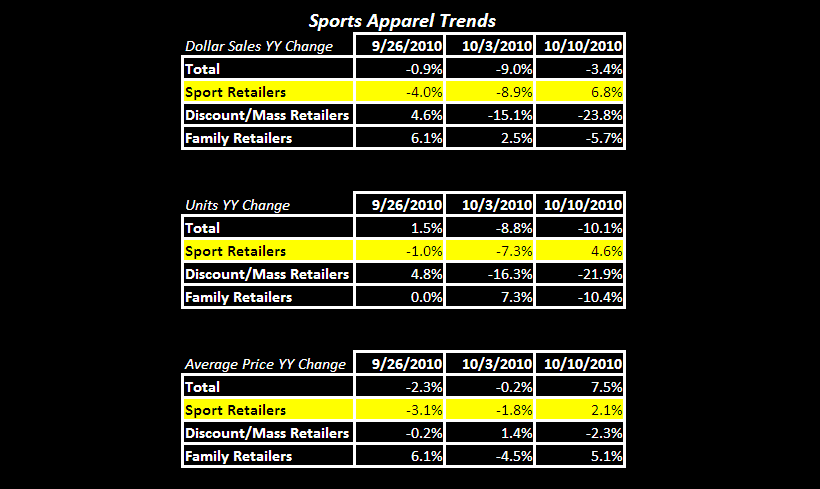

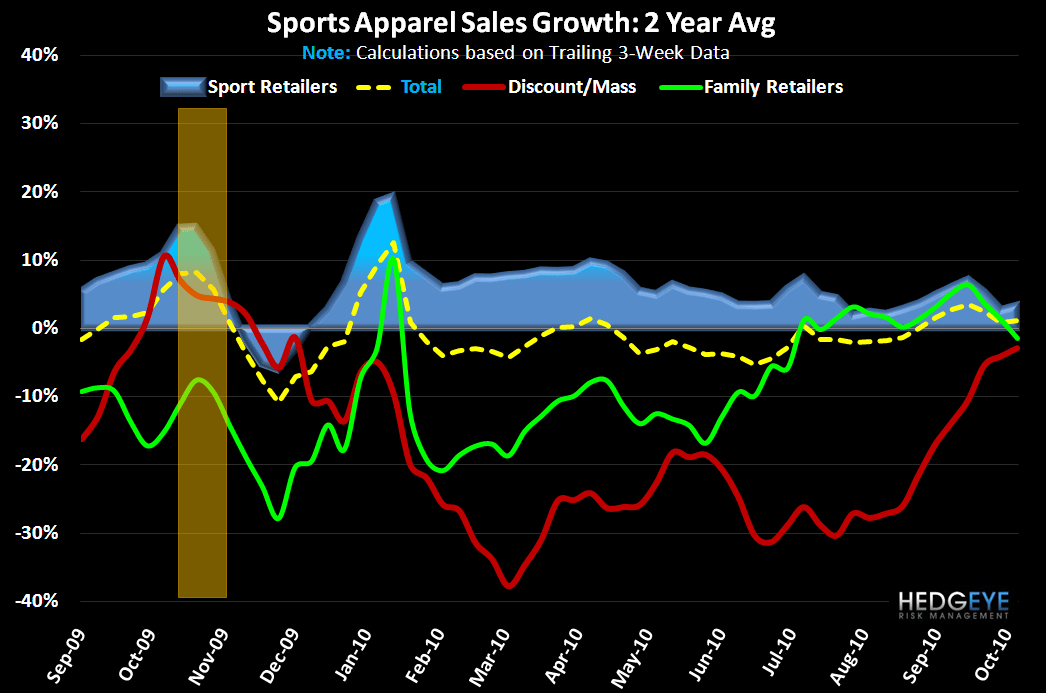

The past two weeks of sports apparel sales were down. We’d been waiting for a third week to call it a trend. It didn’t happen. The sports apparel channel staged a meaningful rebound in the latest week.

The past two weeks of sports apparel sales were down. We’d been waiting for a third week to call it a trend. It didn’t happen. The sports apparel channel staged a meaningful rebound in the latest week.

By joining our email marketing list you agree to receive marketing emails from Hedgeye. You may unsubscribe at any time by clicking the unsubscribe link in one of the emails.