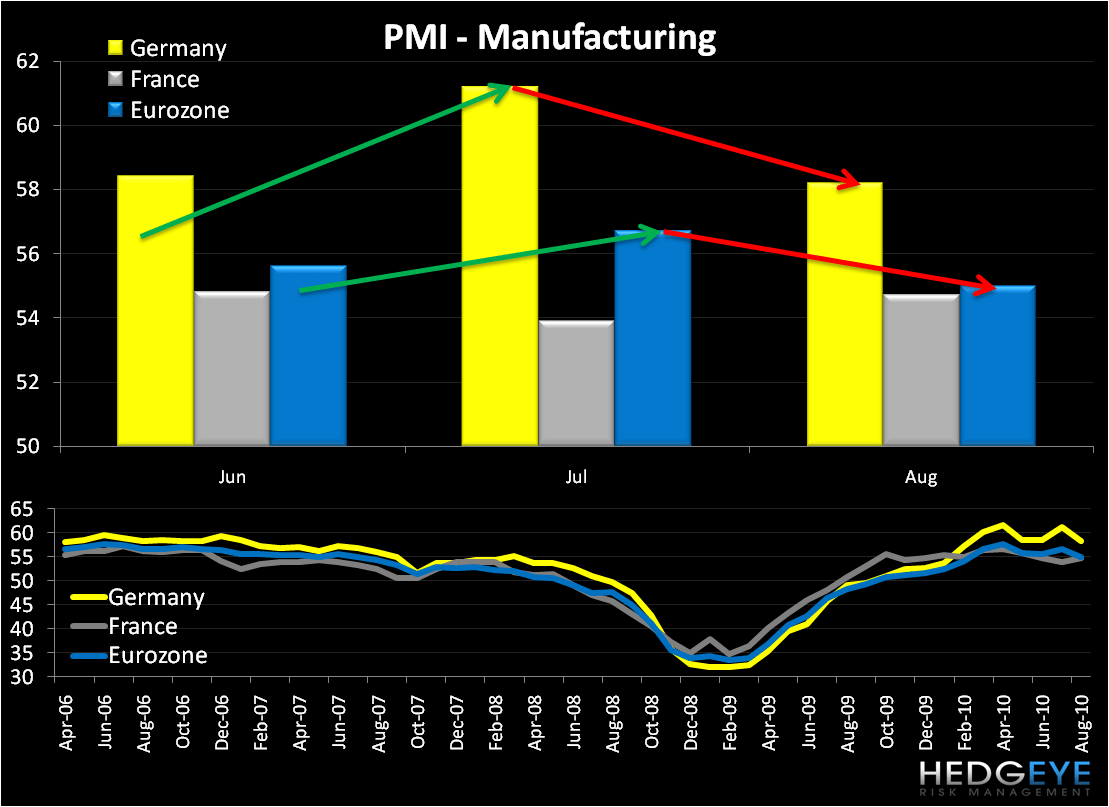

Our call has been for an inflection in European data in August to the downside. Today, PMI Manufacturing data showed a significant decline in Germany and for the Eurozone average. Services also fell in France and the Eurozone, while German Services continued their steady gain. We contend that Manufacturing and Services numbers from Europe, especially Germany, France, and the UK, will trend downward throughout the remainder of the year.

As we’ve outlined in previous notes, our thesis for this slowdown includes:

- August Data - we expect to see a sequential slowdown (month-over-month) in the fundamental data following the exuberance of the World Cup.

- Headwinds - European markets will be pinned against significant macroeconomic headwinds in the back half of 2H10, including suppressed growth, consumer demand, and confidence as a result of government austerity measures.

- Housing - continued downward pressure on the housing market, in particular in Spain and the UK.

- Legacy - ongoing uncertainty about European sovereign debt, including bank exposure to sovereign debt, which was largely unaccounted for in the 91 bank stress test, as well as continued fiscal and political weakness throughout the region (Greece and Hungary in particular).

Matthew Hedrick

Analyst