“Lacking much experience with this option, we do not have very precise knowledge of the quantitative effect of changes in our holdings.”

–Ben Bernanke

While it’s entertaining, it’s also quite frightening to watch the same failed policy makers and the pundits that pander to them fundamentally believe that they understand exactly how this “QE” experiment is going to play out. Fortunately, Ben Bernanke is not one of those people.

Now that they’ve been liberated from Larry Summers assuring them that he knows exactly what he is doing, here’s a simple risk management exercise for Groupthink Inc in Washington today.

Consider this part of your post Summers rehab – baby steps guys:

- Re-read the aforementioned quote

- Then count how many times you hear the media say QE today

- Then re-read that quote again before you go to bed tonight

Now we don’t purport to have “precise knowledge of the quantitative easing effects” on the US economy either. Einstein himself said that “if we knew what we were doing, it wouldn’t be called research, would it?” That said, our fundamental macro research does point us toward Japan’s experiment with QE as being an unsuccessful one.

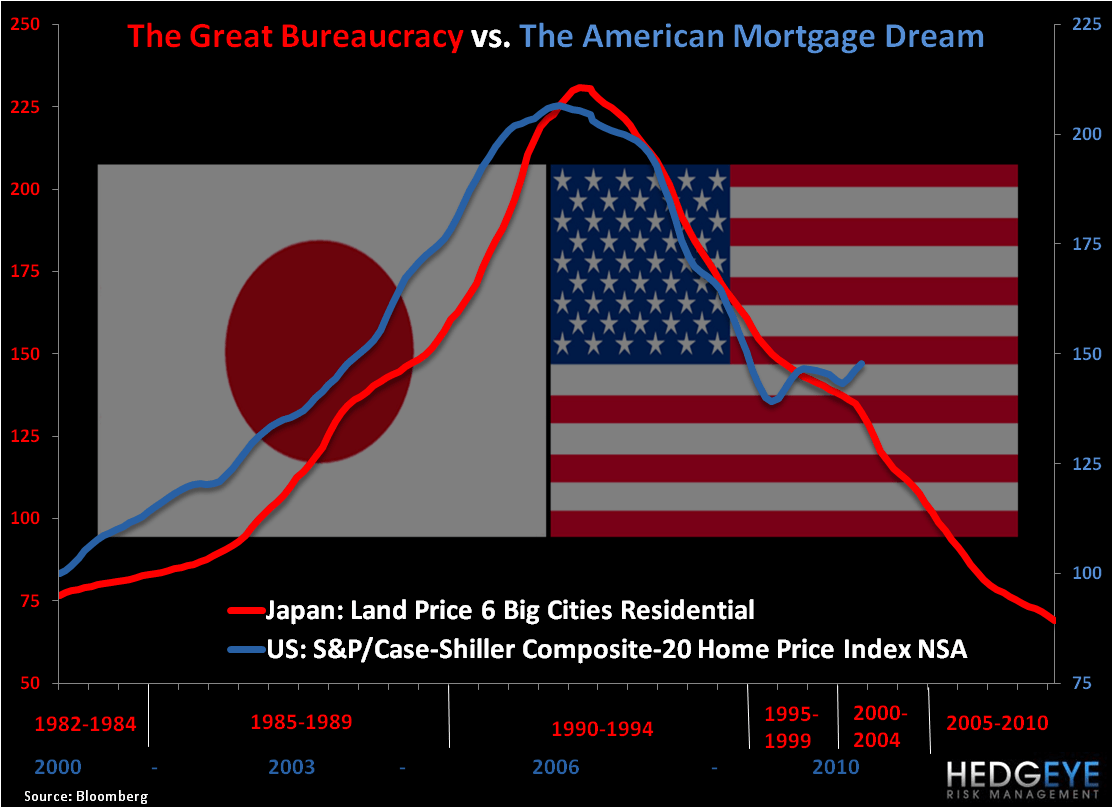

While the United States of America in 2010 may not “precisely” be Japan of 1997, there are plenty of similarities developing in terms of Big Bureaucratic Government resolve. If you have any recovering friends from Groupthink Inc who make it past the remedial exercise above, please send them our Chart of The Day (see below) that overlays the Japanese real estate bubble with ours. *Note the duration.

For really advanced stage rehabilitation from the Academic Dogma that’s been driving Ben Bernanke and Larry Summers policy making decisions, you can overlay Japanese Government Bonds Yields (JGBees) with US Treasury Yields (QE Mees). While we don’t have “precise” measurements on how low the rate-of-return on America’s aging population’s hard earning savings accounts can go, we do see ZERO percent as a credible gravitational force.

We’ll be expanding our Japanese research effort in Q4, but if you’d like a taste of the contrarian Hedgeye cool-aid, please send an email to sales@hedgeye.com and we’ll get you a solid report from our Hedgeye Jedi, Darius Dale, who punched out a not yesterday titled, “Japanese Pensions: Risks to the Global Economy.”

Post-rehab students of objective macro-economic research have learned that the Japanese demographic curve started to age before America’s baby boomers did. Importantly, this doesn’t mean America can’t age in due course. Advanced research studies on campus here in New Haven have revealed that time, as a risk management factor, is actually quite hard to reverse.

All the while (alongside time), there’s this other little research critter we monitor here at Hedgeye called price. Again, this is getting into the really advanced stuff folks, so try to “dumb this down” if you attempt to explain this to anyone in Congress, but TIME and PRICE are significant factors in a modern day risk manager’s search for more “precise” knowledge about future probabilities.

Now let’s go to the future state - if we really want to dial up Washington’s fully loaded rehab research engine we gotta go where Heli-Ben has never gone before. As Buzz Lightyear would say, “to infinity and beyond” – the cosmic galaxy of the hedgie universe – REAL-TIME PRICES!

I know, I know… this is deep. But let’s suspend disbelief for a moment and take a gander into the cosmos of Hedgeye REAL-TIME PRICE research and look at what we see:

1. Currencies: The US Dollar is down for the 14th week out of the last 17, breaking to lower-lows that we havn’t seen since mid-April when chaos theorists in New Haven said something about May Showers. Sounds serious, because when you Burn The Buck at the stake, it starts to become a very bad thing - importing crazy critters that Bernanke has never seen (like inflation, shhh…).

2. Bond Yields: US Treasury yields are getting pulverized again this morning on the short end of the curve, with 2-year yields in America hitting their lowest levels ever. Ever, of course, is a long time… and while we can’t tell you “precisely” how poorly this ends for a lot of people in this country, we can assure you this ended poorly in Japan.

3. Equities: US stocks have backed off of the line I said I was going to walk this week (1144 in the SP500), leaving our intermediate term TREND line of resistance intact. Whether or not the perma-bulls want to admit that lower-highs in everything US equities since 2007’s leverage-cycle-peak matter or not is something that Nikkei bulls in Japan have been powdered by since Gordon Gekko’s last 1980’s dance.

QE ain’t for me.

My immediate term TRADE lines of support and resistance for the SP500 are now 1127 and 1146, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer

This note was originally published at 7:59am, this morning September 23, 2010. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK and PORTFOLIO IDEAS in real-time.