THE HEDGEYE EDGE

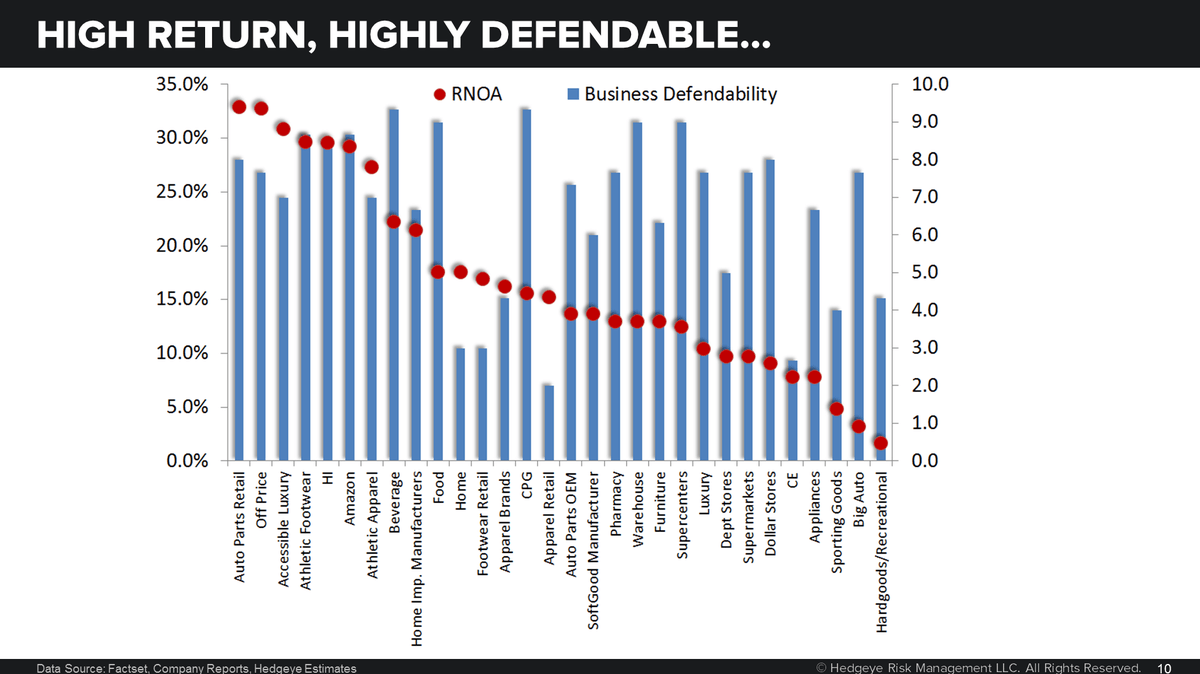

O’Reilly Automotive (ORLY) is a best in class retailer that is getting stronger. The business defendability and return characteristics in Auto Parts Retail are both off the charts. It’s simply not in the stocks today.

The consensus ‘Amazonism fear’ of the space receives too much attention. If AMZN had to re-create any auto parts retailer – it would be the biggest distraction outside of building a fleet of US delivery trucks and scaling up drones. At 16x 2018 EPS there is more Amazon fear than acknowledgement of its competitive moat and future earnings power discounted in the current share price.

O’Reilly’s protective moat leaves it with the lowest AMZN risk in its space. As it leverages its distribution network and supplier base it will prove that it has not yet seen peak margins. The combination of best in class organic DIFM/DIY (Do-It-For-Me and Do-It-Yourself) networks, store growth, and store maturation curve provide the best outlook for trend and tail sales growth.

Customer exposure to the Amazon threat is the lowest of the group due to its distribution network and unappreciated digital platform. It is likely to lead future industry consolidation, either by making a strategic move or being so good that it forces the others to play defense to catch up.

We see tail EPS Power to upwards of $20. Over trend we are facing the tail end of a bottoming process in comps (cycled difficult +4.8% comparisons in 2016 with +1.5% SSS in 2017). Our industry's call needs to be flat out wrong for ORLY to decelerate from here. Same-Store Sales have consistently grown for over a dozen years. We expect a re-acceleration as the new car cycle (the six year lag for new cars to enter the addressable market for auto parts retailers) headwind becomes a tailwind.

Consensus expectations are at 2.9% for same store sales in 2018 and our work takes us above that. We are looking for 300bps acceleration in revenues in 2018. Gross Margins have expanded annually for over a decade. We expect gross margins to continue their upward trajectory after an additional year of investment in digital.

ONE-YEAR TRAILING CHART