TODAY’S S&P 500 SET-UP – February 5, 2013

As we look at today's setup for the S&P 500, the range is 24 points or 0.45% downside to 1489 and 1.16% upside to 1513.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

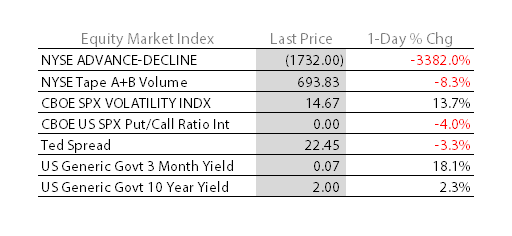

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.74 from 1.71

- VIX closed at 14.67 1 day percent change of 13.72%

MACRO DATA POINTS (Bloomberg Estimates):

- 6:30am: ESM to sell as much as EUR2b 91D bills

- 7:45am/8:55am: ICSC/Redbook weekly retail sales

- 8:30am: Fed’s Duke speaks on community banks in Duluth, Ga.

- 10am: ISM Non-Manf. Composite, Jan., est. 55.0 (prior 55.7)

- 10am: IBD/TIPP Economic Optimism, Feb. est. 47 (prior 46.5)

- 11am: Fed to purchase $1.25b-$1.75b debt in 2036-2042 sector

- 11:30am: U.S. Treasury to sell 4W bills, $25b in 1Y bills

GOVERNMENT:

- CBO releases federal budget projections, economic outlook

- Yahoo’s Mayer, Goldman’s Blankfein in Obama immigration session

- CFTC holds public roundtable to discuss agency’s proposed rulemaking, “Enhancing Protections Afforded Customers and Customer Funds Held by Futures Commission Merchants and Derivatives Clearing Organizations,” 9:30am

- SEC holds a roundtable discussion on decimal-based trading, tick sizes for small, medium sized companies, 10am

- CFPB Director Richard Cordray, National Credit Union Administration Board Chairman Debbie Matz hold “town hall webinar” on “Ability-to-Repay” rule, 3pm

- HHS, FDA discuss creation of alternative pathway for expediting approval of drugs needed for unmet medical needs, 9am

- FCC Chairman Julius Genachowski holds field hearings on Hurricane Sandy to consider how nation’s communications networks work during crises, 9am, 2pm.

- FCC Commissioner Robert McDowell and David Gross, former U.S. ambassador for international communications and information policy, testify at hearing on Internet freedom before 3 House subcmtes, 10:30am

WHAT TO WATCH

- Dell board said to meet to vote on $24b leveraged buyout

- Virgin Media in talks with Liberty Global on possible transaction

- Hartford announces buyback, debt repayment plan after Sandy

- Goldman hired by Russia as corporate broker to boost image

- U.K. economy faces risk of a prolonged stagnation, NIESR says

- German push to speed bank bondholder-loss plan gains momentum

- Wells Fargo to target sovereign wealth funds in Dubai expansion

- Buffett gets $1.8b in investment assets from Cigna deal

- Fidelity said to press Endo Health to consider selling itself

- Facebook said to develop location-tracker app for smartphones

- Homes sell in 2 weeks as U.S. spring buyers face low inventory

- MF Global customer funds rules will get another hearing at CFTC

- UBS 4Q loss narrower than est. after Libor fine, job cuts

- Hemispherx fails to win U.S. approval for chronic fatigue drug

- IBM adds cheaper power servers to expand in emerging markets

- Boeing asks U.S. FAA to permit test flights with Dreamliner

- J.C. Penney asks judge to bar claim retailer defaulted on bonds

- Consumer Reports says Ford, GM turbo engine benefits overstated

- Shirakawa plans to exit as Bank of Japan governor on March 19

EARNINGS:

- Becton Dickinson (BDX) 6am, $1.23

- Diamond Offshore Drilling (DO) 6am, $1.09

- Centene (CNC) 6am, $0.36

- Emerson Electric (EMR) 6:30am, $0.62

- Spectra Energy (SE) 6:30am, $0.31

- Eaton (ETN) 6:30am, $0.93

- Littelfuse (LFUS) 6:30am, $0.84

- Church & Dwight (CHD) 7am, $0.57

- Cardinal Health (CAH) 7am, $0.86

- Sirius XM Radio (SIRI) 7am, $0.02

- Archer-Daniels-Midland (ADM) 7am, $0.59

- Delphi Automotive (DLPH) 7am, $0.87

- OneBeacon Insurance Group (OB) 7am, $0.12

- Techne (TECH) 7am, $0.77

- Aecom Technology (ACM) 7am, $0.30

- HCA Holdings (HCA) 7:03am, $0.83

- Alliant Techsystems (ATK) 7:30am, $1.71

- Teco Energy (TE) 7:30am, $0.21

- Estee Lauder (EL) 7:30am, $1.05

- Automatic Data Processing (ADP) 7:30am, $0.71

- Vishay (VSH) 7:30am, $0.08

- Arch Coal (ACI) 7:45am, $(0.15)

- Inergy Midstream (NRGM) 7:45am, $0.16

- Inergy (NRGY) 7:46am, $0.08

- SunCoke Energy (SXC) 7:59am, $0.34

- Magellan Midstream (MMP) 8am, $0.65

- Spectra Energy (SEP) 8am, $0.37

- Computer Sciences (CSC) 8am, $0.65

- Kellogg Co (K) 8am, $0.66 - Preview

- UDR (UDR) 8am, $0.34

- Agco (AGCO) 8am, $0.98

- Liberty Property Trust (LRY) 8am, $0.63

- Lennox International (LII) 8am, $0.55

- Allergan (AGN) 9am, $1.18 - Preview

- Bell Aliant (BA CN) Pre-Mkt, C$0.41

- Unum Group (UNM) 4pm, $0.77

- Chipotle Mexican Grill (CMG) 4pm, $1.95

- Expedia (EXPE) 4pm, $0.65

- Ultimate Software (ULTI) 4pm, $0.39

- Universal (UVV) 4pm, NA

- Panera Bread Co (PNRA) 4pm, $1.74

- CBL & Associates Properties (CBL) 4pm, $0.57

- Kimco Realty (KIM) 4:01pm, $0.31

- Cerner (CERN) 4:01pm, $0.64

- Fiserv (FISV) 4:01pm, $1.40

- CME Group (CME) 4:01pm, $0.64

- NeuStar (NSR) 4:01pm, $0.72

- Hanesbrands (HBI) 4:01pm, $1.04

- Team Health (TMH) 4:01pm, $0.35

- Shutterfly (SFLY) 4:02pm, $1.39

- Thoratec (THOR) 4:02pm, $0.37

- Take-Two Interactive (TTWO) 4:05pm, $0.55

- Zynga (ZNGA) 4:05pm, $(0.03)

- Jack Henry & Associates (JKHY) 4:05pm, $0.50

- Myriad Genetics (MYGN) 4:05pm, $0.38

- Alterra Capital Holdings (ALTE) 4:05pm, $(0.44)

- Trimble Navigation (TRMB) 4:05pm, $0.55

- Aflac (AFL) 4:07pm, $1.48

- Hain Celestial Group (HAIN) 4:10pm, $0.69

- Genworth Financial (GNW) 4:10pm, $0.27

- KKR Financial Holdings (KFN) 4:12pm, $0.39

- Walt Disney (DIS) 4:15pm, $0.77

- CH Robinson Worldwide (CHRW) 4:15pm, $0.70

- Equity Residential (EQR) 4:25pm, $0.76

- Genworth MI Canada (MIC CN) 4:30pm, C$0.78

- Acadia Realty Trust (AKR) 5pm, $0.28

- HNI (HNI) 5:30pm, $0.43

- Suncor Energy (SU CN) 10pm, C$0.74

- BioMed Realty Trust (BMR) Post-Mkt, $0.34

- MDU Resources Group (MDU) Post-Mkt, $0.39

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

CRB Index – Commodities failing at our long-term TAIL risk line for the CRB Index (306) was a big reason why we got longer of Asian/US stocks into yesterday’s close; CRB Index (peaked in 2011) = long-term bubble that is popping as the US Dollar continues to make a series of long-term higher lows; Oil is overbought up here, but we need to see that drop back below $113 (Brent).

- Iron Ore Seen Poised for Bear Market by Smirk as Supply Expands

- Platinum Supply Falls to 13-Year Low as Mines Close: Commodities

- Oil Rises From One-Week Low as Recovery Signs Counter Supplies

- Platinum Trades Near 17-Week High on Concern Supplies Will Fall

- Nickel Drops Most in Three Weeks as Investors Seek to Curb Risk

- Soybeans Rise for Third Session as Brazil Rain May Slow Harvest

- Coffee Gains as Vietnam Growers Hold Supplies; Sugar Advances

- Oil Supplies Rise in Survey on Seaway Disruption: Energy Markets

- Gasoline at U.S. Pumps Jumps Most in Two Years on Crude Rally

- Mongolia Should Get More Control of Rio Mine, President Says

- ADM Profit Beats Estimates After Soybean-Processing Margins Gain

- Niger in Talks With Areva for Uranium Mines to Give More Funds

- Record China Flour Cost Spurring Wheat Imports: Chart of the Day

- Anglo American CEO Carroll Says Platinum Industry Is ‘in Crisis’

CURRENCIES

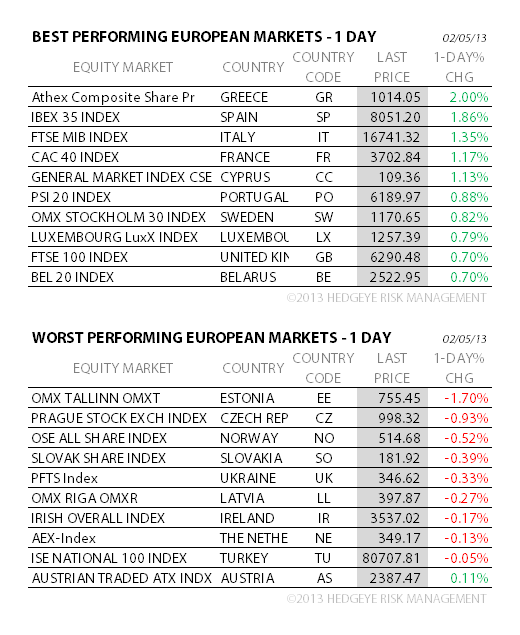

EUROPEAN MARKETS

EUROPE – didn’t take much to freak people out in European Equities – Socialist Quote of The Day “the Euro shouldn’t fluctuate as the market sees fit” (Hollande), as France reports a bomb of a Services PMI print for JAN at 43.6 (vs 45.2 last month); UK and Germany both had very solid PMI reports – both equity markets look very bullish compared to France, Italy, and Spain.

ASIAN MARKETS

KOSPI – continues to be a stealth leading indicator (broke TRADE and TREND supports in the last 3 weeks) and confirmed that bearish TREND overnight, down another -0.8% to 1938 (TREND resistance = 1959); China, Singapore, and Hong Kong look nothing like the KOSPI (so buy those); Shanghai Comp closed up +0.2% last night, despite the European freak-out.

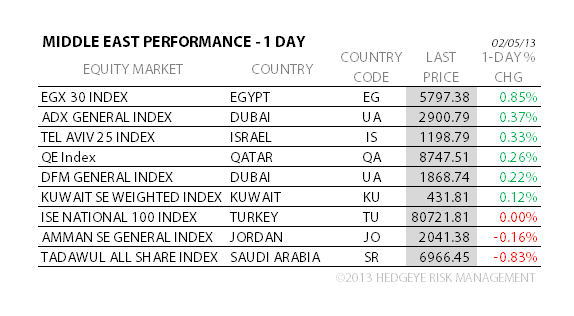

MIDDLE EAST

The Hedgeye Macro Team