The first 10 days of Oct were off the charts in Macau. Normalizing the rest of the month produces full month estimated growth of 63-72% YoY growth.

Macau produced HK$8.6 billion in table revenues in the first 10 days of October. Of course, while stunning, this number was impacted by the Golden Week celebration. After normalizing the rest of the month and adding slot revenue, we arrive at a full month revenue projection of $20-21 billion or YoY growth of 63-72%. This seems stronger than general consensus.

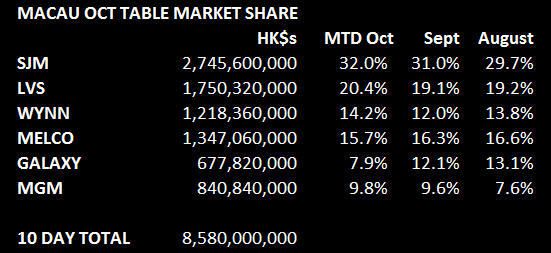

In the chart below, we list the market shares for the first 10 days of the month. We have been hearing Wynn’s hold percentage has been running high the last few weeks and that seems to be corroborated in its October market share. While 14.2% is better than the low hold impacted September at 12.0%, October is so far only in-line with its substandard summer share.

LVS share moved over the 20% mark thus far in October. We suspect The Venetian’s VIP push is paying off. The property appears to be advancing commissions to junkets for up to two months. Another positive is MPEL, which is on its way for a fourth straight month of above trend market share. MPEL has been even more aggressive with junket credit than Venetian and the property’s Mass business continues to ramp. Do these guys finally have their act together? We may have to conclude that they do.

As expected, MGM’s share continues to strengthen as it readies itself for the IPO. MGM has been as aggressive as MPEL in advancing commissions on a 3-4 month basis. In terms of losers, it looks Galaxy is taking one on the chin. We’ve heard they have been mauled on the tables.