In November, our Healthcare analysts Tom Tobin and Andrew Freedman wrote the research note: "VRX | Bear Case $20." The stock has plummeted since then -- down -75%.

Here's an exclusive update from Andrew Freedman:

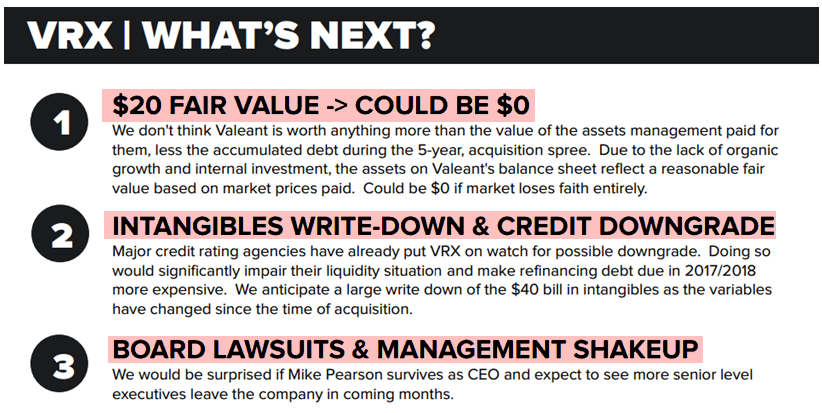

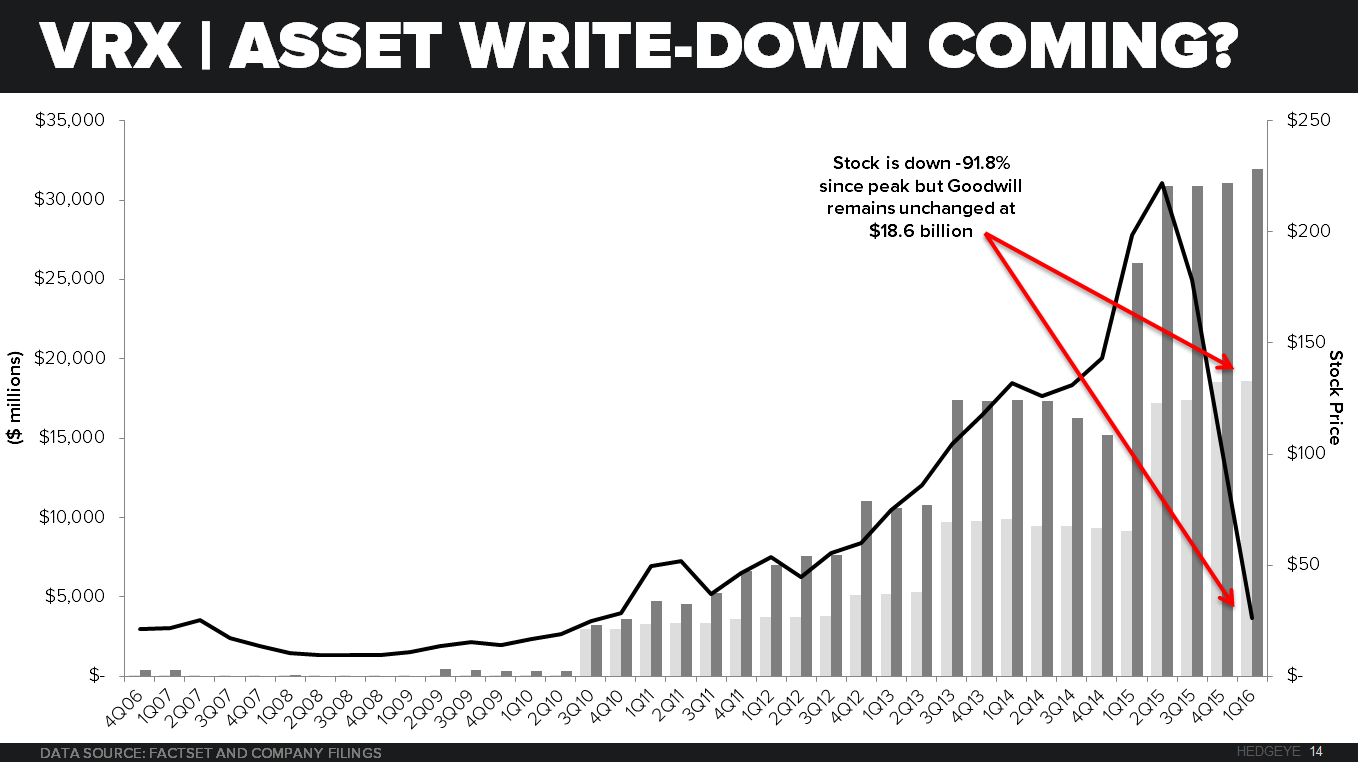

"Our $20 “Bear Case” valuation was based on acquisition price of the assets less accumulated debt and assuming the assets perform on par with historical trends. Clearly the latter part of that assumption is no longer valid given the deterioration in the core business that is likely permanently impaired. With $18.6 billion of Goodwill on the balance sheet and the stock down 91.8% from its peak, the market is already telling us that Valeant overpaid for these assets. We are surprised that Valeant has yet to take a write-down to reflect this reality.

The probability of a Valeant bankruptcy is high, and the probability that we see a sub-$20 stock over the next 12-months is even higher. At this stage, it makes more sense to sell the company off in pieces, repay debt holders, give what is left over (if anything) to stockholders and call it quits."

Chart below is from March, 17 2016.

Tobin and Freedman have been laying out the short case for some time. Here's a video from earlier this year which largely predicted what's happened at Valeant, including the precipitous drop in VRX shares and "we would be surprised if Mike Pearson survives as CEO."

Click below to watch. It's instructive to understand what's to come.

Additional updates worth reading from our Healthcare team:

- Click here to read our original 58-page institutional Black Book on Valeant.