Tomorrow at 11 a.m. eastern we will be hosting our August Theme call, titled: “Should U.S. Government Debt Be Rated Junk Status?” The intention of the title is not to suggest literally that U.S. government debt should be rated junk status, but rather to raise a serious red flag as to the emerging deficit and debt problem in the United States and the investment implications therein. If you would like to join the call, please email sales@hedgeye.com.

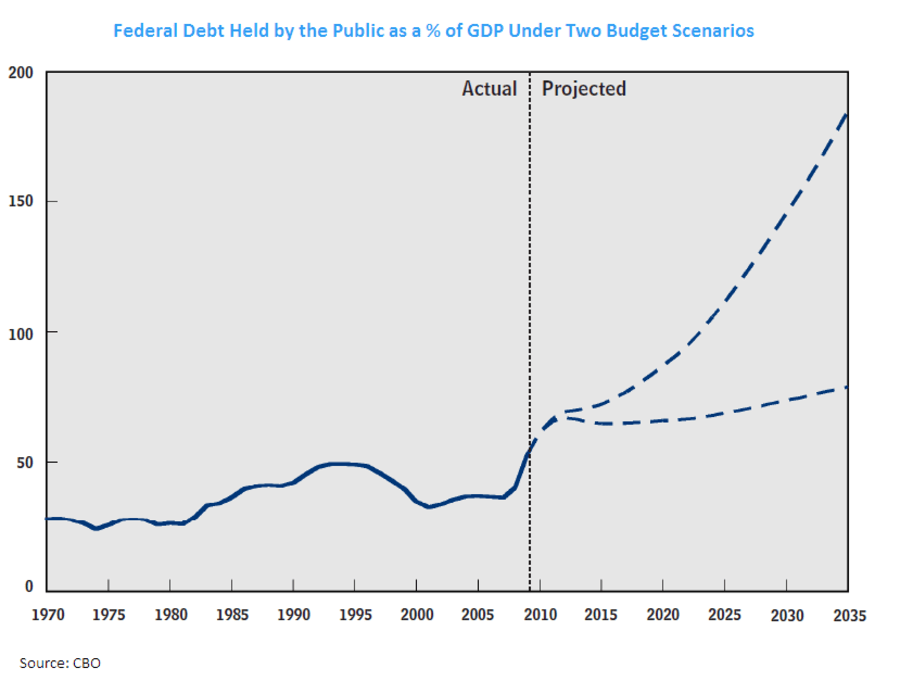

In the chart below, which is sourced from the Congressional Budget Office, the fiscal future of the United States is portrayed based on longer term budget projections. The CBO provides two scenarios for budget projections. In either scenario, the balance sheet of the United States sees a continued build-up of debt for the ensuing two decades. In the more negative scenario, debt as a percentage of GDP accelerates dramatically over the coming decades, eventually approaching near 200%.

As we will discuss in greater detail tomorrow, the primary implication of a build-up in debt on the federal balance sheet is a dramatically different future as it relates to underlying growth. If the last 200 years of data has shown us anything, it is simply that those nations with high debt balances either default or grow well below mean rates as long as debt ratios remain high.

We, of course, aren’t suggesting that the U.S. is bound to default anytime soon, but there are implications of an accelerating U.S. debt balance that we need to keep front and center. One longer term consideration is simply that investors, both domestically and abroad, begin to lose confidence in U.S. government debt particularly at the current all-time low interest rates. An increase in interest rates has meaningful implications for the U.S. budget. According to a paper from the CBO today titled, “Federal Debt and the Risk of a Fiscal Crisis”, a 4-percentage across the board increase in interest rates would raise interest rate payments by more than $100 billion on an annualized basis.

A conclusion of our analysis tomorrow will be that the future will look much different than the most recent past in terms of the economic outlook of the United States over the coming years. And the reality is, as debt grows and confidence wanes, the likelihood of a fiscal crisis of some magnitude grows. In that scenario, as the CBO also wrote today, there are three primary prescriptions for the United States:

“restructuring its debt (that is, seeking to modify the contractual terms of existing obligations); pursuing inflationary monetary policy (that is, increasing the supply of money); and adopting an austerity program of spending cuts and tax increases.”

Is a fiscal crisis in the United States imminent? Perhaps not, but the future of the U.S. government balance sheet is bleak based any reasonable federal government budgetary assumptions. We hope you can join us for the discussion tomorrow at 11 a.m. eastern.

Daryl G. Jones

Managing Director