R3: REQUIRED RETAIL READING

July 26, 2010

The toning craze may be more about perception than reality but it still has blossomed into a meaningful business over the past year. Next up is Skechers’ effort to tap into the men’s market by changing the product’s name from Shape-Ups to the Skechers Resistance Runner. Is the male the customer ready for this?

TODAY’S CALL OUT

Over the weekend we were struck by the frequency of Skechers’ latest television campaign featuring a men’s running shoe. Clearly a major and costly effort is underway to try an build a men’s “toning” business, but this time it’s disguised as a “running” shoe. The product dubbed the Skechers Resistance Runner or SRR is clearly aimed at the male consumer, who is not likely interested or just flat out embarrassed to wear a toning product. With the toning market almost entirely focused on women, it was only a matter of time before a strategy emerged to take aim at men. Initial efforts to engage the male customer with identical take-downs of the female products have likely been slow to materialize. As a result, we now have a $149.99 Skechers running/toning hybrid.

And while we never like to make a call on product or fashion alone, we’re going to go out on a limb here and suggest that the male consumer is not dumb. Merely changing the name of a shoe from “toning” to “running” and dropping the brand name Shape-Ups is not likely to fool anyone. Furthermore, combining the toning sole with a Nike-esque silhouette and then charging only $10 less than the comparable Nike marquee product seems even more ludicrous. Take a look at the $150 Skechers shoe vs. Nike’s $159 Air Max+ 2009 below.

LEVINE’S LOW DOWN

- According to the Compete Online Intelligence report, one in three consumers researches a purchase online before making it in a store. The primary drivers of the research online but purchase in-store include cost, convenience, and the need for a tactile experience. Interestingly, consumer electronics, kitchen products, home furnishings, home improvement, and movies/music/games are the categories consumers research most but then purchase in store. Over 40% of purchases in these categories are researched online and then bought in a store.

- Nordstrom isn’t the only retailer collaborating on a Twilight apparel and accessories line. This time UK retailer, Marks & Spencer, is launching a men’s underwear collection in conjunction with the movie’s star, Robert Pattinson. Called “R-Pants”, the new line of undergarments are meant to appeal to a younger demographic than the traditional M&S customer. Oh and by the way, 25% of all men’s underwear in the UK is purchased at the Marks % Spencer.

- Whether it’s the Walgreen’s influence or many years in the making, word has it that the latest iteration of Duane Reade remodels in Manhattan are generating some buzz. While some of the remodeled stores were an upgrade from prior, poorly laid out locations the new ones are being compared in some ways to Sephora and Target. Open-sell (and more upscale) cosmetics, a mini-fresh food/supermarket department, and a noticeably increased number of registers are all hallmark’s of the company’s latest prototype. It’s been a long time since NY consumers actually wanted a Duane Reade in their ‘hood and this may finally be a reason for New Yorkers to shed their negative views on the tired brand.

MORNING NEWS

Body Central IPO - Body Central Acquisition Corp. filed a shelf registration statement with the SEC for an $86.3 mm initial public offering. Founded in 1973, the value-priced retailer operates 196 stores under the nameplates Body Central and Body Shop across 23 states. It sells apparel and accessories under the labels Body Central and Lipstick. The Jacksonville, Fla.-based specialty apparel retailer’s primary customers are women in their late teens and 20s. The symbol will be BODY and Piper Jaffray and Jefferies & Co. are the co-lead underwriters. <wwd.com/business-news>

Hedgeye Retail’s Take: Another value-focused fashion retailer going down the IPO route. Unfortunately, the company’s fashion positioning and price points do little to differentiate from the numerous other mall concepts chasing the same customer demographic.

Everyone's A Critic Online - In today’s era of online shopping, consumer reviews are taking the place of word-of-mouth buzz. Instead of friends telling friends about their shoe purchases, reviewers potentially have the ear of the entire Internet universe. That’s a risky proposition for brands. Less-than-favorable comments on issues from fit to flexibility can negatively impact comfort companies. Still, industry sources agree that honesty remains the best policy. Most retailing sites post all reviews in their entirety. A recent Nielsen Global Consumer Report on Internet shopping found that 42% of North American consumers said online product reviews were useful to them. At Zappos, about 1,500 to 2,500 reviews are posted each day across all footwear categories, said Matt Burchand, senior director of content at the Henderson, Nev.-based website. <wwd.com/footwear-news>

Hedgeye Retail’s Take: Nothing new here except that we suspect companies aren’t always honest with letting their customers post their free-flowing thoughts. The recent iPhone 4 debacle is a case in point. According to some tech blogs, negative consumer comments posted on apple’s forums were removed by the company during the initial wave of negativity. Is censorship the next big issue for consumers?

Volcom to Acquire Australian License - Volcom, Inc. signed an agreement to acquire the Volcom licensee in Australia. Terms of the transaction were not disclosed. The company anticipates the acquisition, which is expected to close in the third quarter, to be neutral to earnings in 2010. <sportsonesource.com>

Hedgeye Retail’s Take: While none of the company’s recent activities is a game changer, it’s worth noting the Volcom has been one of the more active names in the M&A space lately. Even after the bid for West 49 was dropped, Volcom managed to pick up a California lifestyle brand as well as its Australian licensee.

Zara Stores Open in India - Moving fast in the Indian market, Spanish retailer Zara opened three stores in the country within five weeks. The brand made its debut on the Indian market through a joint venture with Trent Ltd., the listed retail arm of the $70.8 bn Tata Group. Trent already has a presence in the retail industry with Westside stores and Star Bazaar hypermarkets. Inditex controls 51% of the joint venture, while Trent Ltd. owns 49%. Current regulations on foreign direct investment in India stipulate that foreign single-brand retailers must pass a 49 percent stake on to a local partner. According to a June report by McKinsey & Company, Indian apparel sales are forecast to reach $25 bn this year, having grown in excess of 10% over the past five years — a growth rate faster than that of the overall India retail market — and the trajectory is expected to continue over the next five years, doubling within that time period. <wwd.com/business-news>

Hedgeye Retail’s Take: Keep an eye on the loosening of the foreign direct investment laws, which many now believe may soon be relaxed. As such, we’d expect many brands and retailers to begin to dip their toes in the Indian market as they prepare for potential growth. If McKinsey is even half correct on its apparel sales estimate, then there is a long, long road ahead for apparel growth in this market (provided the consumer is even remotely interested in foreign brands).

Bangladesh Ranks 4th Largest Garment Exporter - Bangladesh has been ranked the world’s fourth largest garment exporter, contributing around 3% of total exports, according to the World Trade Organization. The 30-year-old RMG industry of Bangladesh has transformed into a global sourcing destination. Bangladesh is the biggest exporter of cotton T-shirts and stands second in exporting cotton pullover and jeans to European countries. As also the country, in terms of volume is the second biggest exporter of cotton trousers to United States. Currently, Bangladesh in its more than 5,000 garment manufacturing units employs around 2 mm people, of whom 90% are women. <fashionnetasia.com>

Hedgeye Retail’s Take: While Bangladesh’s importance in the world of apparel sourcing continues to grow, it’s worth noting how fragmented the sourcing base remains for the category. As the 4th largest exporter, the country’s share of exports is just 3%. This should serve as a reminder that at least for now, there are many, many options for which a brand or retailer can source garments in a cost effective manner across the globe.

Footwear Manufacturers Continue to Move to Indonesia - Six Taiwanese and South Korean shoe makers are relocating their factories from China and Vietnam to Indonesia, which will create an additional income of US$550 mm for the country, said the Indonesian Shoes Association (Aprisindo). Due to increasing labor costs and raw material issues in China and Vietnam, the six manufacturers, which have been outsourcing a significant amount of shoes and products for leading footwear brands like Nike, Adidas, Reebok and Geox, are expected to finish the relocation by this year-end mainly to East Java. <fashionnetasia.com>

Hedgeye Retail’s Take: Indonesia continues to be the biggest beneficiary of rising costs in China, which at least for now should continue to benefit. However, as wages and material costs rise in China and manufacturing leaves the country, we would not be surprised to eventually see some sort of duty or VAT rebate measures to help keep Chinese factories and workers employed.

Japanese Retailers Win In Summer Heat With Non-Smelling Underwear - Japanese retailers are headed for hot summer sales of cheap beer and non-smell underwear, driven by above-average temperatures and consumers with fatter wallets. Sales of the products are beating projections, said Hiroshi Katsuno, manager of Goldwin’s Maxifresh underwear group. “Data from our experiments show that one shirt can absorb smell coming from four liters of sweat,” he said. The Uniqlo chain, owned by Fast Retailing Co., has increased sales of sweat-absorbing, quick-drying underwear even as overall sales slowed in the three months through May. <bloomberg.com/news>

Hedgeye Retail’s Take: If ever there was a time for Under Armour and its anti-cotton, moisture wicking products to gain acceptance now appears the time. While we hope warmer temperatures aren’t here to stay permanently, the need for innovation in textiles is clearly heightened by global warming.

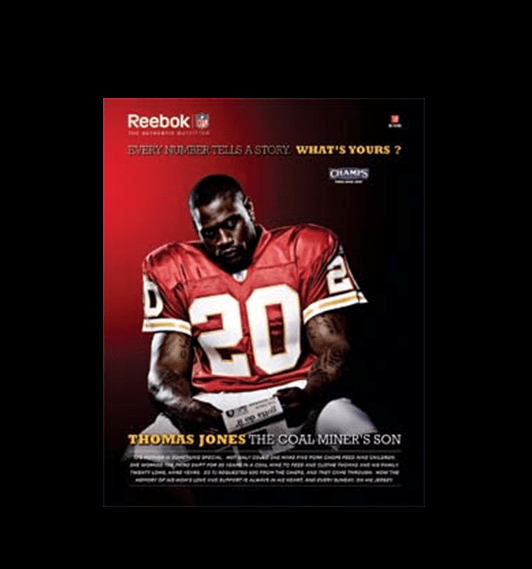

Reebok To Blitz NFL Jersey Market - Tennessee Titans quarterback Vince Young celebrates the day his mother was born, wearing No. 10 for her June 10th birthday. And Jacksonville Jaguars running back Maurice Jones-Drew recalls the teams that turned him down to play pro football—that would be all 32 in the draft—with No. 32 emblazoned across his chest. There are some of the stories behind those NFL jerseys, according to a marketing campaign breaking next month via M&C Saatchi Sport & Entertainment. The print and retail ads are part of a collaboration among longtime NFL sponsor Reebok, the NFL Players Association and the Champs sporting goods chain that will try to energize sales of the apparel category dubbed names-and-numbers after years of focus on women, performance and lifestyle merchandise. The campaign, running through September, will have a dedicated Web site with video footage of players like New York Giants quarterback Eli Manning and safety Kenny Phillips, Kansas City Chiefs running back Thomas Jones, and other stars talking about the origins of the numbers they wear. More than 600 Champs stores will get extensive signage, crew T-shirts and POP for the seven-figure program under the tagline, “Every number has a story. What’s yours?” <brandweek.com>

Hedgeye Retail’s Take: Another minor victory for Foot Locker and Champs, which should benefit from this collaboration with Reebok and the NFL. Recall that Champs has also partnered with the NBA to create shop-in-shops focused on local teams depending on store’s location. We continue to believe closer collaboration with the brands and in this case, the leagues, is one of the key components to the company’s turnaround efforts.