TODAY’S S&P 500 SET-UP – January 17, 2013

As we look at today's setup for the S&P 500, the range is 12 points or 0.45% downside to 1466 and 0.36% upside to 1478.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.60 from 1.58

- VIX closed at 13.42 1 day percent change of -0.96%

- RUT – after making a series of all-time highs (higher-highs), the Russell2000 finally flashed a negative divergence into yesterday’s close (closing down -0.33% w/ the Nasdaq up); not a bearish signal on the margin unless confirmed today, so watch that.

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Housing Starts, Dec., est. 890k (prior 861k)

- 8:30am: Housing Starts, M/m, Dec., est. 3.3% (prior -3%)

- 8:30am: Building Permits, Dec., est. 905k (prior 900k)

- 8:30am: Init Jobless Claims, Jan. 12, est. 368k (prior 371k)

- 9:45am: Bloomberg Consumer Comfort, Jan. 13 (prior -34.4)

- 10am: Freddie Mac 30-yr mortgage

- 10am: Philadelphia Fed., Jan., est. 6.0 (prior 4.6)

- 10:30am: EIA natural gas storage change

- 11am: Fed to purchase $2.75b-$3.5b in 2020-2022 sector

- 11am: U.S. Treasury to announce plans for 10Y TIPS auction

- 12:05pm: Fed’s Lockhart speaks, Bloomberg Global Mkts Summit

GOVERNMENT:

- Senate not in session

- SEC Commissioner Gallagher at U.S. Chamber of Commerce

- Bloomberg Global Markets Summit, w/speakers Atlanta Federal Reserve President Dennis Lockhart, Paul Wolfowitz of the American Enterprise Institute, 8am

- CFPB holds hearing on mortgage-svcing underwriting rule

- FDA decisions:

- NuPathe’s migraine patch

- Decision date for Santarus, Cosmo ulcerative colitis drug

- Dept. of Veterans Affairs may award five-year, $5b technology contract; Lockheed Martin, HP, have shown interest

WHAT TO WATCH

- Boeing’s Dreamliner planes grounded by U.S.

- Japan Airlines to cancel all Boeing 787 flights Jan. 19-25; Air India, Latam Airlines will also ground its Dreamliners

- GS Yuasa may take months to complete 787 battery probe

- Citigroup, BofA among banks releasing earnings this AM

- Silver Lake close to lining up ~$15b in funds for Dell LBO

- HP approached by investment bankers about selling assets

- Rio Tinto CEO steps down, co. taking ~$14b of writedowns

- JPMorgan said to settle claim with Whale trader’s supervisor

- AB InBev unwilling to sell Modelo plant for merger approval

- Goldman Sachs issued $6b of bonds in lender’s largest offering

- EBay sales beat ests. as Donahoe pushes mobile commerce

- Trauson says Stryker offers to buy outstanding shrs at HK$7.5 each

- Wilbur Ross still plans to have IPO of Intl Automotive Components Group; declined to say when

- Deutsche Bank profited as derivative hid Monte Paschi losses

- Advanced Micro Devices ex-employees sued over trade secrets

- GM to invest $1.5b in North America factories this year

- Sun Life, Khazanah Nasional Berhad to buy CIMB Aviva for $596m

- Accordia plans to sell ~10 properties to finance shr-buyback

- Hollywood studios sued over royalties from home video sales

EARNINGS:

- Huntington Bancshares (HBAN) 5:55am, $0.17

- BB&T (BBT) 6am, $0.71

- UnitedHealth Group (UNH) 6am, $1.20

- PNC Financial Services Group (PNC) 6:30am, $1.48

- Fifth Third Bank (FITB) 6:30am, $0.41

- BlackRock (BLK) 6:30am, $3.73

- Bank of America (BAC) 7am, $0.20

- Fastenal (FAST) 7am, $0.33

- Netscout Systems (NTCT) 7:30am, $0.35

- Citigroup (C) 8am, $0.96

- Amphenol (APH) 8am, $0.90

- Intel (INTC) 4:01pm, $0.45

- Associated Banc-corp (ASBC) 4:01pm, $0.26

- American Express (AXP) 4:01pm, NA

- People’s United Financial (PBCT) 4:02pm, $0.19

- Wintrust Financial (WTFC) 4:04pm, $0.59

- Capital One Financial (COF) 4:05pm, $1.59

- Matthews International (MATW) 4:10pm, $0.42

- Xilinx (XLNX) 4:20pm, $0.37

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

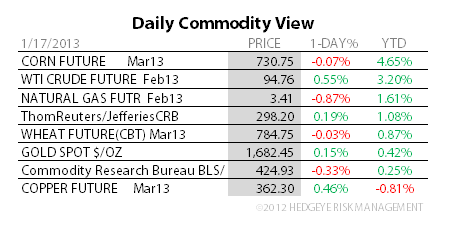

- WTI Oil Rises to Four-Month High to Cut Brent Discount to $15

- JPMorgan Tops Banks for Third Year as Loans Retreat: Commodities

- Rio CEO Albanese Steps Down as $14 Billion Writedown Looms

- Rising Crude Oil May Accelerate Growth of EU Consumer Gas Prices

- Soybeans Drop From 3-Week High on Rising South American Supplies

- Gold Poised to Decline in New York Before U.S. Economic Data

- European 2014 Power Drops to Record as Near-Term Prices Decline

- Iamgold Sees ‘Peak Gold’ Forging $2,500 Price: Corporate Canada

- Korean Oil Buyers to Halt North Sea Price Slide: Energy Markets

- Trough in China PMI, Electricity Output Aids Metals: Bull Case

- Lukoil, Iraq Agree to Cut Output Target at West Qurna-2 Field

- Cocoa Butter Stabilizes in Europe as Grinders Boost Processing

- Palm Oil Declines as India Changes Calculation of Import Taxes

- Merkel Offshore Wind-Power Dream Stalls as Vow Turns to Bluster

- Copper Rises on Speculation Chinese Economic Growth Strengthened

CURRENCIES

YEN – 2-days up, tapped immediate-term TRADE resistance (24hrs ago), then straight back down here today (-0.87%); we re-shorted the bounce and went through why in our Global Macro Themes presentation titled #QuadrillYen this wk; let us know if you want that slide deck. Interesting that Nikkei didn’t go up on Yen down overnight.

EUROPEAN MARKETS

DAX – starting to make a series of lower-highs and also leads losers in European majors this morning – Euro up +0.5% to $1.33 starting to annoy some European exporters; this is the Currency War.

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team