Full-year same-store sales and commodity guidance seem to be at risk.

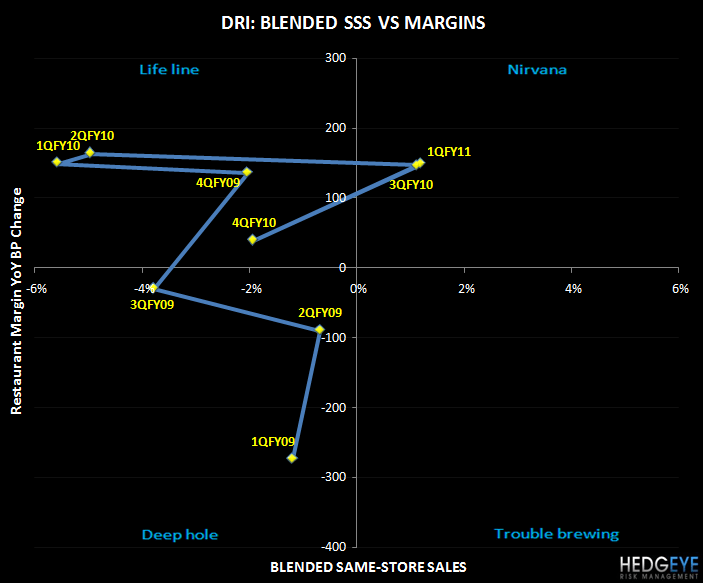

DRI reported a relatively strong fiscal first quarter with blended same-store sales up 1.1% and EBIT margin improving nearly 130 bps YOY. One area of continued concern, however, stems from performance at Red Lobster, which lagged the industry benchmark as measured by Malcolm Knapp by 170 bps during the quarter on a reported basis and by 70 bps when you adjust for the timing mismatch around the concept’s Endless Shrimp promotion. During the prior quarter, Red Lobster lagged the industry by only 30 bps.

The company attributed its weaker-than-expected results at Red Lobster to ineffective promotional tactics in the quarter. Specifically, management referred to its June promotion, which it said did not offer a compelling enough dish and its July promotion, which featured too high of a price point at $14.99. Helping to offset the weakness at Red Lobster were same-store sales trends that continued to get better at LongHorn and improved trends at the Olive Garden after reporting a sales shortfall during fiscal 4Q10.

The two biggest risks to Darden’s numbers this year stem from the company’s ability to achieve its full-year blended same-store sales growth guidance of +2-3% and rising commodity costs. There were a lot of questions on the call about the company’s ability to meet its comparable sales targets for the year after coming in below the full-year guided range during the first quarter when the company was lapping its easiest comparison from the prior year. This was a concern I had going into the quarter; full-year comp guidance seems aggressive as it implies a sharp improvement in two-year average trends. And, given the fact that Red Lobster’s top-line trends decelerated even further during the quarter on a two-year average basis, even when you adjust for the promotional timing issue, this full-year guidance seems even less obtainable.

Management justified its comp guidance and the implied sequential improvement by saying that the industry is recovering faster than it had expected. Excluding Darden, the industry, as measured by Malcolm Knapp, reported flat same-store sales during DRI’s fiscal first quarter, up from -1.4% in the prior quarter. On a two-year average basis, this implies a 20 bp improvement making fiscal 1Q11 the fourth consecutive quarter of sequentially better industry trends on a one-year and two-year basis. This sequential improvement in industry comps during the quarter is, in fact, better than I would have expected but I don’t think it guarantees that trends will continue to get better from here.

Management highlighted recent GDP growth, as opposed to decline, and its correlation to consumer spending as one reason why industry trends should continue to improve. I would argue, however, that although GDP growth may be positive this year versus negative last year, the rate of growth is decelerating and the Hedgeye expectation is for it to soften further in 2H10, which on the margin will be bad for the economic recovery and will limit the improvement in industry trends. Even if industry comp trends do improve to -1%, as management guided to, DRI’s 2-3% blended same-store sales guidance assumes 300 to 400 bps of outperformance during the year after reporting only 110 bps of outperformance during fiscal 1Q11. Red Lobster’s softening trends will make it that much harder to achieve such a wide gap to Knapp. Management did say that with industry trends improving faster than expected, driven primarily by higher average check growth, that it expects Darden’s full-year gap to Knapp to come in slightly narrower than it initially expected. That being said, its guidance still assumes sequentially better industry trends and continued outperformance.

During fiscal 1Q11, operating margin improved nearly 130 bps YOY. The company achieved better leverage during the quarter on the food and beverage, labor and restaurant expense lines that I had anticipated. Management said that positive comp growth, of course, helped in that regard along with the company’s cost saving initiatives related to automating its supply chain, centralizing facilities management and driving sustainability to reduce water and energy usage.

Lower food and beverage costs as a percentage of sales drove the most upside relative to my numbers, which management attributed largely to lower commodity costs. Management expects to benefit from a similar level of food cost favorability during 2Q, but then expects food costs to be up about 0.5% in the back half of the year. There is little risk to the company’s 2Q food cost outlook as Darden is locked in on about 90% of its needs through the end of calendar 2010. Right now, the company is only contracted for about 40% of its commodity needs for fiscal 2H11. Although management believes that current levels of some commodities it uses are unsustainable and is therefore, not yet locked in, this commodity exposure poses a risk to Darden’s 2H11 numbers.

Howard Penney

Managing Director