Editor's Note: Below is a Hedgeye Guest Contributor research note written by Dr. Daniel Thornton. During his 33-year career at the St. Louis Fed, Thornton served as vice president and economic advisor. He currently runs D.L. Thornton Economics, an economic research consultancy.

Please note that while the views expressed in this column do not necessarily reflect the opinion of Hedgeye, Thornton's analysis is hard-hitting and provocative. A must-read for thoughtful investors.

In a speech on May 26, Fed Governor Jerome Powell noted that “A long period of very low interest rates could lead to excessive risk-taking and, over time, to unsustainably high asset prices and credit growth.”

One cannot help but wonder what Governor Powell considers to be a “long period.” The federal funds rate quickly headed to zero when the Fed increased the monetary base by making loans to financial institutions following Lehman Bros. bankruptcy announcement on September 15, 2008. The Federal Open Market Committee (FOMC) slowly reduced its target for the funds rate from 2% to effectively zero by December 15, 2008, in spite of the fact that the funds rate was already near zero, see "Requiem for QE."

The funds rate target remained at this level for SEVEN years before the FOMC increased the target to between 25 and 50 basis points on December 16, 2015. So the funds rate has been excessively low for nearly 7.5 years. This is unprecedented, and an extremely long period.

I am also struck by Powell’s suggestion that “very low interest rates could lead to excessive risk-taking and, over time, to unsustainably high asset prices and credit growth.” It’s already happened! The FOMC’s low rate policy has already led pension funds and retirees to take excessive risks.

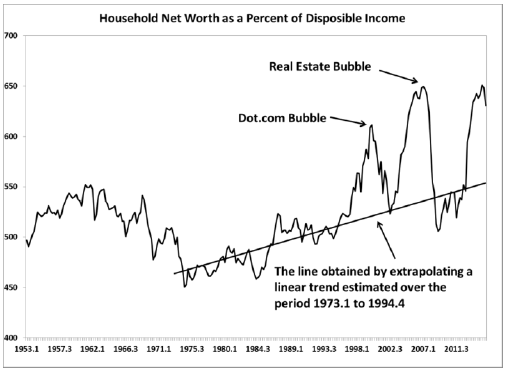

It has also produced unsustainably high asset prices as evidenced by this graph from "My Scary Chart." The figure shows household net worth as a percent of disposable income. The first two peaks were due to unsustainable increases in assets prices: The first, to equity prices, the second to home prices.

The third is due to a combination of equity and home prices. This rise in household wealth also seems to be unsustainable. The question is: Does it decline slowly to the trend line or does it fall precipitously like the previous two?

The FOMC’s policy has already caused banks to make an extraordinary quantity of loans in a slow growth economy and has caused the M1 money supply measure to more than double since Lehman’s announcement, see Excess Reserves and Excessive Risk Taking.

Powell appears to be waking up to the consequences of the FOMC’s policy. He concluded his speech with, “My view is that a continued gradual return to more normal monetary policy settings will give us the best chance to continue to make up lost ground.” However, he is yet to come to the realization that the return to “normalcy” needs to happen quickly not gradually. Waiting two or more additional years won’t improve the economy; it can only cause further harm.