NewsWire: 10/12/2020

- According to the latest CBO budget outlook, annual economic growth is expected to be just 1.6% annually over the next 30 years. This would be the lowest growth since the 1930s, which the report attributes to persistently low birthrates, slowing labor productivity growth, and ballooning federal debt. (The Wall Street Journal)

- NH: Every year about this time, the CBO releases another "long-term" budget outlook--this one going all the way to 2050.

- The headlines surrounding these outlooks typically focus on the CBO's long-term projections for federal deficit and debt trends. Since this new projection comes on the heels of 2020's unprecedentedly large stimulus package, there's plenty of startling news here to report. And we will come back to it in tomorrow's NewsWire report.

- But let's start first with the subject of WSJ reporter Greg Ip's discussion, which is changes in the CBO's underlying long-term economic assumptions. In their own way, these assumptions are even more startling.

- Up front, we need to set the stage. Real GDP growth averaged nearly 3.5% over the business cycle from 1951 until 2002. It dropped to around 2.5% from the 9/11 recession trough to the 2008 peak. And then it dropped still further to 1.6% during the ten-year recovery (2009-19) since the GFC.

- So where is it going next? You may be hoping that the CBO would write off much of the recent decline as a one-time misfortune, unlikely to happen again. But no. The CBO currently projects that real GDP growth over the next three decades will virtually be unchanged--at around 1.6%--from where it was over the last decade. See the following chart. (Note: The word "potential" here is just CBO's way of focusing on the steady growth trends and paying no attention to cyclical booms and busts.)

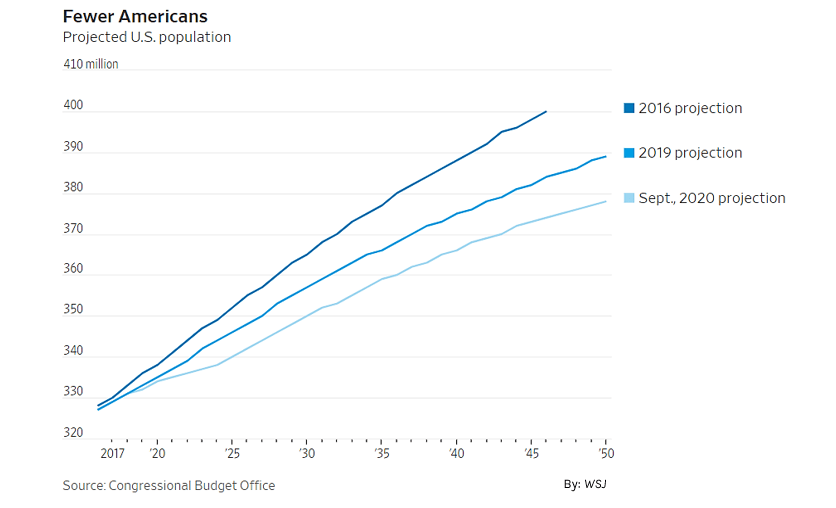

- The biggest game changer, as this chart makes clear, is declining growth in "potential labor force," that is, the U.S. working-age population. A relatively large Boomer generation is retiring or dying at the older end, and relatively small post-Millennial generations will be taking their place at the younger end. Last decade, the labor force grew at only 0.5% annually, already the slowest decadal rate in American history. Thereafter, it will slow even further. By the 2030s, it will nearly come to a halt at 0.2% before slightly accelerating again in the 2040s (when the Millennials' own children start entering the workforce--call this the "echo-echo" boom if you like.)

- Much of this downshift in workforce growth was obvious to demographers decades ago. Now, on schedule, it is arriving.

- Yet new data over the last few years are persuading demographers that the speed of the projected downshift will likely be faster than they had earlier expected. This explains why the CBO has recently been ratcheting down its long-term population and real GDP growth rate forecasts from one report to the next.

- What new data are we talking about? Well, let's look at three negative surprises.

- First, there's the stubborn and ongoing decline in the US total fertility rate (TFR). Throughout the long economic expansion of 2009-19, contrary to all expectations, the TFR declined in every year but one (2014, a minor uptick). Last year, at the peak of the business cycle, the TFR hit another historical low at 1.71. In 2020, we know that the TFR will take another big hit--maybe all the way down to 1.55 or lower. (See "The Baby Bust of 2020.") Few demographers any longer believe that most of this is just a temporary "tempo effect." The impact of recent fertility declines on new workers will be significant by the 2030s and (especially) the 2040s. Millennials, it seems, will not be generating as large an "echo" as we once anticipated.

- Second, projections for net immigration are getting scaled back. Here we're looking at many drivers: declining family size in Latin America; tougher enforcement of immigration laws; and (most recently) a severe reduction in net inflow to due Covid-19 restrictions. Annual immigration is still expected to grow decade over decade, but not as rapidly as was once expected. It will certainly continue to play a critical role in any further expansion in the American workforce. Indeed, by the 2030s, it could be responsible for all net growth in U.S. employment. (See "Immigration an Increasingly Vital Component of U.S. Population Growth.")

- Third, mortality rates are not declining as fast as we once hoped. The 2010s witnessed an astonishing rise in the mortality rates of working-age Americans--and, for several years in a row, declining U.S. life expectancy. More deaths among Americans who are still working translates, mechanically, into fewer workers and lower real GDP. This effect isn't as large as fertility and immigration, but the fact that we're talking about it all is quite a surprise. For the first time (that I can recall), the CBO model is differentiating between the mortality trend for lower-income Americans versus higher-income Americans. (See "Adults Under Age 65 Driving Decline in U.S. Life Expectancy.")

- OK, so much for labor-force growth. Now let's turn to productivity growth, the other main driver of real GDP. Here admittedly it's harder to make any certain long-term forecast. Yet over the last few years, as Ip notes, the CBO has steadily ratcheted down its productivity assumptions.

- Yet the reason for the CBO's pessimism is not that it expects productivity growth to be lower in future decades than it was in 2009-19. The CBO actually assumes slightly faster growth. (See first chart above.) It simply no longer assumes that the recent recovery was an era of anomalously low productivity growth and that we should expect a sizeable rebound. The CBO is gradually migrating toward the view that last decade's productivity growth dropoff was due to long-term structural forces that may not change much in the foreseeable future.

- One of these forces, responsible for about a third of productivity decline (relative to pre-2008 decades) is declining net accumulation of capital--that is, structures and equipment, intellectual property, and residential housing. This rate has been declining both in the private and public sectors, and the CBO expects this decline to continue. Here's one area where growing fiscal deficit projections directly impact economic projections, since higher federal deficits will ultimately crowd out private investment via rising real interest rates--and crowd out public investment by pressuring policymakers to delay or defer such outlays.

- The other force, responsible for the remaining two-thirds, is declining "total factor productivity" (TFP), which basically reflects any change in labor productivity which cannot be accounted for by a change in easily measurable capital inputs. Here we're talking about all the intangibles. One of these is human capital. Today, the oldest working generation, Boomers, is nearly as educated as the youngest working generation, Millennials. This means that a dynamic which helped boost TFP in earlier postwar decades--the steady replacement of older less-educated retirees with younger more-educated entrants--will no longer matter as much.

- TFP growth also encompasses expected qualitative shifts in productivity growth which defy any quantification. One of these is climate change. Here, the CBO manages to come up with an impact number--no doubt because it feels political pressure to take this formally into account. But its estimate is very small: Climate change per the CBO will pull down productivity growth by -0.03% per year over the next 30 years.

- A more important driver of future productivity growth, in the minds of most economists, is the underlying pace of business dynamism. Here, as good model-driven economists, the CBO analysts say nothing explicit. But I have argued that one could make an excellent case for declining dynamism by pointing to clear declines in worker mobility, job creation and destruction, firm turnover, and numbers of firms--and clear rises in market concentration, barriers to innovation, the size and age of a typical firm. (See "Declining Business Dynamism: A Visual Guide," "Have Boomers Stifled Business Dynamism?" and "What Will It Take to Re-Invigorate U.S. Entrepreneurship?") In other publications devoted to explaining "the slowdown of growth in total factor productivity," the CBO summarizes a similar list of causes.

- With Donald Trump as President, conservatives have regularly bashed the CBO for their irresponsible "pessimism." But I have a pretty safe prediction to make. If Biden is elected, they will be bashing the same CBO projections for their unrealistic optimism. That's how partisan we've become--not just in our perceptions of the uncertain future, but even in our perceptions of how the economy is doing right now.

- Tomorrow: The Fiscal Side of the CBO Long-Term Forecast.