Here's analysis via Hedgeye CEO Keith McCullough in a note sent to subscribers earlier this morning:

"The 10-yr Treasury yield crashed on Friday's jobs bomb (that was in line with the change in Janet’s favorite labor market indicator index, more on that below) to 1.71%, which implies that A) the data is beating the Fed’s forecasters, big time, YTD and B) if she hikes into this, she’s going to implode all of the illusions of real growth (i.e. the aforementioned reflation trades)"

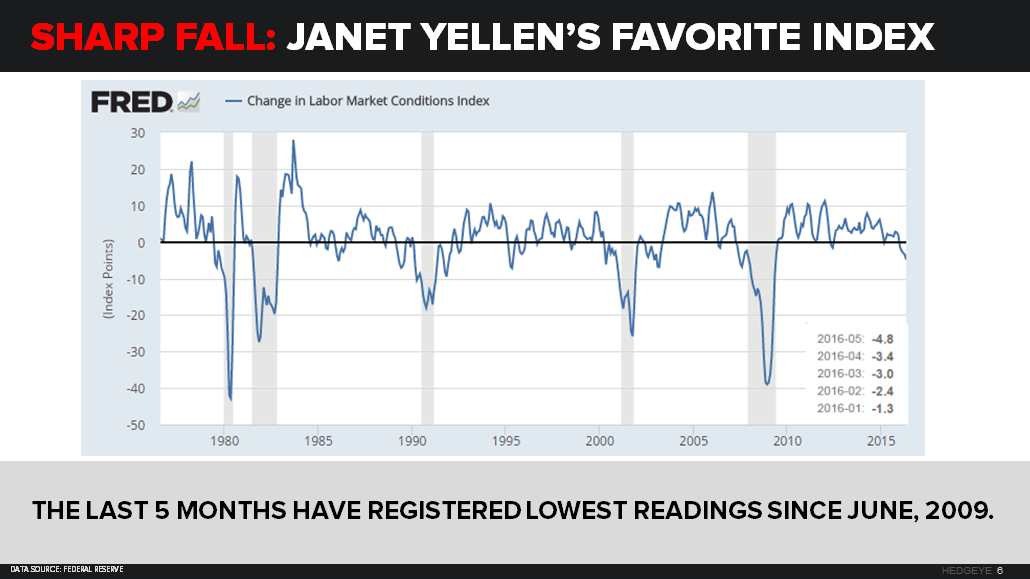

More on Yellen's favorite indicator...

The "Labor Market Conditions Index" contracted for the fifth straight month to down -4.8% in May. Meanwhile, the prior month was downwardly revised from -0.9% to -3.4%.

In other words, not good.

(For more on how the Fed could interpret all of this, check out "5 Charts: How Last Week's #JobsBomb Is Impacting Global Markets.")