THIS WAS ORIGINALLY PUBLISHED ON JUNE 4, 2010. REAL-TIME MACRO CONTENT IS AVAILABLE TO RISK MANAGER SUBSCRIBERS.

____________________

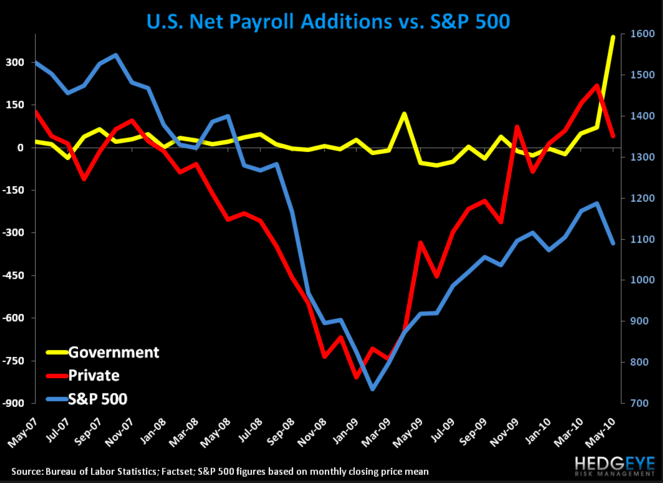

Conclusion: Employment “growth” is anemic and looks weak going forward, which will be a negative catalyst for equities.

Today’s underwhelming Employment report was no doubt made worse by Goldman Sachs Chief Economist Jan Hatzius’ lofty forecast of +600,000 payrolls for the month of May (a +100,000 increase from his previous estimate). While being “a little low on the census contribution” was his chief reason for upping his forecast far above the median consensus estimate of a 536,000 gain, our Hedgeye estimate was that he (and consensus) was “a little too high” on the private contribution. Jan’s estimate was for an incremental 150,000 private payrolls to be added in May vs. 180,000 consensus.

Private payrolls added for the month of May was reported at an anemic 41,000 – first marginal deceleration since December of 2009. After a 9% drop in the S&P throughout the month, and a near 11% drop from the highs of April to the end of May, it was proactively predictable that the rate of job growth would slow on the margin. For clarification, the S&P 500 and Net Private Payrolls have a 0.72 positive correlation over the last three years. That’s an r-squared of 0.53, which suggests some level of statistical significance.

Interestingly, if we normalize for the birth-death adjustment, which we admit is the fodder of conspiracy theorists, and exclude the 215,000 birth-death adjustment, the economy actually lost 226,000 jobs. Even if you aren’t willing to accept that dire of a claim, those unemployed longer than 27 weeks hit a new record coincident with this report at 46%. The likelihood that people just give up hope and drop out of the workforce increases every week with that statistic.

We shorted the QQQs into the close yesterday based on the view that this payroll number was going to be worse than expected. While Hatzuis’ took the shot, and we admire him for that at least, by inflating the whisper consensus number, he actually increased the probability that we would be right on our short call and that payroll additions would be worse than expected by implicitly increasing consensus expectations.

While consensus hiring is boosting over all payroll additions and, temporarily, decreasing the unemployment rate, this payroll report should be framed for exactly what it is . . . a disaster. As we’ve highlighted in the chart below, this is a sequential decline in the addition of private sector jobs and highlights two critical points: a) this is a jobless recovery at best and b) the stimulus package has failed to stimulate any real sustainable jobs additions.

With the stimulus behind us and census hiring also primarily in the rear view mirror, it is likely that the payroll additions will continue to be anemic, and that the actual unemployment rate ticks back up. And that, as they say, is not good.

Daryl G. Jones

Managing Director

Darius Dale

Analyst