“The lofty pine is oftenest shaken by the winds; high towers fall with a heavier crash; and the lightning strikes the highest mountain.”

-Horace

I haven’t considered a heightening probability of a US stock market crash in an Early Look note since 2008. I’ll go there this morning.

Before I look forward, allow me to take a step back. To fully appreciate the risk that is getting baked into this US stock market cake, we should respect history’s lessons. If you believe that the professional politicians of the Fiat Republics of modern day America and Japan have as much to lose as those in the Roman Empire did in 49BC, you’ll find my using a quote from the leading Roman lyric poet of that era appropriate.

I’m not a poet. I’m a Risk Manager. In probability speak, I am registering signals in my global macro risk management model that would consider an abrupt 1-3 day US stock market crash in October probable. To be clear, I’m not saying it’s likely – but I am saying it’s probable. There is a difference.

Probable is proactively predictable. Likely would be a better than 50% chance. What I see here is a 33% chance this happens, so let’s strap the accountability pants on and take a walk down that path. For a Heavier Crash to occur during a compressed period of time, we still need a few more things to happen:

- We need to see the SP500 get squeezed one more time in the next few weeks to a price north of 1164.

- We need to see volatility (VIX) get oversold towards 20.

- We need to continue to see the world’s said “reserve currency” lose its credibility.

The bad news is that all 3 of these factors are already in motion, big time (since late August the SP500 is +10%, the VIX is down over -20%, and the US Dollar has been crushed to lower-intermediate-term-lows). If these 3 factors continue to travel the path of least resistance (SP500 up, VIX down, and US Dollar debauched), we could have a serious short term problem.

Measuring time and space is a critical aspect of my profession. As a chaos theorist, I don’t expect to be taken seriously by the gurus of buying cheap P/E’s, nor do I want to be. If the Ken Fishers of the world didn’t realize they were going to get smoked in 2008, I don’t see why they’d see it coming now. Evolving the risk management process is a dynamic exercise in and of itself. We all need to change as the market’s ecosystem does.

So what would a Heavier Crash look and feel like?

- The most probable scenario that the perma-bulls would consider improbable is a 1-3 day correction on the order of -5.4% to -6.9%.

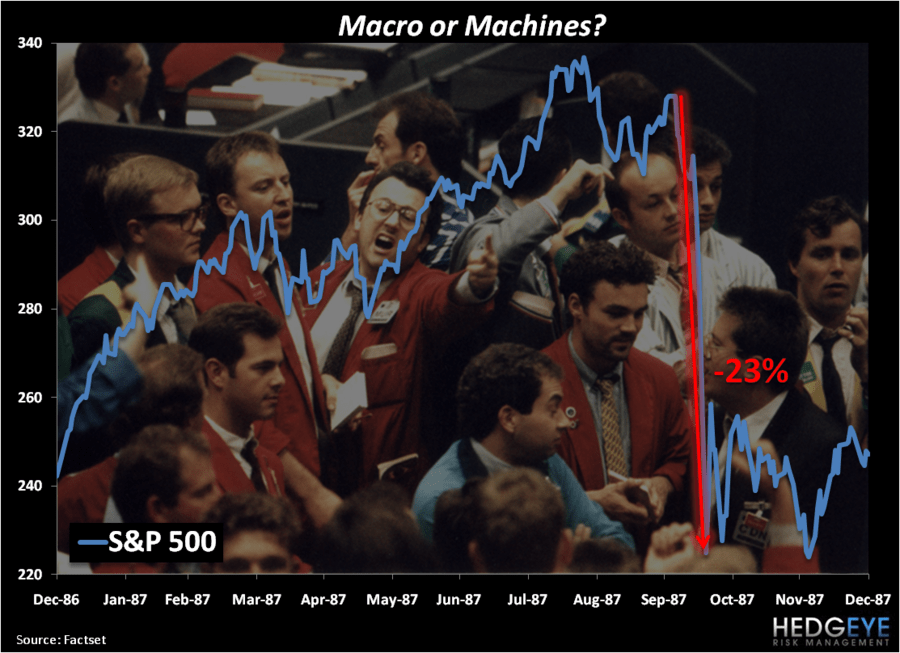

- The least probable scenario in my model is an October 1987 type day (down -23%); I’d still consider that improbable, for now.

Now isn’t that a correction rather than a crash? If we eliminated that one little critter that the market calls expectations, yes, it might be. But relative to the expectations in this market today (this morning’s Bullish to Bearish Survey from Institutional Investor is seeing a +2400 basis point swing to the bullish side since the week US stocks closed at their late August lows), this could feel like a Heavier Crash than it might be considered in nominal terms.

What immediate term bearish data and price information in the land of global interconnectedness am I staring at in my notebook?

- The SP500 is teetering on a critical line of support (my intermediate term TREND line of 1144); any slicing through that line on accelerating volume puts this bearish scenario back in play (again, that’s not what I would consider tail risk – it’s a probability to manage risk around)

- Volatility (VIX) continues to trade with an extremely high inverse correlation to the SP500 with TREND line support for the VIX at 20.96

- The SP500 is actually down for 4 out of the last 6 trading days and the market’s breadth is deteriorating

- Financials (XLF) remain the only sector in the SP500 (of the 9 we model top-down daily) that’s bearish from a TREND perspective

- Yield Spread (10s to 2s) continues to compress this week versus last and remains a bearish headwind for US Financial spreads and earnings

- High Yield is trading within 7bps of its April 2010 highs at 8.25%; this is a contrarian indicator, big time

- Levered Loan Index at 15.13 is 5bps away from its late April early May highs; another contrarian (bearish) indicator for equities

- Case-Shiller Prices (JUL) rollover again sequentially (month-over-month) and we forecast the October 26th Case-Shiller report to be a bomb

- US Consumer confidence comes in at a bomb, 48.5 for SEP versus 53.2 AUG, despite CNBC cheering the stock market higher

- “Republican House” finds its way onto the cover of Barron’s = consensus bullish catalyst now

- M&A rumors haven’t been this frothy since September of 2007 (we’ve counted 67 alleged “takeouts” that haven’t occurred)

- US Dollar Index continues to burn at the stake of QE hope; down now for the 15th of the last 18 weeks and Washington doesn’t care

- US Treasury Yields are in a Bearish Formation across the curve (2yr yield TRADE resist = 0.51%) = bearish signal for US economic growth

- Chinese stocks have closed down for 6 out of the last 8 days and the Shanghai Composite is now broken on immediate term TRADE duration

- Japanese stocks continue to be the armpit that is long term QE; Nikkei down 3 of last 5 days and down -10% for 2010 to-date

- Japanese exports (AUG) hammered sequentially down to +15.3% y/y vs +23.5% y/y in JUL; expect more Fiat Fool intervention from here

- Japan’s Bureaucrats calling for another 4.6 TRILLION Yen in stimulus and proposing to pay for it by raising taxes this time?

- Spain’s IBEX is breaking its immediate term TRADE line this morning (first time in months; support line could become resistance at 10,501)

- Italy’s CDS continues to push higher at 205bps and remains the country with the most downside relative to consensus (we’re short EWI)

- European CDS continues to push wider on the heels of Greek Equities getting smoked (down -13% since 1st week of September with SPY +9%)

- Russian deficit risk heightening in the face of Medvedev firing the longstanding (18 year) mayor of Moscow

- Romania’s Interior Minister resigns in the face of austerity implementation

- Sri Lanka is now issuing sovereign debt ($6B worth) and markets there are cheering it on?

- Dubai says “we are back”

Acknowledging that there are plenty of bullish data points on the other side of this ‘QE is going to save us all’ expectation (there better be with the SP500 up +9.6% in a straight line from its August 26th low), I can only count 15 of consequence this morning - and that’s less than what I’d need to see for me not to call for a buckling of your chinstraps.

Horace’s lightening has already struck some of the highest mountains of buy-side and sell-side exposures in the last 3 years, but the lofty pines of professional politicians and the highest ivory towers of academic dogma that support them are still in for their heaviest crash yet.

My immediate term support and resistance lines for the SP500 are now 1136 and 1155, respectively. It’s not October yet. The SP500 hasn’t touched 1164 yet. So I’m not short the SP500 yet. Measuring time, space, and probabilities matter.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer

This note was originally published September 29, 2010 at 08:01am ET