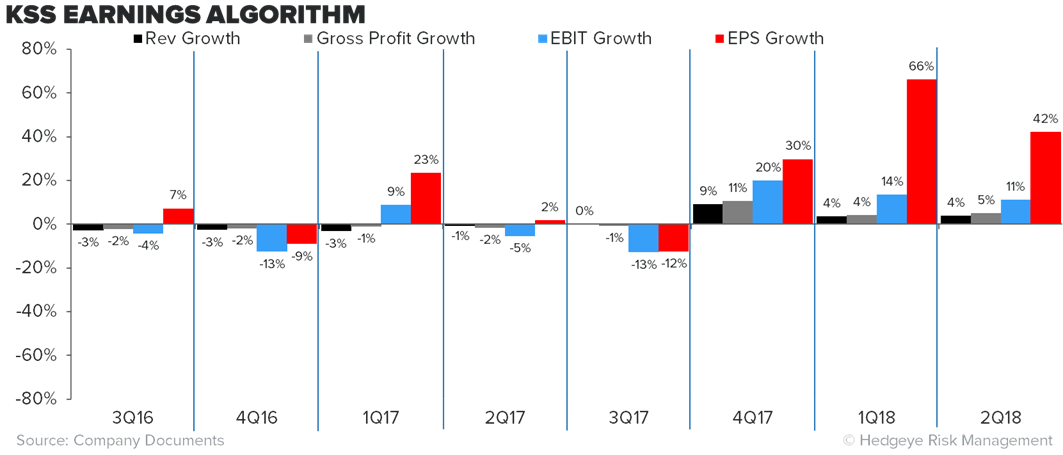

- The absolute quarter was solid, 4% comp, 5% gross profit growth, 11% EBIT growth and 42% EPS growth (taxes). And you can’t deny the cash flow performance. CFFO up 100% with inventories remaining clean. (though we’re 3.5 quarters into this trend. Now what?)

- We saw EBIT slow on an accelerating top line. We think that is a big risk as the company starts facing slowing top line from slowing macro and tougher compares as well as harder margin comparisons in 2H.

Comp Cagey

- When asked about the comp components, CFO answered with the following:

- Yeah, so as you know we no longer break out the components of comp sales. As far as I'm concerned as the finance executive, as long as I'm driving a positive comp and can therefore leverage and accrete EBIT, I'm fairly happy. I did say our ATV drove our comp sales in Q2 and Michelle pointed out that traffic remains our number one priority. We do have, it can make one piece of color for you which is we do have automated counters in most of our stores if not all of our stores. We compare that against competitors. We all report it to a third-party and our traffic count is, we believe, in good shape relative to what we see from competitors.

- Why the cagey answers on comp components? Is traffic not as strong as it appears? Getting more customers or not?

- What stands out is what management didn’t say. We didn’t hear “traffic was positive” or “traffic accelerated” despite the company claiming earlier this year that its growing its customer base. To be clear, this NEEDS to be a traffic growth story for this to work long side.

“Standard to Small” likely matters more than you think.

At face value, its bullish that the company has shifted 500 stores to “small” and maintained good results. But let’s look at some of the specifics of this action.

- Low DD decline in inventory in these 500 stores. That’s helpful as to the cleanliness in inventory.

- With the “Standard to Small” initiative, we’re curious as to what extent this translates into any comp effect with the change to comp accounting last year…

- “In 2017, we changed our comparable sales definition to align with our internal company reporting. Under the new definition, Kohl's store sales are included in comparable sales after the store has been open for 12 full months. On-line sales and sales at remodeled and relocated Kohl's stores are included in comparable sales, unless square footage has changed by more than 10%. The prior definition included sales for stores (including relocated or remodeled stores) which were open during all of the current and prior periods.”

- We’re not sure a “standard to small” store counts as a SQFT reduction. Though this quarter did see net sales growth 40bps lower than comp growth with store count up YY and no sequential change in selling or gross square footage. We suspect comp/rev spread could widen into year end.

- What happens to comp, inventory and GM next year, if they all look better due to scaling down the size of store locations in an extremely bullish consumer environment? Lapping that in 1H19 could bring unexpected challenges.

There’s no mistake that we’re lapping the significant inventory benefit of this initiative. Unless it gets rolled out to all stores, the inventory improvements will slow – and this is definitely not an ‘all store’ initiative – it’s a ‘bad store’ initiative.

D&A Decline

- 2Q18 saw D&A down for the first time in 7 quarters. One of the odd elements of KSS cash flow, is the fact that D&A has recently been ~$200mm to $300mm higher than capex annually, yet it continued to grow. D&A was guided to $960mm this year, vs $990mm last year, so perhaps D&A will start to revert after this quarter’s inflection. D&A commentary was the following: “consistent with the prior year as additional IT amortization and depreciation on our fifth e-commerce fulfillment center, which opened last summer, were more than offset by the reduction and depreciation due to the maturing of our store portfolio.”

Nine West Coming

- In April 2018, it was announced that Nine West's U.S. business filed for bankruptcy and will close all stores. The Nine West brand was acquired by Authentic Brands Group out of auction months later.

- Now it’s heading into KSS doors. KSS adds a few brands every year, and the brands rarely make a material impact on results, they’re just too small. With Under Armour launch being less than a comp point last year, Nine West won’t be a needle mover – and what it does move on the top line will dilute Gross Margins as it will replace private label.

Credit

- The word “credit” was absent from this call. Why shouldn’t it be? it’s only 35% of EBIT. Actually it's smart for management to not highlight the 4.8% increase in other revenue, since management has little control over that line item. This increase is likely driven by higher credit revenue as we have seen improving credit metrics from low end card lenders (COF/SYF). What was a building headwind just over a year ago has quickly inflected into a Trend tailwind.

- The revenue increase meant credit contributed ~$12mm of incremental GP or ~5 cents in EPS this Q.

- We think KSS’s credit exposure is still a large unappreciated tail risk.

Under Armour and Active

- Active continues to drive a significant portion of growth, with the major brands outcomping the company.

- Under Armour accelerated its comp from 1Q, which makes sense given the spring weather trends.

- The company started its Active Expansion pilot in 30 stores earlier this month. The expansion means a 40% increase in active square footage, and will provide customers with almost 50% more choices.

- KSS should put the brakes on Active expansion. This move is too backward looking.