Overview

One Medical posted disappointing 2Q21 guidance. COVID-19 testing fell off sooner than anticipated in their original guidance for 2021, which called for a drop off in COVID-19 testing in the second half of the year. We thought there would be a better handoff from COVID-19 testing to COVID-19 vaccinations along with a return to in-person care. Our app downloads and Provider Tracker line up well with 1Q21 and the 2Q21 guidance. We have seen evidence that the recovery for in-person care began mid-March and has extended through April and into early May.

Guidance

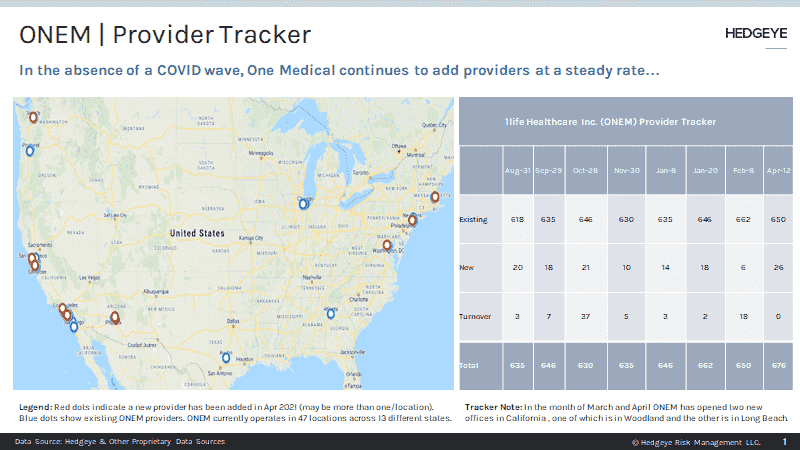

2Q21 Guidance calls for membership between 610,000 to 620,000 although the current tracker reading points to 630,000. The Provider Tracker has 676 providers through mid-April 2021, up from 635 as of November 2020, in line with the improvements in care margin we've seen (growth in providers has lagged membership growth). Revenue guidance is a range of $111MM to $118MM vs. the consensus of $117MM. Given the upside in member growth and in-person care recovery, as well as a staffing level that indicates membership levels at 625K members, we expect revenue to be at or above the upper end of guidance.

Risks

The risk for ONEM is that the hybrid care model has been adopted by a large percentage of competing physicians and that the ONEM offering is no longer as compelling to patient and employer sponsors. Also, telemedicine use is abating post-pandemic. Our view is many providers are pulling back on tele, both out of a desire to physically see their patients and difficulty maintaining a hybrid practice (this could work in ONEM's favor).

Outlook

ONEM is well-positioned to take share as they continue to expand their footprint to more markets, increase membership and relationships with Health System Partners, with Baylor, Scott & White being the latest addition. Assuming the headwind from COVID-19 testing is as contained as management suggests, the current EV/Sales multiple of 9X 2022 estimates looks attractive to us. We expect a modest beat 2Q21 will be followed by accelerating membership and revenue growth in 2H21 and into 2022.

All data available upon request. Please reach out to with any inquiries.

Thomas Tobin

Managing Director

Twitter

LinkedIn