Guess what folks? Futures matter again. The 14% growth # is completely consistent with our call on a multi-year business acceleration. But let’s not turn a blind eye to the math. Weighted channel growth is 3% -- 4% tops. This 10% from share gain NEEDS to continue with the stock up here. (Note: if images are not coming through -- let us know and we can send out the raw analysis).

Despite being a big bull for reasons that I still think other bulls don’t appreciate, I noted last week that those looking to manage risk around the quarter at least needed to acknowledge the sky-high expectations on both sides of the Street. In other words, ‘at least play it safe and take out your umbrella if there’s rain in the forecast.’

So what did Nike do? They ‘pulled a Nike’ and toasted the high-end of expectations. If there’s any one notable takeaway after packaging up all the commentary, Q&A and financials, it’s that the financial and human resource pain trade inside of Nike a year and a half ago is starting to pay off. Global demand is reaccelerating; a) in both footwear AND apparel, and b) across all the company’s new consumer categories. This has legs, folks. See our Nike Black Book from earlier this year for more details.

That said, the quarter was less than perfect, and there are a few items that raise question marks. These might seem like nit picks, but when the stock trades up after expectations were already so high, we need to nit pick.

a) The quality of the beat ($1.14 vs. our $1.08 and the Street’s buck) was not outstanding. Revenue missed our model by 2-points and the Street’s by a point. Blame it on FX – as the business remains solid on a constant-currency basis – but FX is KNOWN, so there should not be any surprises there.

b) Gross margins looked solid – right in line with our model and above NKE’s sandbag.

c) But the big delta was in SG&A, where operating overhead was flat on a -4.8% comp last year.

d) So the bottom line is that revenue delta cost $0.02 relative to our $1.08, and an unsustainable SG&A rate added up for $0.08. So overall…sales were +8%, EBIT was +11% and EPS was +10% (higher tax rate offset repo).

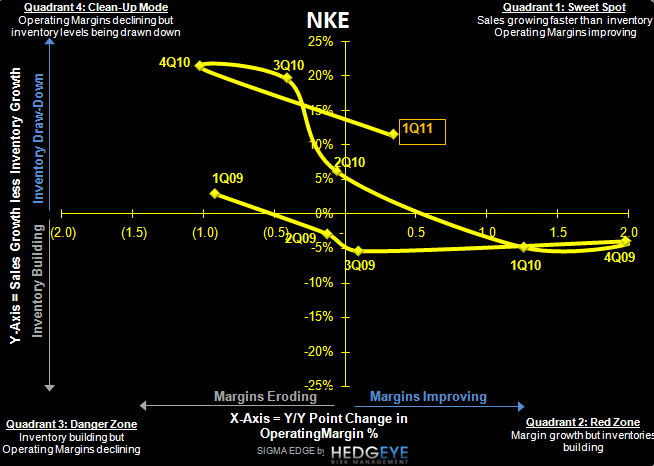

e) Sales/inventory spread and SIGMA position are good, but eroded 1,000 basis points sequentially. Not a disaster, but notable.

Back to the Future(s)

That brings me to the title of this note. Friday morning Keith and I were discussing the numbers. I took a few minutes and gave the plusses and minuses of the financials – noting the low quality relative to expectations. Then I got to the 14% North American futures number, and he looked at me like I had two heads and chuckled. He was probably thinking something like “Hello! Anybody home McFly? Think McFly, Think!”

That’s when it hit me… Sell side analysts and people inside the company – of which I was both – have it engrained in them that ‘futures really don’t matter that much anymore.’ That, of course, is a product of a time period where NKE would trade on the US business and nothing else. Even when US Footwear got to be less than 1/3 of sales – the US footwear number is what would drive the stock, and would drive the company (and the sell side) batty. Over the past few years, the market finally ‘got it’ that there’s more to this business than the US. But today, Mr. Market is definitely reverting to his former view as to what’s important. The trader in Keith got this in about 3 seconds flat. It took my inner McFly a couple hours to get ‘Back to the Futures’.

NOTE: Though unrelated, Nike secured a patent last quarter for a self-inflating shoe. Remind you of anything?

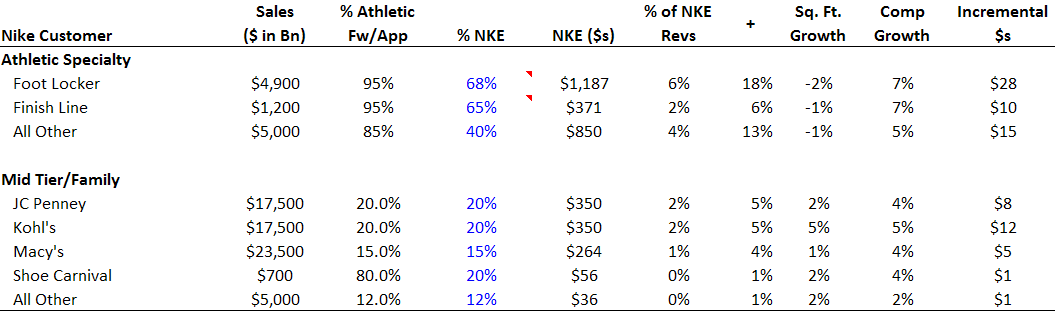

That leads to the 14% NA futures number. Let’s put things into perspective. 14% growth over the next 2 quarters is the equivalent of adding $289mm in new business (assuming that 85% of the base is on the Futures program). This number annualized is bigger than the ENTIRE US BUSINESS for over 90% of the footwear brands in the world. The good news is that the number is balanced over footwear and apparel. That definitely makes this number more easily digestible.

But is anyone watching the comp, square footage growth, and inventory trends of the channels that sell Nike’s product? Yes, they’ve picked up recently – no doubt. They’re also generally light on inventory. And yes, a better R&D cycle should help as well. But keep in mind that Adi and Reebok are no longer share donors (after losing 11 points of share—from 18% to 7% -- over 5 years) and casual brands like Skechers are giving it a go in the performance category.

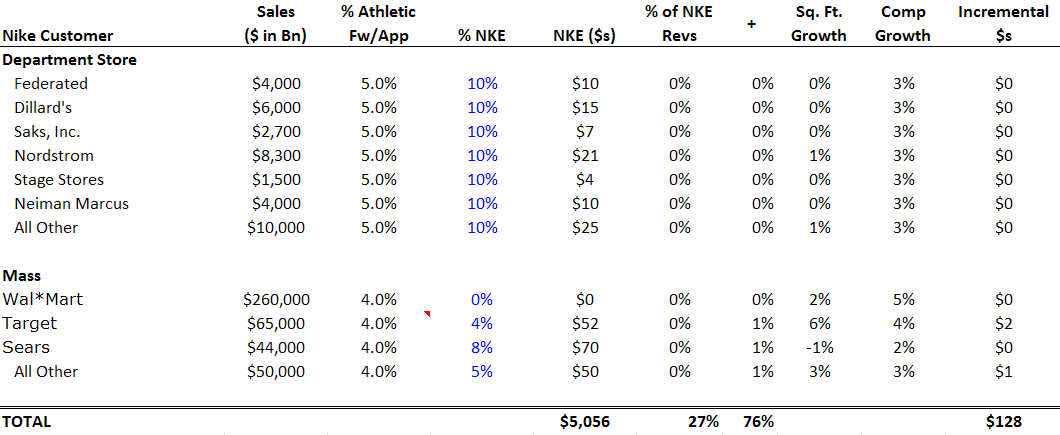

Precise quantification of this order number is tough. But here’s our best crack. When we add up comp and square footage growth by customer and by channel, we get to about $128m top line growth for the YEAR – or about 2.5%. Now…this excludes growth in Nike retail and Nike.com – both of which should take the aggregate growth rate on a reported basis for Nike up by another 2-3 points. So what we need is to justify doubling this growth rate again due to market share gains in order to get to 14%.

*Hedgeye Estimates

Right now, this is absolutely, positively, 100% realistic. But with Nike’s sales/inventory spread ticking down on the margin, and sales in the channel (incl square footage) supporting 3% growth, we need to sustain a steep trajectory in share gains to keep the halo on the US futures number.

It pains me to even write this, because our long-term call is so much bigger than the US. But Mr. Market just told us that local share matters again. We’re going to have to keep our Hedgeyes on this into the fall.