Editor's Note: Below is transcribed analysis from today's edition of The Macro Show hosted by Senior Macro analyst Darius Dale. Click here to learn more about The Macro Show.

|

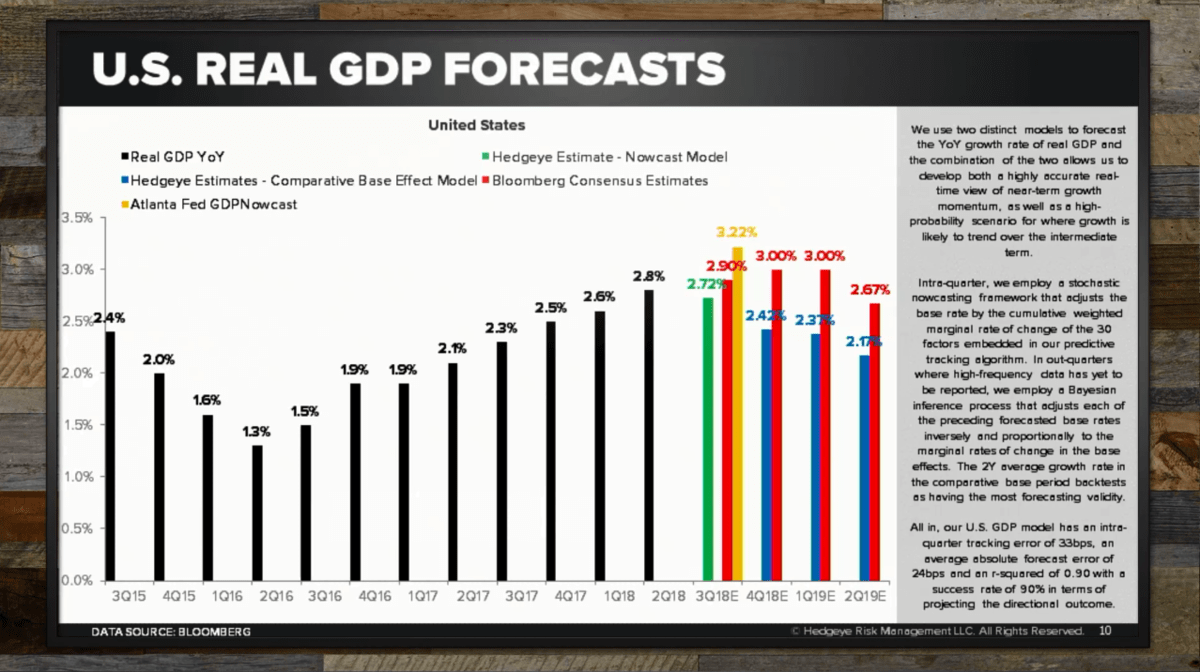

Subscriber: Any comment on the likelihood of new all-time highs in the S&P 500? I see lower highs in the Risk Range and low volume. Dale: I think the market signaling new all-time highs is definitely a different set-up than we’ve had. That’s an incremental signal that we need to digest. I don’t want to mince words. This all-time high is not like the all-time high we saw in January. That all-time high was perpetuated by Quad 2 growth factor exposures outperforming with positive earnings momentum. What’s actually leading the market to all-time highs now is not the stuff that people are long. It's slow growth exposures. It’s not the fundamental thesis that people are long based on Wall Street consensus GDP estimates. I think people are being forced to chase things like REITs (VNQ) and Consumer Staples (XLP) and Utilities (XLU) after this move. That’s what you see now in some of these implied volatility discounts that are showing up in REITs recently. There’s complacency there because people have to chase. If anything we’ve learned in the Q2 reported season to date, if you’re not perfect you’re going to get tagged. If you weren’t signaling anything other than rainbows and puppy dogs and roses up until now, that’s probably it for you. But the economic outlook has changed. That’s the thing about our #PeakCycle macro theme for the U.S. We’re not calling for a material bombing out in growth. What you see in this chart is a pretty easy crest then rollover. But what matters is consensus has U.S. growth up and to the right, accelerating after 2 whole years of acceleration. That’s the call. The call is that the data is just not as good from a second derivative perspective. If you roll the clock forward a couple quarters, it’s going to look a lot more negative than what consensus growth estimates imply from both a top-down GDP perspective and from a bottom-up EPS perspective. |