Back in July, we decided to map out where the restaurant companies were in terms of their positions on the SIGMA chart. Changes in top-line growth and margin expansion/contraction clearly illustrate key operational trends in each company. Tracking these changes as the quarters roll over, and the different valuation multiples that are assigned companies as trends change, offers valuable insight.

All restaurant companies want to live in Nirvana, with same-store sales positive and margins growing on a year-over-year basis. Not all of the restaurant companies in Nirvana are there for the same reasons; some companies may be lapping easy comparisons, driving comps entirely by pricing or thanks to a temporary but very favorable cost environment. In these cases, such companies will not sustain their positions in the Nirvana quadrant.

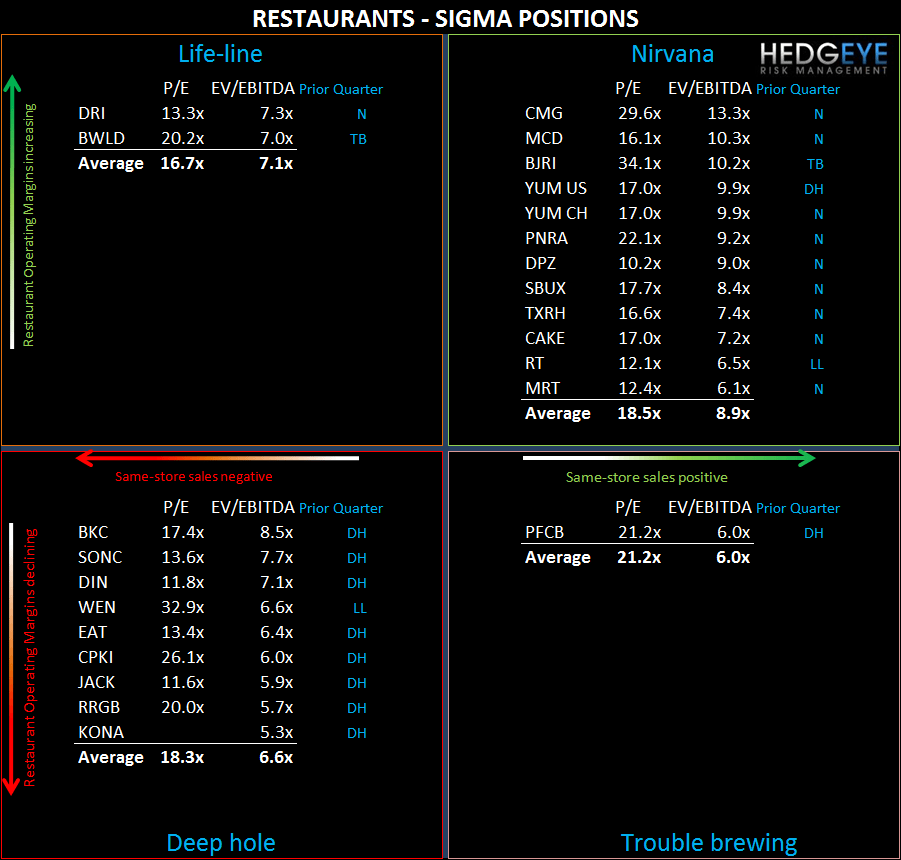

The following companies are currently enjoying positive same-store sales and margin growth as of the most recently reported quarter: CMG, MCD, YUM US, YUM China, BJRI, DPZ, PNRA, SBUX, TXRH, CAKE, RT and MRT. All of these companies, with the exception of YUM US and BJRI, were operating in Nirvana territory before the most recent quarter was reported.

As I did in July, I would like to bring to your attention a few names that I think may be “moonlighting in Nirvana”. YUM China, TXRH, MRT, CAKE and RT are the five names I would highlight as being particularly vulnerable to a move from Nirvana in the second half of 2010 (or by fiscal 2Q11, in RT’s case).

YUM continues to expect to face labor and commodity inflation in China during the second half of the year. Overall, as expected, China continued to operate in Nirvana during the second quarter, but will likely move into the Trouble Brewing quadrant (positive same-store sales and YOY decline in restaurant operating profit margin), and potentially, into the Deep Hole, during the back half of the year as higher food and labor costs materialize.

TXRH is guiding to same-store sales of +1% for the remainder of the year which implies a relatively stable two-year average trend. Food deflation is set to provide a sequentially more favorably environment than in 2Q but not as much as the company enjoyed in 1Q. That being said, YOY comparisons from both a cost of sales and restaurant-level margin perspective are set to become more difficult in the back half of the year.

My concern for MRT is primarily top-line related. While there is a certain amount of risk in their beef costs only being 20% contracted for 2010, given the 14% increase in Live Cattle prices YTD, I believe that the steep increase in sequential comps from 1H to 2H09 will make it difficult for MRT to maintain positive comps, particularly in 4Q10.

CAKE could also face pressure going forward due to an average check problem; customers have been trading down to small plate and snack items. In an effort to maintain comps going forward the company implemented a 1% effective menu price increase in August. Same-store sales and margin comparisons become decidedly more difficult, for CAKE, in 2H10.

RT’s outlook for their next quarter (1QFY11) is quite positive; same-store sales could improve again on a one-year and two-year basis and restaurant-level margins should increase year-over-year. However, as I wrote in my recent note “RT: IMPROVING BUT THINGS SHOULD SLOW”, momentum will likely slow from there for RT. Same-store sales, by my reckoning, will come under pressure for the balance of FY11 with margins likely following suit due to higher food costs as a percentage of sales and more difficult comparisons come to bear on the bottom line. RT could possibly be heading for the Deep hole in 2QFY11.

Other Nirvana standouts:

CMG: CMG is largely unlocked from a commodity perspective and this could impact margins adversely in the second half of 2010. Further increased costs on the labor, other operating cost (higher marketing) and G&A lines could further impair CMG from maintaining positive margin growth in the back half of this year. Investors may be less concerned about this increased margin pressure if the company is able to maintain its sales momentum from the second quarter.

The Deep hole quadrant is inhabited by companies experiencing negative same-store sales and declining restaurant level margins.

The following companies are currently suffering: SONC, DIN, BKC, WEN, EAT, CPKI, KONA, JACK and RRGB. The trouble about the Deep hole quadrant in this current environment is that there is no “magic bullet” that can solve the issues that have led the company there. Sometimes there are plans that management initiates that are margin accretive and build sustainable top-line momentum, but these strategies require a patient management team (resisting the temptation to take short cuts to print good numbers) and several quarters to implement. McDonald’s “Plan to Win” is one example of an effective strategy that has changed that company.

For the QSR names in the list above, MCD is the main problem. They continue to knock the cover off the ball – I estimate a +7% comp in August – and it is hurting BKC, WEN, SONC and JACK. For these names, I would not expect much movement from the Deep hole over the next few quarters and I believe that will be reflected in their valuations. Compounding the impact of MCD’s outperformance, JACK’s geographic issues augment the macro headwinds. Their overexposure to California and young Hispanic males (high unemployment cohort), in particular, has been pressing their stock for some time.

Other Deep hole standouts:

EAT: We expect the top-line to be volatile in the near-term as the customer familiarizes itself with the new menu. Following the most recent quarter’s earnings, I am marginally less confident in Brinker’s ability to meet earnings expectations over the next two quarters (1H11). I do expect, however, the company to see a material YOY improvement in restaurant-level margin in FY11, despite near-term sales volatility. Having extensively researched the operational initiatives and changes being undertaken by the firm to increase margins and customer satisfaction, I see the potential for a strong turnaround for Brinker. I remain confident in the direction of the company but believe that the turn in fundamentals is further out than previously thought.

Trouble Brewing: We believe that the trends associated with the Trouble brewing and Life-line quadrants are unsustainable. Companies usually find themselves in either territory in a transitional phase. Typically, if a company is posting positive same-store sales and declining year-over-year margins, the company is not leveraging the positive top-line and is spending too much on growth-related costs or increasing discounting. Whatever the reason, it usually spells trouble.

PFCB is currently situated in this quadrant. On a sales-weighted basis, its concepts are running same-store sales of +0.8%. Having taken price in May, for the first time in two years, and improved operational performance during the first half of the year, the company could see top-line strength persist if traffic can hold up (as of the date of the most recent earnings call, 7/28, traffic had been positive for five months). I expect a gradual improvement in restaurant-level margins in the second half of the year for PFCB.

PFCB is facing easy comparisons in 3Q10 on many fronts. At the same time, trends are getting better at the Bistro, which should make for a strong third quarter. PFCB could move up and to the right into the Nirvana quadrant during the back half of the year after starting out the year in the deep hole.

The Life-line quadrant is usually populated by companies that have “pulled the goalie”. When customers are not coming through the doors, sometimes companies cut costs in order to maintain bottom-line numbers in the absence of top-line strength. This clearly is an unsustainable situation. In other cases, such as 2Q for BWLD, a shift in commodity margins can boost margins and add to profitability even in a difficult top-line environment.

The following companies are in the Life-line territory currently seeing restaurant-level margins increasing year-over-year but same-store sales declining: BWLD and DRI. BWLD is likely going to experience year-over-year restaurant level operating margin expansion over the next number of quarters. This is largely due to the 31% decline in chicken wing prices since the YTD peak in January. The company is in the process of closing underperforming, lower volume stores but it is likely going to take some time.

Howard Penney

Managing Director