This insight was originally published on July 16, 2010 for subscribers. RISK MANAGER SUBSCRIBERS have access to SELECT MACRO content in real-time.

____________________________________

Position: Long Chinese Yuan via the etf CYB.

Conclusion: Slowing economic data supports sequentially slowing growth in China, and policy actions suggest more slowing is to come. Despite this, China's organic growth story is right on track. Eventually, investors will pay a premium for it again.

Like we’ve been saying since our January 15th Chinese Ox in the Box theme, China’s 6-9 month economic outlook looks bearish. As bearish as that may be, the long term economic outlook for China is equally bullish and at a point, investors will again pay a premium for that growth. The whole concept of premium is hinged upon relative economic health and that will begin to matter a great deal more than it did in 1H10, as investors begin to rightfully get long those nations with strong balance sheets.

China has been tightening its economy to cool its white hot growth and inflationary pressures. Those methods have included: targeting a reduction in loan growth, raising lender’s reserve requirements, selling bills to soak up excess liquidly, and tightening controls on the expansion of businesses that are heavy energy users (i.e. manufacturing). As a result of these actions, we have seen Chinese economic growth slow as verified by the following data points:

- GDP slowed sequentially: 10.3% y/y in 2Q vs. 11.9% y/y in 1Q;

- Money supply growth (M2) continues to slow: 18.5% y/y in June vs. 21% y/y in May – June marks the slowest growth since Dec. 2008 and has slowed each month since November;

- Loan growth continues to slow: 603B Yuan ($89B) in June vs. 639.4B Yuan ($94B) in May vs. 774B Yuan in April;

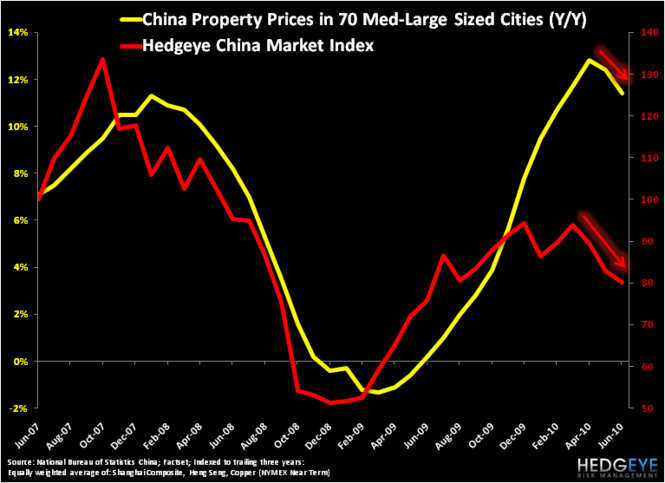

- Property Prices continue to slow: 11.4% y/y in June vs. 12.4% y/y in May vs. 12.8% y/y in April;

- CPI slowed sequentially: 2.9% y/y in June vs. 3.3% y/y in May

- Commercial Real Estate sales growth slowing – Floor Space sold declining: 15.4% y/y Jan-June vs. 22.5% y/y Jan-May; Sales Volume slowing: 25.4% y/y Jan-June vs. 38.4% y/y Jan-May;

- Fixed Assets Investment continuing to slow: 25.5% y/y Jan-June vs. 25.9% y/y Jan-May;

- Funds In Place for Investment continuing to slow: 29.2% y/y Jan-June vs. 33.8% y/y Jan-May;

- Investment in Construction Projects slowing: 27% y/y Jan-June vs. 28.7% y/y Jan-May.

As suggested by the data above, China’s tightening measures are producing the desired results and China has no plans to loosen the reins anytime soon. On Tuesday, The Ministry of Housing and Urban-Rural Development reiterated that it will maintain curbs on speculative purchases and increase market supply. Furthermore, China’s banking regulator said it has made no changes to policies on home loans, calling on commercial banks to strictly enforce home loan rules.

The momentum associated with these declining statistics and the government’s resolve to maintain tightening policies towards the Chinese property market suggest that the easy money in China has likely moderated for now. As a result, the Chinese equity markets have suffered (the Shanghai Composite is down 27% YTD and is underperformed by only Greece since the start of the year). Chinese entrepreneur confidence followed suit, down 2.5% Q/Q in 2Q, alongside slowing imports, slowing PMI, and slowing industrial production. Furthermore, weakening commodity prices in the face of a dollar decline are all sings that the Chinese demand side of the REFLATION trade is diminishing.

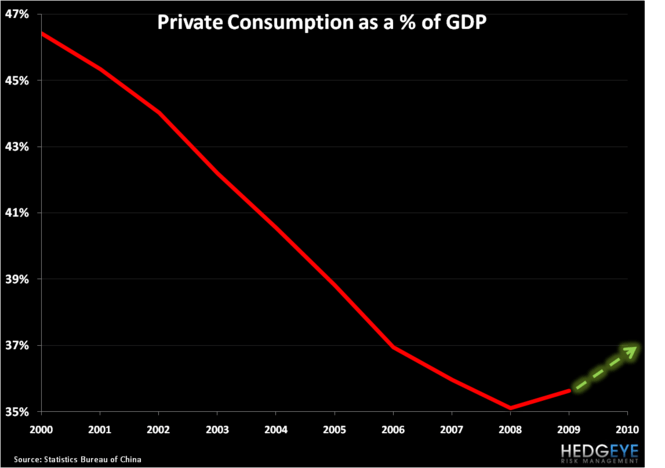

All is not cause for alarm, however. As I pointed out in a note last Tuesday, the Chinese government has been busy making moves to position itself to better weather a slowdown in international trade. Those measures include increasing minimum wages by as much as a third in more than 21 provinces and municipalities this year, and, of course, relaxing the Yuan peg. Those measures, combined with further appreciation of the Yuan from here, will help stimulate domestic consumption, which has fallen from 46.4% of GDP in 2000 to 35.6% of GDP in 2009. Domestic consumption in China, much like Singapore, has a very bullish long term outlook and recent developments are further enhancing those prospects.

Those prospects are exactly the reason the international community is pouring capital into the country. Foreign Direct Investment in China just hit its second-highest reading on record in June. Investment sequentially accelerated to 39.6% Y/Y in June to $12.5 billion, the Ministry of Commerce said in Beijing yesterday – the most since December 2007. For the first six months of the year, Foreign Direct Investment rose 19.6% Y/Y to $51.4 billion, after a 14.3% Y/Y increase in the first five months. Foreign Direct Investment in China has shifted on the margin towards investing in China’s growing urbanization. Tesco, the U.K’s biggest retailer, said in April it will spend 2.5 billion pounds ($3.7 billion) over five years to open shopping malls and hypermarkets in China. For China this is a step in the right direction vs. last year when nearly 52 percent of foreign investment went to manufacturing and another 19 percent to real estate (National Bureau of Statistics). Furthermore, China could see even higher foreign investment if it opened up more industries, including telecommunications, transport, and resources to overseas companies. Any policy shifts in that direction will only accelerate the amount of capital flowing into the economy.

Rising incomes and the likely urbanization of hundreds of millions of people has also attracted private equity funds flows into the economy. At only 40%, China’s urbanization has a great deal of headway to grow, which is one of the reasons China attracted $10.5 billion (275% Y/Y) of private-equity capital in the first half of this year, accounting for 68 percent of the $15.4 billion raised in Asia in the period (Centre for Asia Private Equity Research). Following in the footsteps of Blackstone Group LP and Carlyle Group, KKR is seeking to raise $800 million to invest in China.

All told, China’s organic growth story will matter more when consensus finally comprehends the downside risk associated with the U.S.’s 12-18 month forward economic outlook. As easy money brought on by REFLATION, accelerating trade, and industrial production slows globally, organic growth stories will move to the forefront of investment opportunities. Governments worldwide will have to think twice about levering up and implementing further stimulus, so those economies that have proactively prepared themselves to grow organically will see their equity markets and currencies strengthen in 2H10 and 2011, and beyond.

Darius Dale

Analyst