Costs are too much to absorb, according to CEO Howard Schultz.

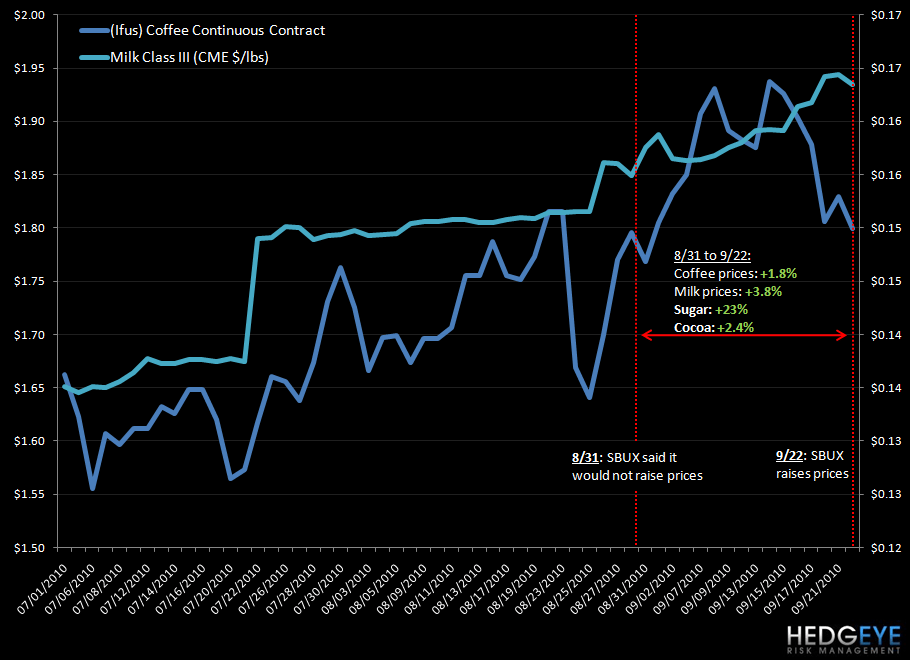

August 31, 2010: SBUX says it has no plans to raises prices, even though it expects higher coffee costs to weaken its profits in the upcoming fiscal year. Management said it is able to maintain its current prices because it has long-term relationships with farmers, traders and co-ops in multiple coffee-growing regions. Importantly, it also has bought the majority of its coffee for its upcoming fiscal year. No change in the fiscal 2011 EPS guidance of $1.36 to $1.41, which factors in an expected $0.04 hit from higher coffee prices.

September 21, 2010: At a conference in LA, CEO Howard Schultz predicted a “tough” 2011, with conditions improving the following year. At the time I thought this was a very odd comment. What was going to make FY2011 so tough given how strong sales are? Or have they slowed?

September 22, 2010: From the SBUX press release, SBUX is raising some prices “due to the recent dramatic increases in the price of green arabica coffee, currently close to a 13-year high, as well as significant volatility in the price of other key raw ingredients, including dairy, sugar and cocoa.”

So what had changed between late August and now?

- Coffee is up 1.8%

- Milk is up 3.8%

- Sugar is up 23.1%

- Cocoa is up 2.4%

While we think same-store sales have slowed in 4Q10 on a one-year basis, the company reiterated its comfort level with current guidance, as management affirmed its forecast for the current fiscal year.

Going into 2011, expectations will remain high as the company’s FY11 same-store sales guidance of low-to-mid single digit growth assumes a fairly steady improvement in two-year trends. For reference, +1% same-store sales growth in the U.S. in FY11 would imply a 350bp improvement in two-year average trends from FY10 (assuming 6.5% growth for FY10). I think same-store sales and margin growth will continue to materialize in FY11 but the rate of growth will slow and the company’s ability to continue to surprise to the upside from both top-line and bottom-line perspectives will likely diminish.

Howard Penney

Managing Director