This note was originally published at 8am this morning, August 31, 2010. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK in real-time, published by 8am every trading day.

____________________________________

“What’s good about the contemporary world? You can say something around the corner from a public toilet and the whole world will hear because all the television cameras will be there.”

-Vladimir Putin

In context, this quote is taken from comments yesterday by Russian Prime Minister Putin in which he said that dissidents would keep getting beaten if they continued to hold unauthorized rallies.

The quote struck a chord with me on two fronts: 1.) it’s representative of the “closed” world Russia’s brass intends to promote, and 2.) it flies in the face of everything that Hedgeye’s founder, Keith McCullough, believes in, namely that an investment environment governed by transparency, accountability, and trust will help to increase the flow of ideas and hold market participants (and politicians) to higher standards--both of which will ultimately lead to a more even playing field for market participants and society at large.

Sticking to the first point, I’ve had the recent pleasure of working with our new Energy sector head, Lou Gagliardi, to analyze investment positions on the often “slanted” Russian playing field. While I’ll save the company-specific calls for Lou’s sector launch on September 16th, I do want to highlight some of the macro fundamentals and TREND and TAIL themes that may play out in Russia over the intermediate to longer term.

While we’d be duration sensitive in adding Russia to our virtual portfolio (we’re currently bearish over the intermediate term on oil), which we’ve previous played via the etf RSX, and we’re generally cautious on investment risk in Russia, the fundamentals suggest that Russia could outperform should commodity prices (in particular oil and gas) remain around current levels. Further, we see the country’s increasingly larger share of geopolitical influence as a bullish indicator for domestic and global stability and like its growth profile of ~4% in 2010 (IMF), versus 1% in the Eurozone and 3% in the US.

Fundamentals First

The first fundamental point to consider when discussing Russia is an obvious one, but one worth stating: the country is levered to the mighty Petrodollar. Russian President Dmitry Medvedev has been quick to issue decrees over the last year that the country will work to diversify its growth away from sole reliance on energy commodities, yet it’s clear to us across multiple metrics just how important the oil and gas industries have been for the country’s growth, a set-up we don’t expect to change over the next 3-5 years.

As a point of reference, oil and gas exports accounted for roughly two-thirds of all Russian exports by value, with oil and gas revenue contributing ~1/3 of general government revenue. Further, reviewing estimates on the marginal tax rate on petroleum, the government pulls in an average of 90 cents on every dollar of exported crude selling above $25/barrel, a favorable set-up should the price of oil remain around the current level of $75/barrel. [Note: under $25 the government also receives its share, albeit a proportionally smaller one on a tiered basis].

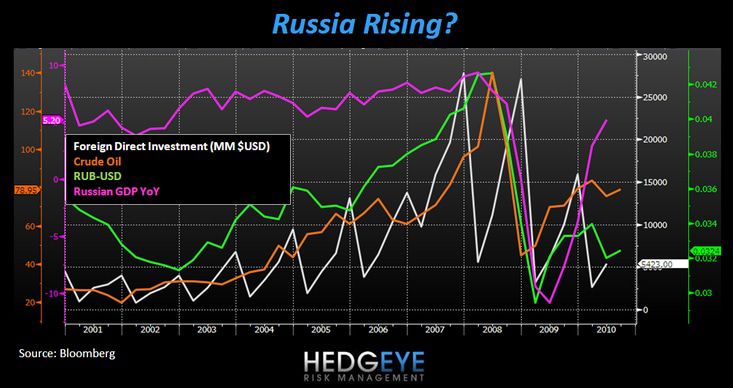

The chart below shows the tight correlations between the price of a barrel of oil, foreign direct investment in Russia, and the RUB-USD, and an inverse relationship to GDP over the last 10 years, which helps to outline the importance of the US Dollar in determining the price of oil, and therefore Russia’s economic outlook. The chart also implies an interesting trend in investor behavior: foreign direct investment piles in or out of Russia based on the price of crude. [As a side note, natural gas prices (not charted) fell in 2009 while oil ramped higher, a function of both separately priced global markets and supply and demand drivers that differ from crude.]

And if we’re right on our short call on the USD due to such factors as rising deficit and debt levels in the US and the potential for further QE packages (money printing) combined with our Housing call for a 15-50% decline in US home prices, a weak dollar may help buoy crude prices, and therefore Russian growth. The r-squared for the US Dollar Index versus crude is currently at 0.86 over a three week duration or a negative correlation of -0.93.

Sifting through Russian Tail- and Headwinds, in brief

Pros-

- Gas and Oil Cards: Russia holds the largest natural gas reserves in the world and is 2nd largest global producer of crude at ~9.7 MMB/d and the 2nd largest global exporter at ~7.0 MMB/d.

- Gas Influence: Europe relies on 1/4 of natural gas supply from Russia (40% in Germany). Gazprom’s 51% ownership stake in the natural gas Nord stream pipeline, which runs across the Baltic Sea, will add significant supply (est. 26 Million households) when the first line comes online in 2011.

- FX Reserves: 3rd largest in the world at $475.2 Billion.

- Geopolitical Influence: (Europe) political dominance over Ukraine, Belarus, and Moldova, important natural gas and oil transit countries and Russia’s window to the West, and an increasingly tighter grip over Kazakhstan, an energy rich country and world’s 5th largest grain exporter. (China) strategic and expanding partnership with China. China lent Russia $25 Billion in exchange for guarantees of crude last year.

- Consumer Demand: from QSR operators to automobile manufactures, select companies are highlighting a positive outlook on Russia. Ford’s Russia Chief Mark Ovenden recently said that “our view of Russia is that it will certainly be the most significant growth market in Europe and a very significant growth market globally.” For reference, Russian car deliveries increased 9% in the first seven months of the year (versus +0.6% in 1H for the rest of Europe) and jumped 48% in July, spurred by the economic recovery and the government’s cash-for-clunkers program, according to the Moscow-based Association of European Businesses.

Cons-

- Demographics: the country’s demographic outlook is grim. The World Bank reported that by the end of 2009, 17.4% of the population (24.6 Million) will live beneath the subsistence level of $185 per month, about 5% more than before the global recession. The Economy Ministry said Russia’s working population will annually decrease by ~1 Million every year over the next three years, and the population has been in decline over the last 14 years, falling to 141.0 Million in 2010.

- Inflation: The Economy Ministry raised its 2010 inflation forecast to 7-8% from the previous estimate of 6-7% after the drought is set to crimp agricultural production and push up consumer prices (negative domestically).

- Political friction with the USA: talks with President Obama to “restart” relations have largely stalled and relations between Washington and Moscow have parted ways following the exchange of spies in July. Ongoing Russian fears that US will install antiballistic weapons in Poland and Czech Republic persist.

As Lou often says in our morning meetings, we want to be long energy long countries like Russia. While multiple factors play into our analysis, the root of Lou’s comment implies an investment bias towards countries that produce more oil (or natural gas) than they consume. Brazil is another country that follow this mold.

Despite the political curtain that is often drawn in Russia, the country’s natural resources offer a compelling investment opportunity with a commensurate risk premium. Stay tuned as we look to add Russian energy names to the Hedgeye Virtual Portfolio. To get access to Lou’s energy launch please contact sales at sales@hedgeye.com.

Matthew Hedrick

Analyst