“All truths are easy to understand once they are discovered; the point is to discover them.”

- Galileo Galilei

The penalties for non-consensus thinking were harsher 400 years ago. In 1610 Galileo published his observational studies of the moons of Jupiter as evidence in support of Copernicanism and a heliocentric model of the solar system. At the time, most astronomers still believed in a geocentric model and considered a heliocentric model outrageous. Galileo’s work was derided by many of his contemporaries and, ultimately, Galileo was brought before the Roman Inquisition for heresy, tried, found guilty and forced to spend the rest of his life under house arrest.

Fortunately in today’s world the penalties for having a non-consensus view generally aren’t as severe. That said, it can still take a long time for certain entrenched assumptions to change and evolve, which brings us to the subject of today’s Early Look. One such entrenched assumption in the investment community today is that home prices are unlikely to fall materially from here.

For those unfamiliar, our view on housing is bearish and our argument relies principally on supply and demand data, and the imbalances that exist between them. Our analysis has sought to both measure and quantify the effects of dislocations in supply and demand in housing and the lagged effects these imbalances have on home prices. Our conclusion is that based on the current supply and demand imbalance, prices will be 15-20% lower in 12-18 months on a national basis. This is an overly simplistic summary of a 100+ page presentation we’ve assembled on the subject, but below we present just a few of the facts worth considering.

Consider the following. There are currently 3.99 million homes on the market for sale as of the end of June. Existing home sales were 5.37 million (seasonally adjusted annualized rate) in June, which equates to 8.9 months of supply. This is disingenuous, however, as June existing home sales represent April contract activity. We know that post-April pending homes sales are down over 30% through May and June. As such, we would expect a comparable decline in existing home sales once the data rolls through on a lag later this month. In other words, existing home sales for July/August will be in the ~4 million range, which will be a wake-up call to the Panglossian bulls. Assuming inventory remains around 4 million this will equate to ~12 months of supply. The market is often considered in equilibrium when inventory is 5-6 months of supply. For reference, 12 months will be the highest amount of supply seen since the housing downturn began. This 12 months figure does not include shadow inventory, which likely represents an additional 4.2 to 6.0 million homes (according to estimates from the Mortgage Bankers Association, the Federal Government’s HAMP Program, and Lender Processing Services, the largest mortgage default processor in the country.)

Laurie Goodman, a Senior Managing Director with Amherst Securities, one of the leading providers of mortgage data analytics, recently published a paper in the Financial Analysts Journal entitled “Dimensioning the Housing Crisis” in which she submits that from the beginning of the crisis (YE06) through today there have been 1.5 million homes liquidated through foreclosure and short sale. During this timeframe, depending on which housing series you use, home prices have fallen 20-35% nationally. Using conservative assumptions, she concludes that a further 11-12 million homes will be liquidated in coming years. If 1.5 million liquidations coupled with broader supply/demand imbalances triggered 20-35% downside in home prices, consider what 11-12mn liquidations will do amid a more severe underlying supply/demand imbalance.

While the government has intervened over the past 18 months to try and arrest the rate of decline in home prices, we think their efforts have merely kicked the can down the road and have done little to alter the underlying nature of the problem. Ultimately, the pressure from foreclosures will outstrip the government’s ability to hold back the supply.

Touching briefly on the demand side of the equation, demand for mortgages as measured by the MBA Purchase Index has been steadily falling for the last five years. After averaging 471 in 2005, the Purchase Index fell to 264 in 2009 (-44%). 2010 to date is down to 209 (-55%). The month of July averaged just 170, a 64% decline from 2005. For reference, 2010 year-to-date demand is consistent with demand last seen in 1997-1998, while July demand is consistent with levels last seen in 1995.

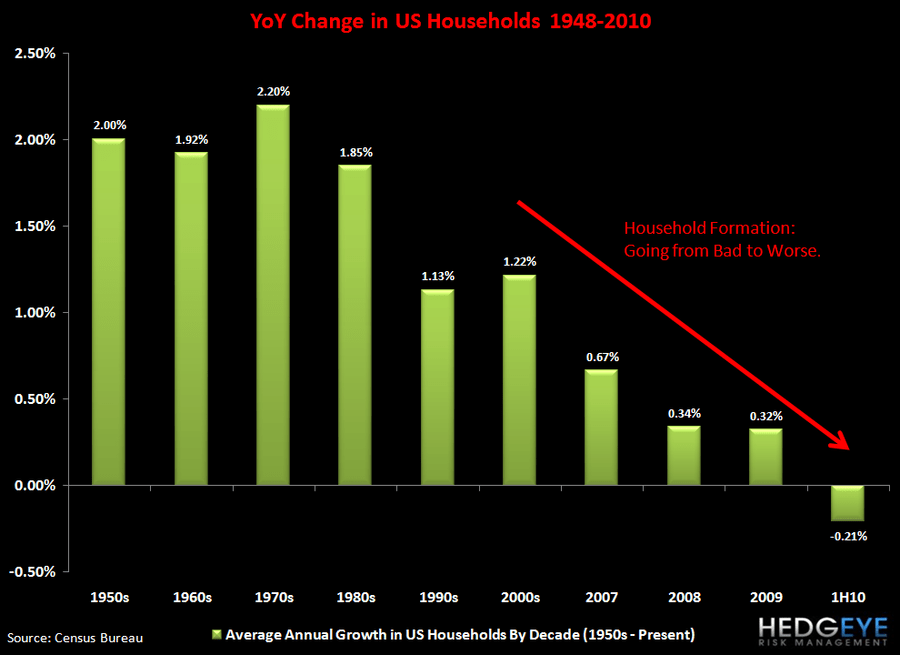

It seems obvious to us that home prices are headed materially lower from here, yet many people – most in fact – don’t agree. There are a host of reasons we’ve had explained to us why home prices shouldn’t go down from here. The most oft-cited is the demographics argument, namely that there should be solid net new household formation over the next several years that will drive marginal demand for homes high enough to absorb existing supply, shadow inventory and whatever other pressures might come down the road.

It’s foolish to dismiss criticism out of hand without first thinking it through – especially when multiple investors are telling you the same thing. To that end, we’ve analyzed the core of the argument that household formation is set to take off, and what we’ve found is quite interesting. The chart at the end of this report shows data that we don’t think many people are aware exists. It represents real household formation rates through June 2010. We have the data monthly – not many people do. What is striking is that it shows that in the first half of 2010 the number of households in the US actually shrank. This is the first time this has happened since the data series began, and our data goes back to the 1950s. Moreover, negative growth in 1H10 follows anemic growth in 2008 and 2009.

Why is this? Normally, some 60% of net new household formation occurs in the 20-29 year old demographic. It’s typically at this age when a young person moves away from home and, in doing so, a new household is created. The catch is that unemployment is at 9.5% nationally, and the unemployment rate for this age cohort is well into the teens. Remember, household formation is a derivative of confidence, which itself is merely an extension of the employment environment. This lack of confidence must be having a profound effect across the country for the number of households to actually be shrinking.

Will this change? The relationship between the economy and household formation is reflexive, to borrow a philosophical concept from George Soros. That is to say, when times are good household formation drives the economy amid a virtuous cycle, but when times are bad the economy will suppress household formation, which, in turn, feeds back negatively into the economy in a vicious cycle. The latter is the dynamic that exists today.

Our firm is of the strong view that US economic growth is poised to decelerate meaningfully in the back half of the year and into 2011, which will keep a lid on hiring. This will in turn keep the lid on household formation, the one credible case for a pick-up in housing demand.

Josh Steiner

Managing Director