YUM is scheduled to report 2Q10 earnings after the close on Tuesday. On an EPS basis, my estimate is coming in light, at $0.50 versus the street’s $0.54 estimate, but given the company’s track record of beating expectations, I would not be surprised if numbers came in above my estimate.

Going into the quarter I continue to have two primary concerns, largely related to what I recognize as overly aggressive unit growth in China and profitability issues in the U.S.

CHINA:

Despite the expected sequential slowdown in same-store sales growth in 2Q10 on a 2-year average basis (management’s guidance implies a 300 bp deceleration), I don’t think the issues in China will become more apparent until the second half of 2010 when restaurant profit margin should decline YOY. Specifically, management pointed to commodity inflation and increased wage inflation in the back half of the year. It is important to remember that restaurant margin growth in 1Q10 was driven primarily by commodity cost deflation of $15 million.

Although same-store sales improved significantly in 1Q10 on a 2-year average basis, I don’t think this trend is sustainable (again, management’s 2Q and FY10 guidance implies a deceleration). Any slowdown in same-store sales growth will take a toll on margins as the company faces commodity and wage rate headwinds in 2H10.

As shown in the chart below, YUM China has been operating in what we call “Nirvana”, when both same-store sales and YOY restaurant profit margin growth are positive. YUM should remain in Nirvana territory in 2Q10, but trends should get more difficult in 2H10, with the company potentially falling into “Deep Hole” territory (negative same-store sales and YOY decline in restaurant level margin) in 3Q10 and “Trouble Brewing” territory in 4Q10 (positive same-store sales and YOY decline in restaurant level margin).

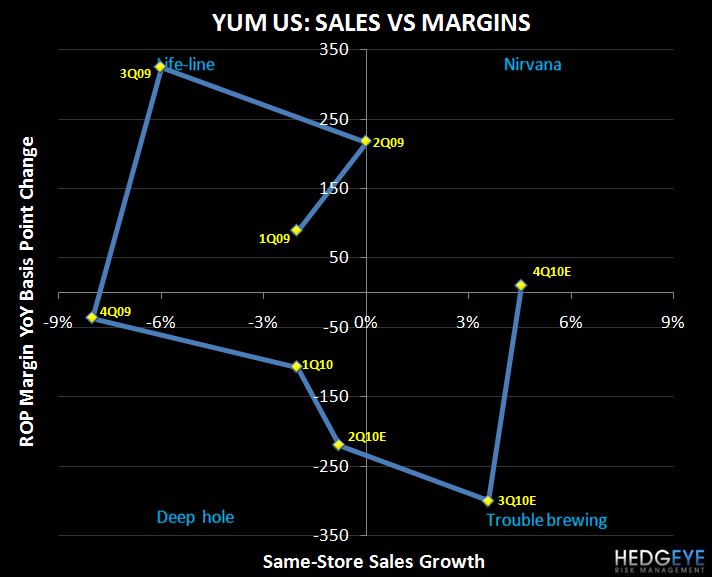

For reference, when we think about the four quadrants outlined below, we recognize the trends associated with operating in both the “Life-Line” and “Trouble Brewing” territories as unsustainable. Broadly speaking, if a company is posting positive same-store sales and declining margins (Trouble brewing), the company is unable to leverage its positive top-line and is therefore spending too much (often a result of growth related costs).

Within “Life-Line”, a company’s margins continue to grow despite negative same-store sales growth. A lot of restaurant companies have operated in this quadrant in recent quarters as they have focused on cutting costs to offset the difficult sales environment. A company cannot cut costs forever without hurting the customer experience so margins will eventually follow the direction of same-store sales growth.

U.S.:

YUM is facing its most difficult same-store sales comparison in 2Q10 as it laps the Kentucky Grilled Chicken launch and a +3% comp at KFC (the only positive comp at KFC in 2009). That being said, I am expecting same-store sales in the U.S. to improve slightly in 2Q10 from 1Q10 on a 2-year basis, primarily as a result of the new $2 combo meal at Taco Bell (lower drink and combo sales hurt 1Q10 trends) and the Double Down at KFC (which was reported to be on the menu indefinitely after initial plans introduced it as an LTO).

During the first quarter, U.S. profitability was hurt by an increase in the number of consumers buying off the “Why Pay More” menu at Taco Bell. Even if same-store sales get better in 2Q, this value menu will likely continue to be an important driver of traffic growth at the concept. This combined with the fact that commodity costs should turn inflationary in the U.S. and the YOY restaurant profit margin compares get increasingly difficult for the next two quarters should continue to put pressure on U.S. profitability.

The chart below highlights that U.S. same-store sales and margins have suffered for some time now, with the company operating in a “Deep Hole” for the last two reported quarters. YUM will likely remain in a “Deep Hole” in 2Q10 but should then recover somewhat in the back half of the year as it emerges from the “Deep Hole” and potentially moves into “Nirvana” territory in 4Q10. This expected recovery is largely a function of easy comparisons in 2H10 (as management pointed out on its 1Q10 earnings call). YUM is lapping -6% and -8% same-store sales from 3Q09 and 4Q09, respectively.

We will have to see how same-store sales track for the rest of the year in the U.S. (QSR trends, on average, continue to be choppy), but I continue to think that YUM’s full year U.S. operating profit could fall short of the company’s guidance of 5% growth (I am currently modeling nearly 3% growth with the bulk of that growth coming in 4Q10 when the company is lapping a 23% decline from 4Q09).

Howard Penney

Managing Director