CoD driving strong Mass and VIP business. We’re well above the Street.

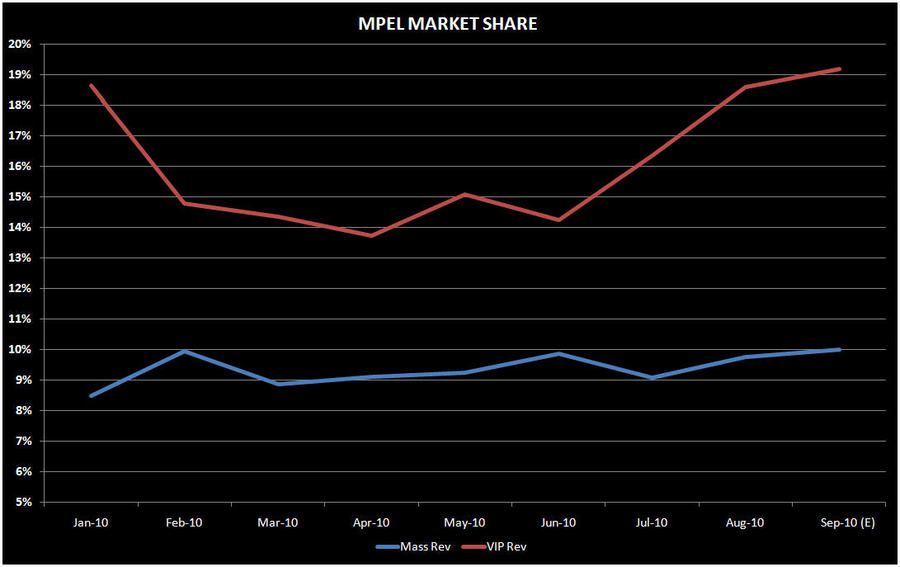

The “crew that couldn’t get their act together” appears to have gotten their act together. We first highlighted the potential for sustained market share gains in late July. MPEL gained significant share that month, gained even more in August, and is poised to take another step forward in September. Gaining market share while the market grows 40-70% is impressive, particularly for a company held in such low esteem by the investment community.

Given the strong market growth in Macau this quarter as well as an estimated 250bp sequential increase in market share to 16.0%, we think MPEL can post EBITDA of $120 million. Consensus is only $100 million. Our Q4 estimate of $92 million is also higher than the Street at $88 million.

City of Dreams drives most of the company’s revenues and profits and has been the market share driver. So what’s driving the market share gains? On the Mass side, we believe the reconfiguration of the slot floor earlier this year has created a busier and more exciting feel. Too much space can be a bad thing for a casino. Also, management was very promotional in the first half, particularly in Q2, which seems to be paying dividends.

On the VIP side where the market share gains have been more pronounced, aggressive junket commissions have certainly helped although we do not think Q3 commission rates and VIP promotional activity have increased. Rather, we think MPEL may be advancing junket commissions for 3-4 months. Essentially, they are providing more credit to the junkets. This should have the impact of better margins than a straight commission increase, but may create longer term credit risk. For now, we are not worried.

While 16% market share was probably aided by high hold, particularly in September, we think a 15%+ share is probably sustainable and is likely above investor expectations. Sure the stock has moved up significantly off its sub $4 in late July when we first turned positive on the name. However, MPEL remains discounted to the group--10.5x 2011 EV/EBITDA versus 12.5-14.5x, and EBITDA estimates could go higher. There is still 25% upside to the low end of that range, without the benefit of higher numbers.