This insight was originally published on July 13, 2010. Macro Select intraday updates are available to RISK-MANAGER SUBSCRIBERS in real-time.

MACRO: THE DEFICIT STILL LOOKS UGLY, NORMALIZE FOR TARP AND IT LOOKS UGLIER

_____________________________________________________________________________

Conclusion: While June was an improvement for the deficit due to timing related to Memorial Day, the year-to-date numbers remain concerning. On the other hand, the appointment of Jack Lew to OMB Director is a marginal positive.

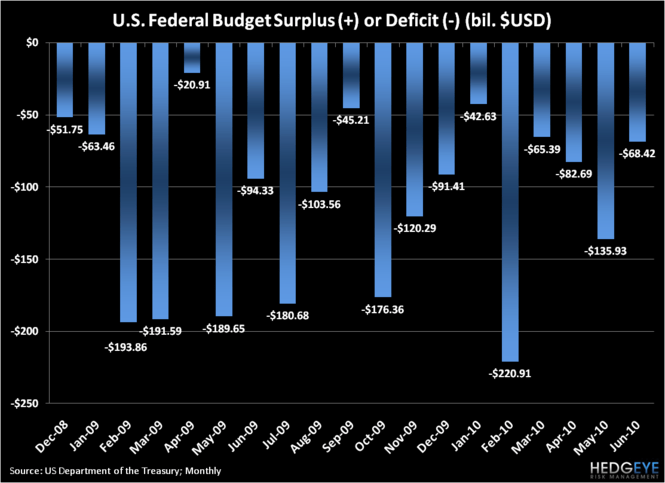

The U.S. government reported a smaller monthly budget in June versus June 2009 with a deficit of $68.4 billion versus $94.3 billion last June. In the year-to-date, the budget deficit is $1 trillion versus $1.1 trillion over the same period in 2009. On a year-to-date basis, the budget deficit as a percent of GDP is 9.2% versus 10.2% in the same period in 2010. While this high level summary suggests marginal improvement, the underlying facts still suggest dire fiscal issues in the United States on a number of fronts.

First, the June improvement in deficit can be attributed primarily to timing of revenues. Due to the Memorial Day, a large amount of tax revenue was pushed into June. In aggregate for the year-to-date, overall revenues are only up 0.5%, with corporate income tax contributing all of this increase growing 33% y-o-y. Personal income tax, on the other hand, is down -4.4% in the year-to-date. So despite the “economic recovery”, tax receipts from individuals are still lagging on a year-over-year basis (jobless recovery sound familiar?).

Second, while reported outlays were $73 billion, or 3%, lower for the first three quarters of the fiscal year, this decline included a reduction in nearly $350 billion from a combination of TARP, Treasury payments to Fannie Mae and Freddie Mac, and net outlays for FDIC insurance. If normalized for TARP, so removing the $350 billion from last year’s numbers, then spending ex-Tarp is up 10.6% on a year-over-year basis! Not a good trend.

While a large proportion of this was driven by unemployment insurance, every major line item showed a meaningful increase year-over-year. Specifically,

- Defense spending was up 5.8%;

- Social security was up 6.0%;

- Medicare was up 4.3%;

- Medicaid was up 8.9%; and

- And Other was up 9.1%.

Line item spending dramatically outpaced the economy vis-à-vis GDP growth and tax revenue growth.

In conjunction with this release, President Obama also named Jack Lew the new budget director. While Orzag has a following amongst the paparazzis in Washington, Lew is actually an experienced hand in the budget area and has spent seven years in the OMB. He was lastly OMB director under President Clinton until 2001, and produced a budget, with the help of a healthy economy, that resulted in a surplus of $236 billion.

Given his prior experience, prior success, and proven ability to work across bi-partisan lines, President Obama seems to have made a solid choice in Lew. Even though he spent some time as Chief Operating Officer at Citi Alternative Investments, we will still give him a free pass on that job choice for now. He certainly has the wherewithal to take a tough stance on the budget, but the next few months will actually show how serious the Obama administration is about narrowing the deficit.

Daryl G. Jones

Managing Director