This chart was published this morning in conjunction with the Early Look note, available to subscribers in real-time at 8am every trading day.

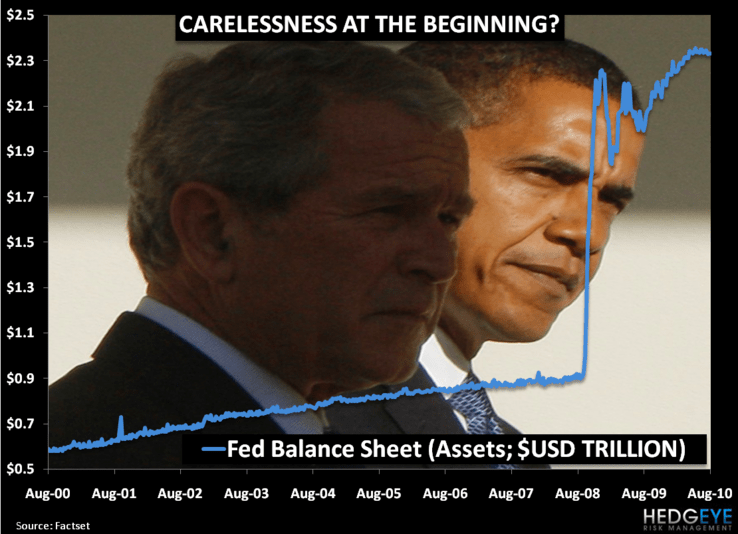

Carelessness at the beginning? Fed Balance Sheet (Assets; $USD Trillion)

This chart was published this morning in conjunction with the Early Look note, available to subscribers in real-time at 8am every trading day.

Carelessness at the beginning? Fed Balance Sheet (Assets; $USD Trillion)

By joining our email marketing list you agree to receive marketing emails from Hedgeye. You may unsubscribe at any time by clicking the unsubscribe link in one of the emails.