“America is a currency creator so there’s no reason for people to live like this. They always say if you print money it will cause inflation. They just printed $3T. Little or no inflation.”

- Ice Cube, 10/1/2020 (Twitter)

So, we’re now compelled to ponder the prospects of a Pence presidency, apparently.

The national discourse has obviously devolved to a wholly satirical level.

A first-order knock on effect for analysts charged with translating policy proposals to quantified growth/inflation/profit forecasts is that taking amorphous talking points and non-descript overtures to aspirational/ideological policy agenda’s and somehow back propagating those to update your expectation around actual macro or market parameters is an intractable exercise.

Nebulous commentary nested atop a straw man premise, further nested within a counter factual argument and garnished with false equivalence can “work” on stage in 2-minute time allotments.

Particularly for an attention-deficit populous with a diminishing proclivity for nuance and no interest in disentangling partial truths or objectively evaluating multi-dimensional problems to which they (seemingly) have no direct attachment to.

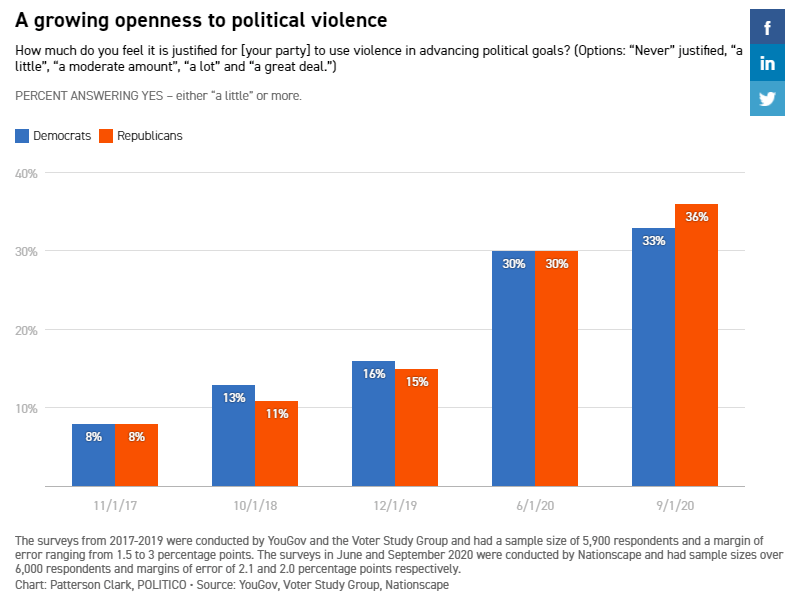

Meanwhile, over one-third of surveyed voters now approved of political violence.

We can do better than this.

Back to the Global Macro Grind…

Allow me a quick Friday riff then I’ll transition to some labor related data contextualization, I promise.

Keith framed Monday’s EL as MMT vs Gravity.

Our 4Q themes presentation offered an alternative framing: MMT because of (Socio-economic) Gravity.

Ice Cube gets it.

The Fed gets it, seemingly.

If you are unfamiliar with FedNow (see: HERE and HERE), it is a Fed designed and implemented instant, digital payment infrastructure that effectively gives the Fed a direct line to every household and business in the country.

If you want an infrastructure capable of making direct disbursements to households in lieu of junk bond purchases and isolated socialism for wall street and the 1%, FedNow is certainly a step in that direction.

Volatility suppression and inequality are both byproducts of policy. Their co-evolution has progressed in such a way that volatility suppression in assets has progressively leaked out and re-manifested in a kind of growing social volatility.

I’ve discussed this elsewhere at greater length but, suffice to say, the self-reinforcing inequality spiral is likely to continue to the point it becomes untenable and implodes in on itself, birthing a more discrete shift towards some version of redistribution policy.

The baby steps towards that eventuality have already been taken (with Bernie/Warren/etc as serious candidates with populous backing)

Until we get a tangible shift towards a real MMT style policy whereby the middle-men (primary dealers & financial mkts with a hoped for trickle down) are cut out and stimulus is delivered more directly to the people, status quo/conventional policy will continue to drive a further rise in inequality.

Again, we’re baby stepping there in policy space (i.e. Main Street Lending Facility, lower income households explicitly a target of policy, FedNow, etc)

I don’t know when we hit the critical threshold but my current view is that it’s basically an inevitability.

That’s not a political opinion or some normative prescription or even the official Hedgeye stance.

It’s just my objective assessment of the larger constellation of factors shaping the macro climate and the conclusion that the socio-economic imbalance is real, the underlying frictions are growing more evident and that the imbalance will ultimately correct/mean revert.

A catastrophic economic reset is not a viable option. ‘QE for the People’ is eminently preferable (and sellable), both absolute and relative.

Anyway, Copper is rolling over, Brent has broken bad, breakevens are flirting with a breakdown, someone is puking TIPS, and the dollar is threatening to confound the “sure thing” short base as the Quad 4 vs Quad 3 debate continues to tick in real-time.

And this week’s domestic high frequency data is labor-centric.

Some quick context:

Jobless Claims & NFP:

- DOL release with link to CA reporting change and full data table (including PEUC figures) → HERE

- Initial Claims fell to +837K *although that comes with the caveat that CA reporting is on pause (which matters given its size & contribution)

- Continuing Claims fell but Total Claimants rose and remains stubbornly elevated … in a further sign that structural damage is an increasingly inescapable reality.

On the spending side, it turns out that if you stop giving people money, they have less money.

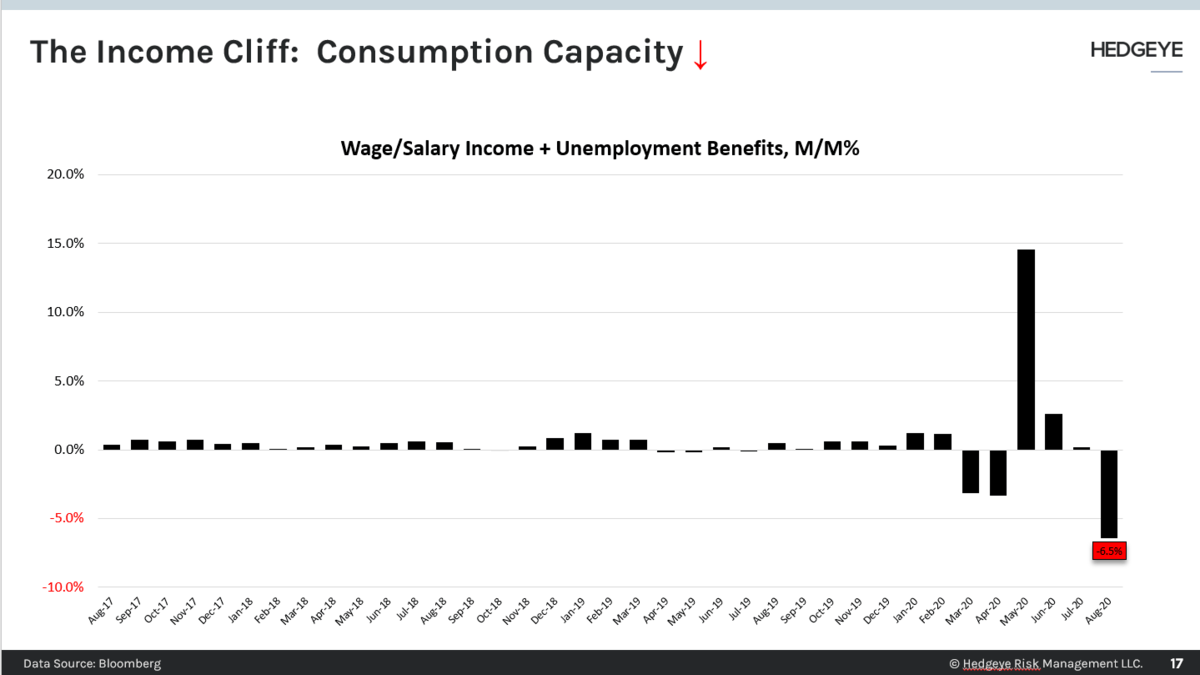

Household Spending:

- Personal Income: Total Personal income fell -2.7% M/M, but more notably...

- Consumption Capacity – the sum of Wage/Salary Income + Unemployment Benefits - fell -6.5% M/M.

- This is the emergence of the collective income cliff and the risk to a stalling in the consumption economy absent further stimulus.

What To Watch:

- With payroll support timelines expiring (airlines) and >100K in job cut announcements this week, there is upside risk over the coming week(s).

- PEUC: Pandemic Emergency Unemployment Claims should be the metric to monitor as the flow out of regular state claims into the 13 weeks of extended benefits will show up here.

- PEUC claims were up a notable +200K in the latest week. Note that this series is two weeks lagged. …

- Note also that regular state benefits typically last 26 weeks we are thru week 28 of the pandemic payroll meltdown. With the PEUC data lagging by two weeks, it reflects flow dynamics for week 26.

- There are scenario’s under which one could get 26 weeks of regular UI benefits, then 13 weeks of PEUC benefits, then roll into an additional 13 weeks of PUA benefits to the extent they meet the eligibility requirements, but:

- The notion that states will fully and smoothly be able facilitate large-scale transitions of this nature is dubious, at best, and …

- Whether they can effectively facilitate a transition that provides for extended-extended benefits probably doesn’t matter. The program and associated benefits, as it stands, is scheduled to expire on December 31st. The PUA Cliff countdown is on.

- NFP: In addition to the Headline gain and any read-through on the timeline for full payroll normalization, further rise in permanent job loss and those on long-term unemployment (15-26wks and 27+wks) will remain the metrics to monitor with respect to burgeoning structural damage and the outlook for spending as those individual lose unemployment benefit eligibility.

- Note that Census Hiring - which supported the August headline by -250K - will begin to roll off … although most of that hit will likely come next month.

And lastly, just to leave you with some perfect K-shaped juxtaposition.

Last month was simultaneously the best month ever for IG issuance and among the worst months ever for bankruptcies and business closure. Simultaneously the best month ever for home sales and record high levels of housing and food insecurity.

Immediate-term @Hedgeye Risk Range with TREND signal in brackets:

UST 10yr Yield 0.62-0.70% (bearish)

UST 2yr Yield 0.10-0.14% (bearish)

SPX 3 (bearish)

RUT 1 (bearish)

NASDAQ 10,508-11,415 (bearish)

Tech (XLK) 109.21-118.46 (neutral)

REITS (XLRE) 33.40-36.12 (neutral)

Utilities (XLU) 56.57-60.40 (bullish)

Financials (XLF) 22.75-24.40 (bearish)

Shanghai Comp 3168-3348 (bullish)

Nikkei 223 (bearish)

VIX 25.06-30.89 (bullish)

USD 93.28-94.97 (bearish)

Oil (WTI) 36.51-40.12 (bearish)

Gold 1 (bullish)

Best of luck out there today,

Christian B. Drake

Macro Analyst