TODAY’S S&P 500 SET-UP

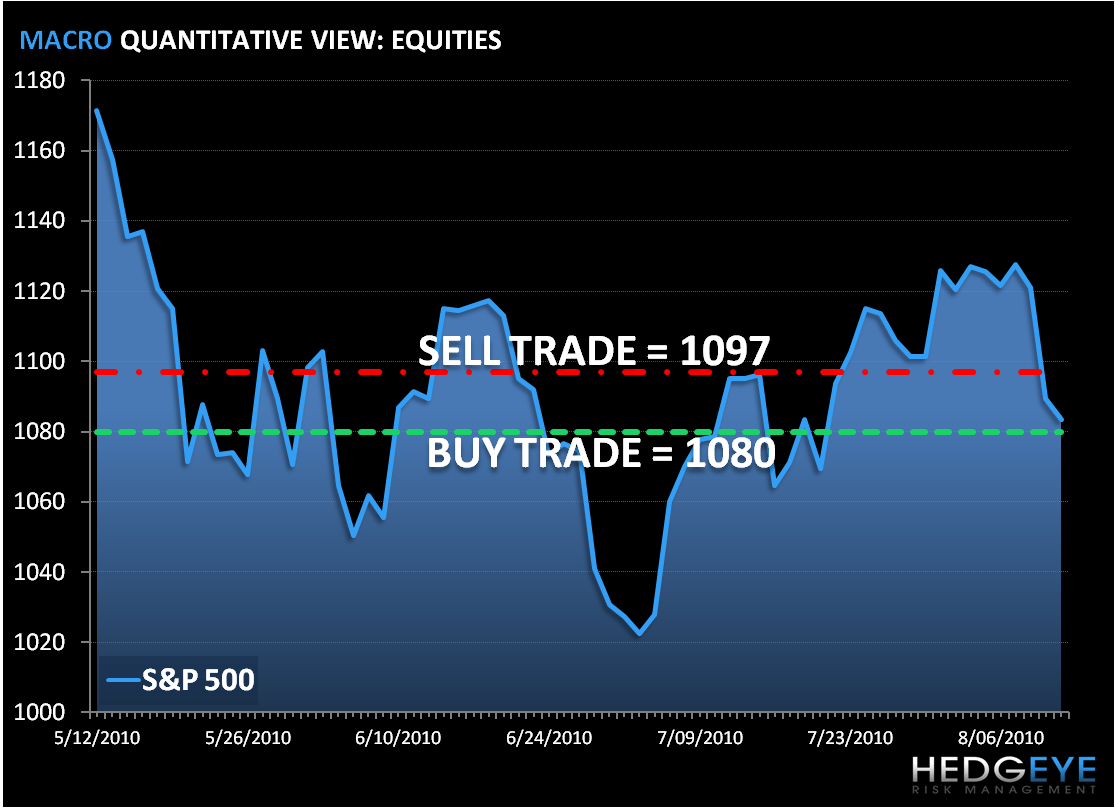

As we look at today’s set up for the S&P 500, the range is 17 points or 0.3% (1,080) downside and 1.2% (1,097) upside. Equity futures are trading below fair value in an erratic morning; there was early strength on the back of strong Q2 German GDP but that has since given way MACRO economic concerns - July CPI and Retail Sales will be in the spotlight today. Headline CPI is estimated to have increased by +0.2% m/m, and Retail sales to have risen +0.5% m/m.

- ADVANCE/DECLINE LINE: -436 (+1854) Breadth positive on a down day!

- VOLUME: NYSE - 1007.39 (-13.48%) - Summer volume for sure!

- SECTOR PERFORMANCE: Two sectors positive - XLB and XLV

- MARKET LEADING/LAGGING STOCKS: Office Depot +4.46%, Motorola +4.16 and Cisco -9.38% and Netapp -8.67%

EQUITY SENTIMENT:

- VIX - 25.73 1.34% - The VIX now up for 4 days and bearish for equities.

- SPX PUT/CALL RATIO - 2.98 up from 1.64 surging yesterday (low on 07/15/10 of 0.87)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD - 22.54 -0.382 (-1.669%)

- 3-MONTH T-BILL YIELD .15% Unchanged

- YIELD CURVE - 2.1661 to 2.2061 (close) - Now at 2.1786

COMMODITY/GROWTH EXPECTATION:

- CRB: 268.91 +0.03% (first up day this week)

- Oil: 75.74 -2.92%

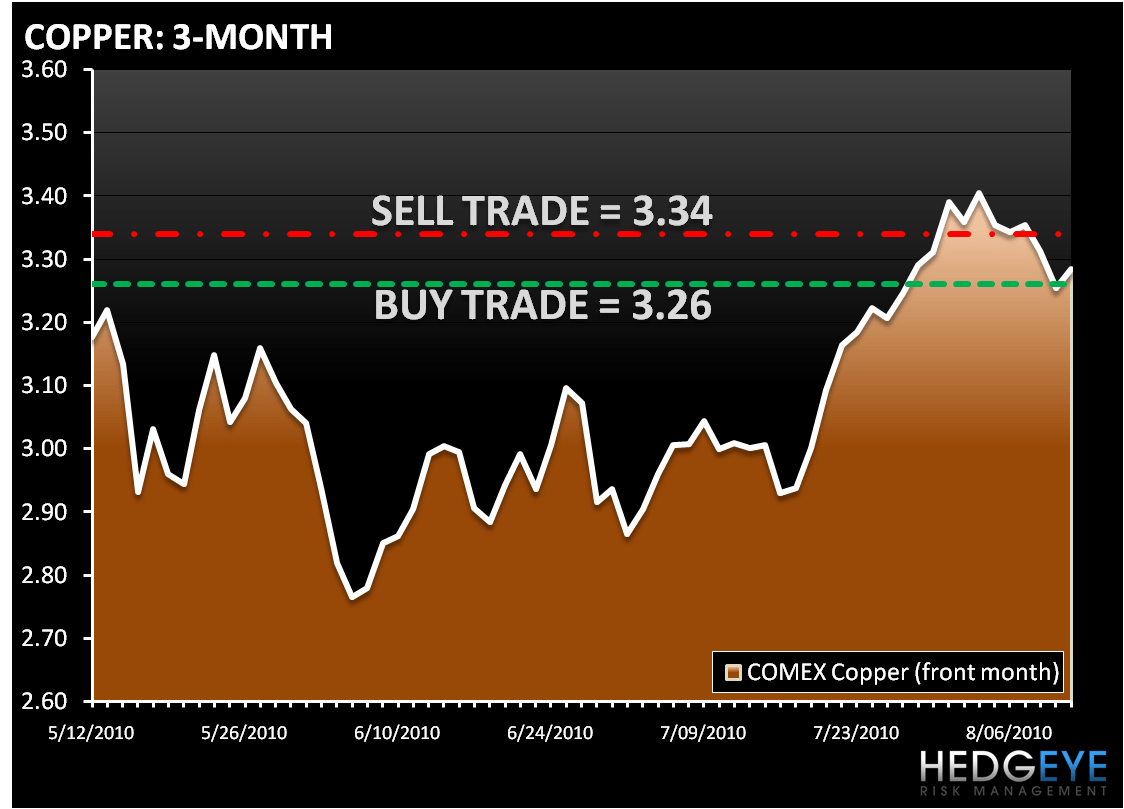

- COPPER: 330.55 +0.92% (currently trading at 322 - BEARISH for growth expectations)

- GOLD: 1,213 +1.38% (safe haven status returning?)

CURRENCIES:

- EURO: 1.2849 -0.28% - (trading down every day this week)

- DOLLAR: 82.635 +0.42%) - (trading up every day this week)

OVERSEAS MARKETS:

- ASIA - Closed on a stronger note. Japan closed modestly higher on the day, but closed 4% lower on the week. China's Shanghai index closed up 1.2% (down 1.94%on the week), as property shares reversed earlier losses triggered after a central bank statement showed a steep drop in new mortgage loans in Shanghai.

- EUROPE - Markets are trading back below breakeven after a slightly disappointing Italian bond auction offset earlier strength generated by a robust Q2 GDP reading from Germany.

- EASTERN EUROPE - Trading mixed to lower - Russia down for the fourth day; Latvia up 1.80%.

- LATIN AMERICA - Trading higher Peru, Argentina and Brazil and up small.

- MIDDLE EAST/AFRICA - Trading mixed.

Howard Penney

Managing Director