Below is a chart and brief excerpt from today’s Market Situation Report written by Tier 1 Alpha. If you’re interested in learning more about the Hedgeye-Tier 1 Alpha partnership, there’s more information here.

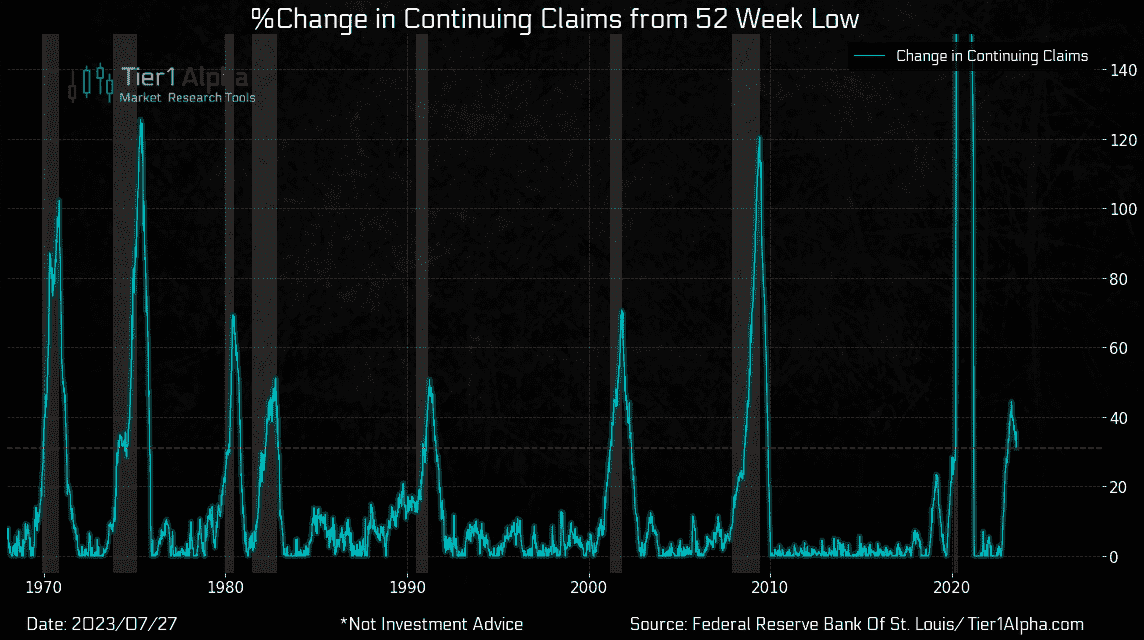

BONUS CHARTLong-term readers of the Tier 1 content know that first and foremost, we track a framework of macro, then monitor and project volatility which has a material effect on systematic inelastic flows, which, by extension, affect the underlying asset prices. The fuel for 401(k) flows primarily comes from gainfully employed individuals. If employment dwindles or slows down, the stream of incremental investment begins to dry up. Although employment is considered a lagging economic indicator, it serves as the north star from a flow perspective. As long as individuals have jobs, they continue contributing to their retirement. This is a significant oversimplification, but it explains why we place such importance on the topic of today's bonus chart. |

Typically, at this juncture, we'd likely be talking about the macro economy's disarray, but vol is down, which means markets are up, and don't overthink it. But this week's unemployment claims figures were actually promising. For the week ending July 22, initial seasonally adjusted unemployment claims stood at 221,000, showing a decrease of 7,000 from the preceding week's total of 228,000. The four-week moving average fell to 233,750 from 237,500. Additionally, the advance seasonally adjusted insured unemployment rate for the week ending July 15 dropped by 0.1 percentage points to 1.1%, and the number of insured unemployed fell by 59,000 to 1,690,000, bringing the four-week moving average down to 1,719,500.

For context, the critical threshold is 300,000 new claims per week, beyond which unemployment can start becoming a self-fulfilling prophecy, leading to accelerated joblessness. Thankfully, we're still some distance from that point. While this is only a single data point, rest assured we're staying with our stance of economic pessimism. Next week it will be back to business as usual, decelerating data and twisted metaphors to explain it.