2Q brought about a sharp upswing in comparable store sales.

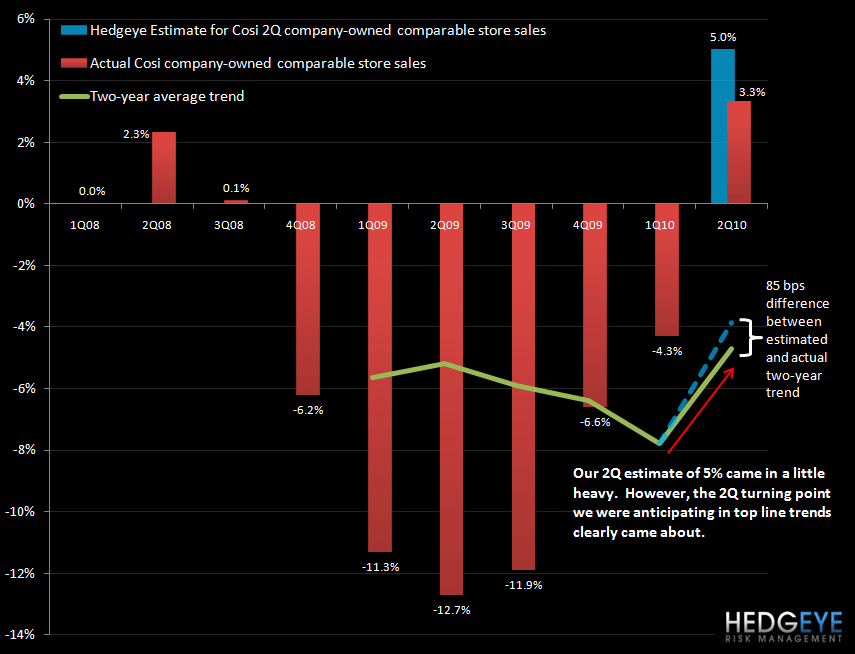

On 6/25, I wrote a post titled “COSI – SALES MOMENTUM IN 2Q” detailing my view that 2Q10 would bring a sequential improvement in same-store sales, driven by product initiatives and marketing efforts. Company-owned comparable store sales for 2Q came in at 3.3%, versus -12.7% in 2Q09 and -4.3% in 1Q10. On a two-year basis, this implies a 310 bp sequential improvement in top line trends. Our comparable store sales estimate from 6/25 of +5% implied a two-year trend sequential improvement of 395 bps – a difference of 85 bps.

This result is encouraging but what gives me additional conviction on the story is that comps in June came in at +5.5%, indicating that trends were improving throughout the quarter. In the press release, President and Chief Executive Officer of Cosi, James Hyatt, said that the strong performance was largely due to the company’s “expanded marketing efforts” aimed at broadening consumer reach and driving traffic in multiple dayparts. Traffic trends at Cosi improved from -5.6% in 1Q to +3.1%. On a two-year basis, trends improved by 410 bps sequentially.

Howard Penney

Managing Director