Editor's Note: This is a special Hedgeye Guest Contributor note written by Mike O'Rourke. Mike is the Chief Market Strategist at JonesTrading where he advises institutional investors on market developments. He publishes "The Closing Print" on a daily basis in which his primary focus is identifying short term catalysts that drive daily trading activity while addressing how they fit into the “big picture.”

Now that Q2 earnings season has commenced, it is an opportune time to examine the expectations landscape.

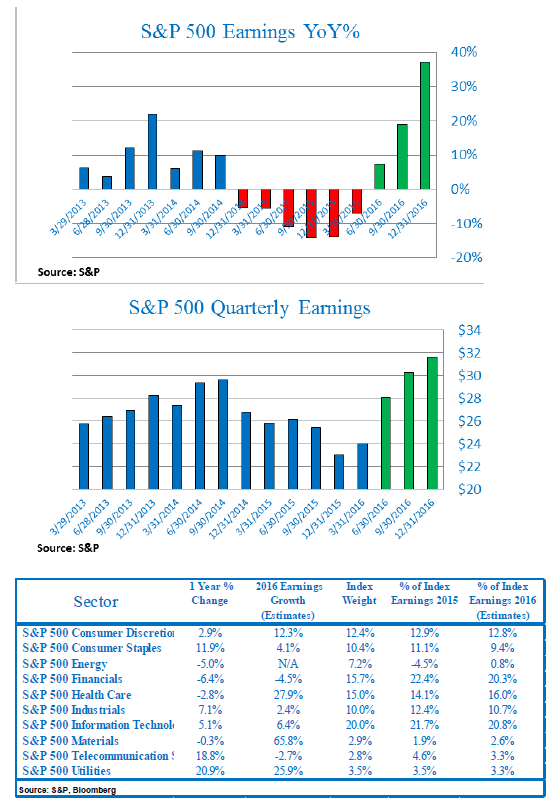

According to Standard & Poor’s, 2015 earnings finished at $100.45, down from $113.01 in 2014. The current forecast for 2016 earnings is $113.96. Considering Q1 2016 earnings were down 7% year over year, it obviously makes 13% full year earnings growth a tall order. Per the S&P data, the last 6 quarters have posted year over year declines. Despite that disappointing trend, Q2 earnings are forecast to rise 7% year over year. As is typical, earnings estimates are very back end loaded, allowing more time to deny reality.

For Q3, earnings are forecast to grow 19% year over year, and in Q4, they are forecast to grow a whopping 37% year over year (chart below). Of course, quarterly earnings in excess of $30 per share would be new record levels (chart below). For some reason, this does not seem like an environment primed for posting record quarterly earnings.

Certain aspects of the environment that led to the peak in earnings in 2014 softened, but they have not reversed. The Dollar remains relatively strong. Although the Dollar index is down 4% from its recent peak, it is still up over 20% from the 2014 level from which it broke out. While Crude has managed a remarkable rebound from its February low, the average price of spot WTI was $48.65 in 2015, and thus far in 2016, it is just over $40.

The volatility around earnings due to the broad decline should fade and this is expected to be the Energy Sector’s first positive earnings quarter since the end of 2014. The Health Care sector will be key, and is expected to do much of the heavy lifting for index earnings, growing close to 30% in 2016 (table below). Considering Q1 earnings for the sector only grew 3.3% year over year, Q2, Q3 and Q4 are forecast to grow 31.7%, 37.7% and 40.5% respectively. There is not much else based on reality in the markets these days, so maybe there is no reason to expect earnings estimates to be any different.