Conclusion: The Street is mixed on BWLD, but the consensus EPS expectations seem low. I am currently modeling FY10 EPS of $2.14 versus the street at $2.08 with more of the upside falling in 4Q10.

I estimate EPS for 3Q10E and 4Q10E of $0.45 (versus the Street at $0.43) and $0.60 (versus the street at $0.56) respectively. The primary risk to my 4Q estimate is the ability of the industry to maintain the current trend of posting improved comparable-store sales results on a two-year average basis.

Reasons for upside:

Company comparable-store sales were up 2.2% in July versus +1.2% in the year-ago period, which implies a 30 bp improvement in two-year average trends since the end of 2Q10 (and trends came in much better-than-expected during 2Q10 after turning positive in June from -3.7% in April).

While this data point for July is encouraging, it obviously does not make a quarter. Industry trends, on average, have improved on a one and two-year basis since early in the summer. Comparisons become easier for BWLD for the remainder of the quarter as 3Q09 comparable-store sales came in at +0.8% (after being up 1.2% in the first four weeks of the quarter).

I am modeling +3.0% company SSS for 3Q10, which implies a nearly 60 bp acceleration in 2-year average trends from the prior quarter.

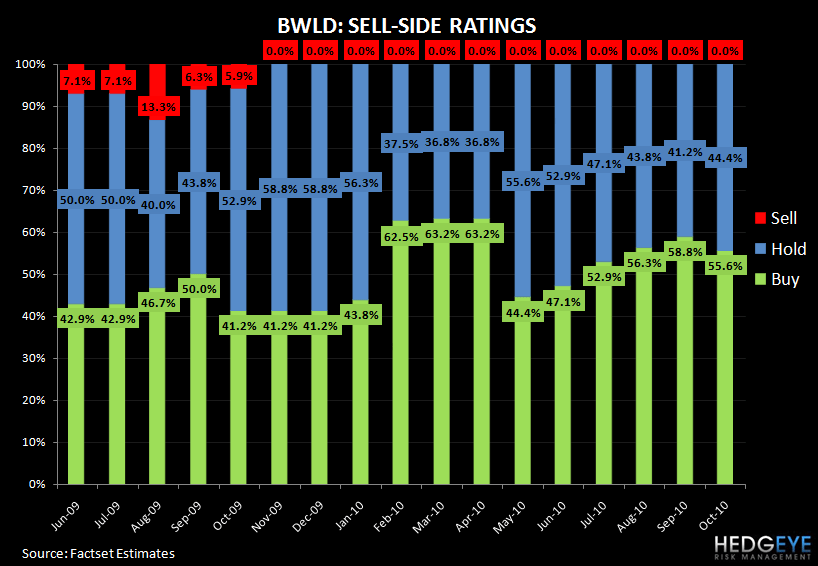

The consensus says: The chart below shows the current sentiment surrounding the stock. Positive ratings (“BUY” and “OUTPERFORM”) are at 55.6%, down from the peak of 63.2% in March, and up from the low of 44.4% in May.

COGS: Chicken wing prices were down nearly 11% in 2Q10. Based on two-month number given for 3Q10 of $1.41/lb, wing costs will be down closer to 16% in 3Q10 versus the $1.67/lb cost in 3Q09. The year-over-year benefit should be even greater in 4Q10 as the company is lapping its highest price paid in 4Q09 of $1.78/lb. This, combined with same-store sales trends that should improve on a 2-year average basis, should drive the bulk of the year-over-year restaurant-level margin growth in 2H10.

Labor: Management guided to slight year-over-year leverage in 3Q10.

Offsets: Restaurant operating expenses are moving higher in 2H10 due to additional pay-per-view TV programming costs and an expected 11% increase in media spending in 3Q and 4Q.

Preopening expenses will be higher year-over-year as the company is expected to open 13 units in 3Q10 versus 5 in 3Q09 and 14 units in 4Q10 versus 12 in 4Q09.

3Q10 EPS Growth:

Although management guided to 20% EPS growth for the full year, they said on the last earnings call that it may not achieve that target in each quarter of the year and they mentioned the expected higher level of preopening expense in 3Q10.

This, along with the fact that the company is lapping its highest quarter of YOY growth from FY09, leads me to think that the company will post its lowest year-over-year growth in 3Q10. My 3Q10 EPS estimate assumes nearly 20% EPS growth after 23% and 31% growth in 1Q and 2Q, respectively.

I think the 49% reported EPS growth in 3Q09 relative to the 24% full-year growth was partly a function of comparisons. The company’s 3Q08 EPS grew only 6% versus 24% for FY08 overall.

SSS actually slowed sharply in 3Q09 on a one-year and two-year basis and chicken wing prices were up 43% during the quarter.

Preopening expenses, however, were much lower YOY in 3Q09 and drove a bulk of the EPS growth as the company only opened 5 units in 3Q09 relative to 18 in 3Q08. If you make 3Q09 preopening expense equal to the 3Q08 level, EPS would have only been up closer to 20%.

Summary:

Based on our restaurant sigma chart, it looks as though the company has a good chance of remaining in the “Nirvana” quadrant (positive same-store sales growth and positive restaurant-level margin growth) for the next several quarters if comp trends hold steady (that is obviously a big if). BWLD needs positive comp growth to offset the growth-related costs inherent in its P&L and comps trends definitely improved more than I was expecting during the second quarter. It will be important to see if BWLD can maintain this top-line momentum.

Longer-term thesis:

I continue to think the company is growing too fast. I consider return on incremental invested capital to be the best metric to look at when considering the sustainability of a company’s unit growth plans. After declining in 2009, returns look to be recovering in 2010 to about 30%, which is impressive. Based on my current estimates (I think it will be harder for the company to achieve 20% EPS growth in FY11), I would expect returns, however, to fall off again in 2011 to a low double-digit range. Although this still implies positive returns for 2011, I have found that the absolute direction of the trend in returns is the more important indicator of future trends and, ultimately, stock performance.

Howard Penney

Managing Director