TODAY’S S&P 500 SET-UP – August 14, 2012

As we look at today’s set up for the S&P 500, the range is 13 points or -0.79% downside to 1393 and 0.13% upside to 1406.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 08/13 NYSE -799

- Down versus the prior day’s trading of 195

- VOLUME: on 08/13 NYSE 484.08

- Decrease versus prior day’s trading of -14.49%

- VIX: as of 08/13 was at 13.70

- Decrease versus most recent day’s trading of -7.06%

- Year-to-date decrease of -41.45%

- SPX PUT/CALL RATIO: as of 08/13 closed at 1.54

- Down from the day prior at 1.64

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: as of this morning 33

- 3-MONTH T-BILL YIELD: as of this morning 0.10%

- 10-Year: as of this morning 1.67%

- Increased from prior day’s trading of 1.66%

- YIELD CURVE: as of this morning 1.40

- Unchanged from prior day’s trading

MACRO DATA POINTS (Bloomberg Estimates)

- 7:30am: NFIB Small Business, July, est. 91.6 (prior 91.4)

- 7:45am/8:55am: ICSC/Redbook weekly retail sales

- 8:30am: Producer Price Index M/m, July, est. 0.2% (prior 0.1%)

- 8:30am: Advance Retail Sales, July, est. 0.3% (prior -0.5%)

- 10am: IBD/TIPP Economic Optimism, Aug., est. 46.9 (prior 47)

- 10am: Business Inventories, June, est. 0.2% (prior 0.3%)

- 11am: Fed to purchase $4.5b-$5.5b notes due 8/15/20-5/15/22

- 11am: U.S. Treasury announces plans for auctions of 3-mo., 6-mo., 1-yr. bills; 5-yr. TIPS

- 11:30am: U.S. to sell $25b 15-day cash management bills in addition to weekly auction of 4-wk bills

- 4:30pm: API inventories

GOVERNMENT/POLITICS:

- House/Senate not in session

- President Obama speaks in Oskaloosa, Iowa. 12:25pm, Marshalltown, Iowa. 4:45pm

- Mitt Romney wraps up 4-day bus tour in Beallsville, Ohio. Noon

- NJ Gov. Chris Christie to be keynote speaker at Republican convention, AP says

- Judge may rule this week on Pa. voter identification law

- State primary elections in Minn., Conn., Fla., Wis.

WHAT TO WATCH:

- U.S. retail sales probably rose 0.3%, 1st time in 4 mos.

- Euro-area GDP contracts 0.2% in 2Q from prior quarter

- German 2Q GDP slowed less than forecast, France avoids GDP drop

- Standard Chartered CEO visits New York, may attend hearing

- Groupon tumbles after 2Q rev. misses ests.

- Pfizer buys over-the-counter Nexium rights from AstraZeneca

- New York Fed finds 63% of small firms able to get some credit

- Doug Whitman denies trading on Polycom tips from Roomy Khan

- Peregrine CEO Wasendorf indicted on 31 false-statement counts

- Kodak, creditors extend deadline for digital patents auction

- Mercedes, Lexus, Audi luxury sedans earn poor crash-test ratings

- 13F quarterly filing deadline today

EARNINGS:

- Home Depot (HD) 6am, $0.97

- Towers Watson (TW) 6am, $1.24

- Flowers Foods (FLO) 6:26am, $0.22

- First Majestic Silver (FR CN) 7am, $0.20

- Michael Kors (KORS) 7am, $0.20

- Estee Lauder (EL) 7:30am, $0.16

- Dick’s Sporting Goods (DKS) 7:30am, $0.64

- Nationstar Mortgage Holdings (NSM) 7:30am, $0.34

- Baytex Energy (BTE CN) 8am, C$0.28

- Saks (SKS) 8am, $(0.09)

- TJX Cos (TJX) 8:34am, $0.55

- Valspar (VAL) 8:42am, $0.96

- Alacer Gold (ASR CN) 9:28am, $0.10

- Bob Evans Farms (BOBE) 4:01pm, $0.60

- JDS Uniphase (JDSU) 4:04pm, $0.12

- Jack Henry & Associates (JKHY) 4:05pm, $0.46

- Myriad Genetics (MYGN) 4:05pm, $0.34

- Boardwalk Real Estate Investment Trust (BEIu CN) 5:46pm, $0.74

- China Gold International Resources (CGG CN) Post-Mkt, NA

- HudBay Minerals (HBM CN) Post-Mkt, $0.08

- Pan American Silver (PAA CN) Post-Mkt, $0.33

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

COPPER – tough to fool the Doctor (or bond yields) here on no-volume inflation rallies – Copper continues to break-down, across durations, failing at 3.43/lb TRADE line support, again.

- Silver Hoard Near Record as Hedge-Fund Bulls Recoil: Commodities

- Oil Supplies Drop to Four-Month Low in Survey: Energy Markets

- Oil Rises for First Time in Three Days on Supply Drop Forecast

- Soybeans, Corn Advance as Drought May Persist in U.S. Midwest

- Copper Advances as Germany’s Economic Growth Exceeds Estimates

- Gold Gains in London as Weaker Dollar Spurs Investment Demand

- Robusta Coffee Falls as Indonesian Supply May Climb; Sugar Rises

- Fracking Hazards Obscured in Failure to Disclose Wells: Energy

- Lonmin Mine Violence Kills Nine, Including Two Policemen

- Philippines Agency Plans to Sell Mining Assets: Southeast Asia

- Cotton Harvest in Australia Seen Climbing to Record on Water

- Natural Gas Trades Near Six-Week Low as Cooler Weather Forecast

- Peregrine Chief Wasendorf Indicted on 31 False-Statement Counts

- Chalco Will Buy 35.3% Stake in Ningxia Power for $318 Million

- Japan Seeks to Buy 70,865 Tons of Milling Wheat in Tender

- Japan’s Executives Swelter in Solidarity to Spare Electricity

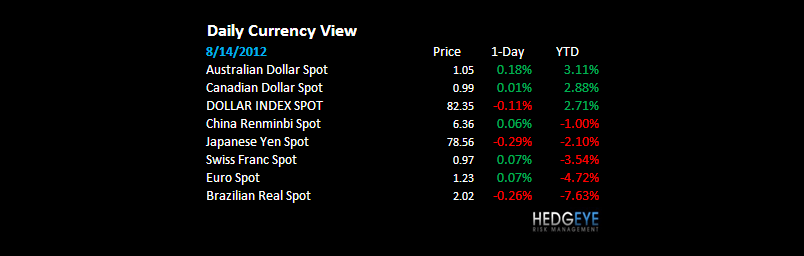

CURRENCIES

EUROPEAN MARKETS

GERMANY – some media fanfare on a “better than expected” German GDP print; in other news, Germany’s GDP falls precipitously q/q from +1.7% y/y in Q1 to +0.5% in Q2 – Growth Slowing as inflation accelerates again here in August (probably why German ZEW for AUG was a -25.5 vs -19.7 JULY).

UK – can you stay stagflation? Say it slowly as the FTSE slowly makes lower no-volume highs post the Closing Ceremonies. UK CPI rises to +2.6% y/y in July vs +2.3% in JUN, consistent with what most countries should print JULY/AUGUST. Brent Oil $114 matters.

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team