This insight was originally published on June 21,2010. MACRO Intraday updates are available to RISK MANAGER SUBSCRIBERS in real-time.

_________________________________________________________________

Conclusion: The potential revaluation of the Yuan is positive for Chinese equities, but likely negative longer term for Treasuries. It will also benefit the currencies of those nations that supply basic materials to China – Australia, New Zealand, Canada, and Brazil.

The global macro news of the day is, of course, the statement by the People’s Bank of China that they are going to end the two year peg of the Chinese Yuan against the U.S. dollar. The timing is apropos as the G20 Summit is occurring this coming weekend in Ontario, and increased pressure on the Chinese to let their currency more freely float was very likely. At the least, the Chinese have bought themselves time in that debate, though it does seem likely that this is the first step in a more freely floating currency.

Per the release from the People’s Bank of China:

“The global economy is gradually recovering. The recovery and upturn of the Chinese economy has become more solid with the enhanced economic stability. It is desirable to proceed further with reform of the RMB exchange rate regime and increase the RMB exchange rate flexibility.”

While this announcement is certainly bullish for the Yuan, it must be taken with a grain of salt as it doesn’t dictate a revaluation of the Yuan or even a change in the daily trading range, but emphasizes flexibility. So, in effective, it was the bare minimum in terms of policy to support a Yuan revaluation. Clearly, though, with increasing signs of inflation within China, this is a way to dampen housing and consumer price increases that threaten the Chinese economy.

So far the reaction from the U.S. government has been muted at best. Treasury Secretary Timmy Geithner released a statement yesterday in which he stated:

“This is an important step, but the test will be how far and how fast they let the currency appreciate. Vigorous implementation would make a positive contribution to strong and balanced global growth.”

Translation: Timmy likes this, but he wants to see more action. While obviously Timmy’s statement may be politically convenient within the confines of the domestic U.S., Chirping Our Creditor has implications in its own right, specifically as it relates to the appetite of the Chinese to continue to fund U.S. deficits. Moreover, a revaluation of the Yuan will fundamentally lead to lower demand for U.S. Treasuries over the long run.

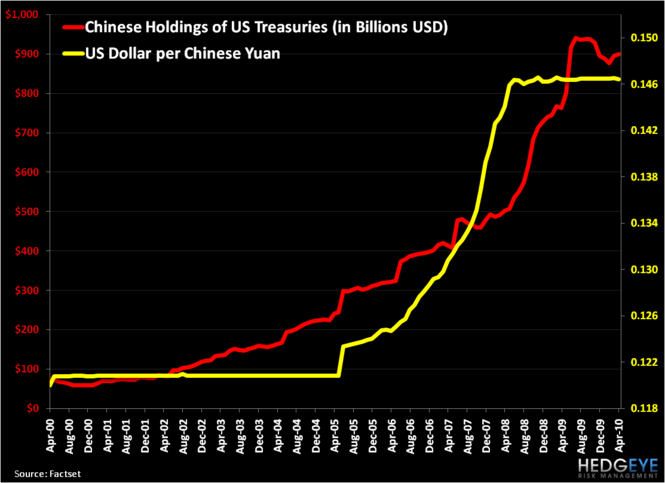

The longer term impact of this change in policy will likely be a decreased demand for U.S. dollars. In order to maintain the fixed exchange rate with the U.S. dollar, the Chinese government had to get long of the U.S. dollar. Their method for doing this was to purchase U.S. Treasury bonds in large sums. With the decision to let the Yuan float, the need to purchase U.S. dollars decreases and with it, on the margin, Chinese demand for Treasuries, which will be negative for the price of Treasuries (and positive for yields). The chart below outlines this point as it shows that Chinese purchased more than $450 billion in U.S. Treasuries over the last two years, while the currencies were pegged, which was almost the same as the prior eight years combined.

So far this morning, the movement in the Yuan has been a bit sleepy. With no specific policy action, the Yuan is still confined to its 0.5% daily trading range. That said, even as this announcement is somewhat rhetorical in the short term, the long term implications are positive:

1) It is indicative of the Chinese showing a willingness to play by the rules of free and open markets, which will increase confidence in investing in China

2) The potential of trade wars will be somewhat alleviated on the margin as the argument that China has a structural competitive advantage due to an undervalued currency is less compelling

3) A stronger Yuan will combat internal inflation within China, which offsets a key potential risk for the global economy – an overheating of the Chinese economy followed by a dramatic decline (think POPPING of a bubble)

As it relates to global trade, a more highly valued Chinese currency will increase China’s purchasing power for commodities, which are priced in U.S. dollars. Therefore as the Yuan appreciates, it will have positive fundamental impacts for those countries that sell commodities into China. Think Australia, New Zealand, Canada, and Brazil. Not surprisingly, the currencies of these nations are acting accordingly and are up between 0.75% and 1.00% across the board today (with Brazil up a little less).

While the movement in the Yuan today may be a bit of yawn, the longer term implications of a meaningful revaluation will have a real investable impact on various asset classes globally. And positioning for this revaluation will be critical.

Daryl G. Jones

Managing Director