Note to SKX management: C’mon guys…don’t get lost patting yourself on a job well done with Shape-ups (and it was, in fact, a job well done). But switch gears and deploy capital in a way that will prevent another blow up. The Street’s over $4.00 in ’11. I can get closer to $2.50.

Yes, it was a love fest on the SKX conference call. Shape-ups, product mo, blow-out quarter, etc… I get it, and so does the consensus. But there are some bigger questions to be asking here – and the answers don’t give me one iota of confidence in the sustainability of this business model or growth trajectory. Consider the following…

1) Shape-ups now account for ~25% of total sales according to our estimates, and accounted for 75%+ of growth vs. last year. Excluding Shape-ups, sales were likely up +10-15%. I will never take anything away from a company that is printing revenue based on hitting – and even creating – a trend. But we also cannot straight line this performance in perpetuity.

2) Industry-wide, ‘toning’ went from ~2.5mm pairs, at an average price point of ~$95 in 2009 to a current annual run rate closer to $1.2-$1.5Bn, 15-18mm pair at $80-$85, respectively. SKX’ share is roughy 60% and has trended down recently as Reebok sales ramped up. Let’s face it folks, with fashion, nothing attracts a crowd like a crowd. Now Payless is selling them for $29.99 with a BOGO (buy one get one half off) and it is 1% of sales today moving towards 6% by year end. That alone would represent ~8% of the industry’s unit share in this category.

3) Why does all this matter? SKX cannot afford either a slowdown in unit demand or ASP compression in this category. Period.

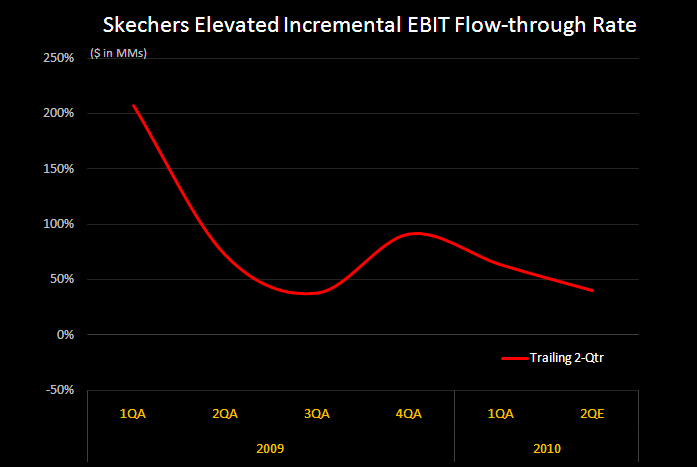

4) Why? Because SKX deploys capital throughout its organization when it can, not when it should. Even today the company is deferring new DC and related equipment spend into next year. Since launching Shape-Ups in early 2009, better than 55% of incremental revenue has landed on the bottom line as outlined in the chart below. After COGS and incremental store build costs alone, this should result in flow through less than 50%. Then add on capacity expansion (DC and equipment, but more importantly, people to crank on R&D and Sales/Marketing to play offense against potential pressure in toning). No one knows the exact flow through needed, but my math suggests that it's closer to 30%.

5) The bottom line with margins is that this company should realize about a 600bp boost in margins this year. If we’re going to give the model any shot at sustainability, then they should be investing more, and printing margin improvement that is half what we see today.

6) In addition, despite higher product costs due to labor, commodities, transportation, yuan, etc… SKX is guiding to higher Gross Margins – which is anomalous and raises a red flag with me as to the sustainability.

7) Longer term, lets not forget that SKX is massively net short Yuan. With 90% of its product sourced in China and less than 5% of its revenue generated in China, this is a pretty steep delta against a freight train of a long-term Macro backdrop for the Yuan. Nike, on the flip side (and even Adidas) only makes 26% of product in China. So it has $10bn in COGS, and $2.6bn in rmb exposure. But it has a growing and profitable China revenue engine, that stands at about $1.8bn today. I could make a strong case that Nike is net long the Yuan within a 2-year time period. That puts it near the top of any other consumer-related multinational that has such favorable exposure. Skechers? Not quite.

8) The punchline? We’re going to see the sales delta slow within 2-quarters, which is the same time that prices in the toning category will be more competitive. Then higher product costs will matter, as will deferred infrastructure investment. Add that all together and it’s not unrealistic to get to 2011 being a down year. The point is that estimates are likely to come in over $4 in 2011 after this quarter. But $2.50 is perfectly within reach – and more likely. When SKX misses, it will get a 10x pe at best. That’s a $25 stock, or 33% down from here.

9) Timing: Will this deck of cards come crashing down next week? I dunno. I doubt it, actually. But I don’t think we have to wait a year, either. Looking at the quarters ahead, and synching with product flow, and competitive climate, I place a 60% chance it happens before Dec 31, and 80% before the end of 1Q11. I’ll work closely with Keith and let him make the call as to what to do in the interim from a TRADE and TREND perspective. But if I owned this name today, I’d be punting it.