CLICK HERE to view a replay webcast of the call.

CLICK HERE to view the associated slides.

Key points discussed on the call:

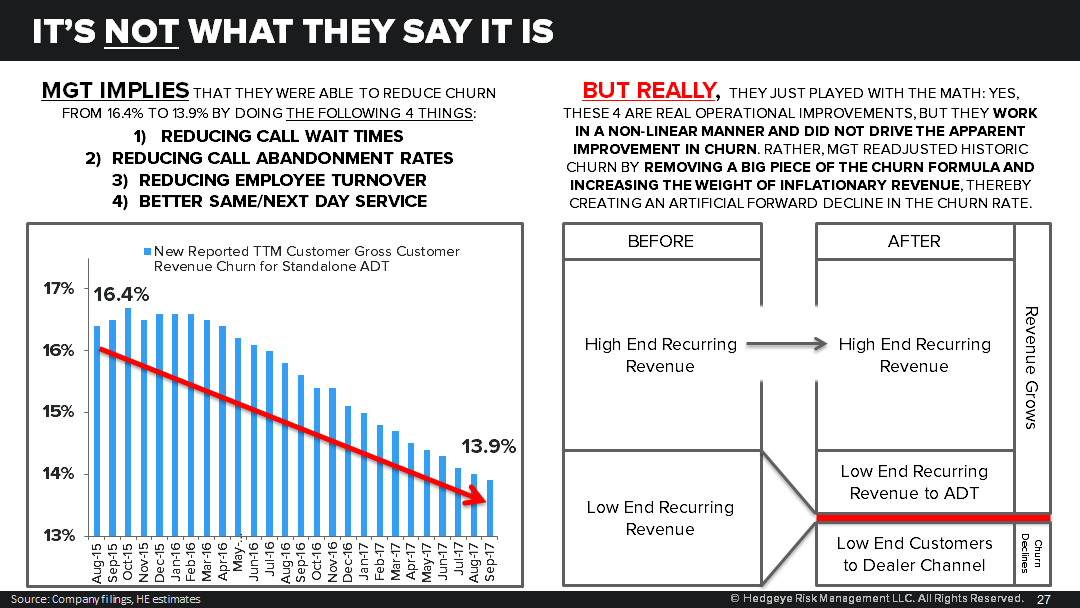

Point 1: Inflection in churn has been more artifice of changing the denominator than the hard work of improving the business

Point 2: There is some real churn improvement just starting to show through in 4Q17 with LTM acquired revenue higher than churned revenue that helps set up 1H18 as peak growth rate

Point 3: Higher prices on the retained revenue base is also a factor in driving lower churn, rather than operational change

Point 4: Double-digit churn % is likely a permanent part of the equation for this ‘life-saving’ service. 75% of that churn is a reflection of customers expressing that the service isn’t worth it. Why? Start with 95% false positives, the cost to the customer (and to ADT) of false positives, and you will understand why points of scale in ADT’s favor will erode.

Call Timestamps:

- Introduction (0-2:40)

- Management’s bull case (2:40-5:40)

- Our ADT IPO Short Thesis (5:40-8:22)

- Customer Reconciliation and Tale of 2 Churns (9:45-20:55)

- The Churn Stack: Long Term Customer Churn Rate (20:55-25:20)

- False Alarms and Their Effect on Churn (25:20-31:40)

- Competitive Landscape and What Makes this Technologically Disruptable (31:40-38:05)

- Looking forward: Market, Peak Growth in 2018, ADT Pulse Pricing (38:05-44:20)

- Model Still Doesn’t Make Sense (44:20-46:15)

- Comps, Valuation, and Closing thoughts (46:15-52:35)

- Q&A (52:35-55:40)