Initially, this onion smells punk. But when you peel back a layer or two, you see that growth is coming from the right places, and the US is inflecting. Oh, and by the way, guidance is ridiculous.

About 16 hours ago, I was sitting in our conference room in New Haven telling Keith and the rest of our investment team that I’m well ahead of the consensus for Nike. Given that there’s enough levers here such that Nike can print almost anything it really wants, I said that the one number I would be genuinely disappointed to see is a single-digit revenue growth rate. I was at 11.4% vs. the Street at 8.9%. We saw 7.7% -- not good.

Yeah, futures looked good, both in absolute terms and the trajectory. Also, inventories were down 13% on top of 8% revenue and 7% futures growth (+10% futures in constant $). The balance sheet was like an impenetrable wall of iron.

Some people might like the penny beat. But let's face it... Nike ALWAYS beats and guidance was cloudy at best. I’m staying true to my earlier comment/concern on revenue. The good news is that many parts of guidance make absolutely no sense to this (self-proclaimed) rational thinker. Also, when diving into the top line, I’m seeing the composition look better than it might indicate at first blush.

Here are some key puts and takes (in no particular order)…

1) On revenue growth: There are actually encouraging signs from key parts of the business.

- US: North America revenue operating margins and futures all accelerated. In fact, when we look at the math behind the 8% futures growth number, we know that apparel (25%) of total was up mid-teens, which suggests that footwear is up around 6%. Either Nike’s share gain in the US is accelerating materially, or the market (in product other than toning!) is beginning to accelerate. We’ll take either.

- The biggest disaster of the quarter was Western Europe. 2% revenue growth, and a 17% decline in EBIT. Perhaps I’m being harsh given that constant dollar futures accelerated from 0% to 7% to 11% over the past 3 quarters. But they gave it all back in FX (from 12% to 11% to -2%). Maybe the metaphor of Western Europe failing to show up at the World Cup is still fresh in my mind and I’m clouding the two. But with EBIT margins down in the qtr by 470bp, you can’t blame me.

- Central and Eastern Europe: Here’s some irony for you…but the same countries whose teams are surprising on the upside at the Cup are also doing the same on Nike’s P&L and order book. A coincidence with close to zero investment significance, I know. But humor me...

- China is crushing it. Teens revenue growth, with margins up 266bps ON TOP OF 923bps improvement last year. As we’ve noted, China is approaching a $2bn revenue organization for Nike. With a 15-20% growth rate, and less than 30% of its $10bn in COGS sourced in China, we’re approaching a point where a floating Yuan is a wash for Nike – which gives it a competitive leg up.

- Japan: The Japanese economy has done a whole lot of nothing for what -- 20 years? Nike’s business is doing much of the same. Seriously, I’m beginning to wonder why they even do business there.

- Emerging Markets: 46% EBIT growth and 30% futures??? They’re crushing it here.

The bottom line is that we’re seeing solid growth in the most important regions – such as China, Emerging Markets, Central/Eastern Europe, as well as an inflection point in the US. Results are being dinged by Western Europe and Japan. The former is particularly important, as we can’t flat out ignore it. But the US is 1.7x the size of Western Europe. If the US turn continues, which we think it will, then it could offset much of a Western Europe decline.

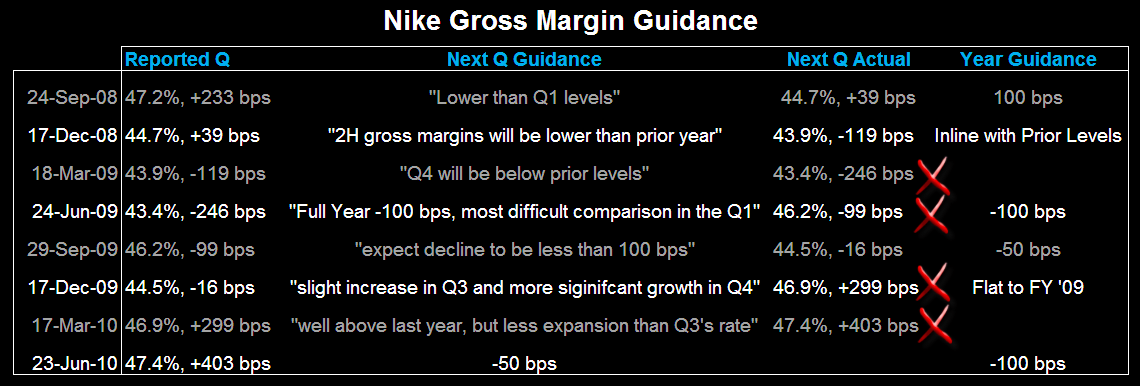

2) Gross margin guidance. I was pretty surprised to hear the company note that full year gross margins should be off by 100bp this year. Actually, my surprise very quickly turned to doubt. Much of the rationale was chalked to FX. But let’s face two facts…

- As much as the $/Euro has been all over the map in recent weeks, the weighted average impact across all of Nike’s trade partners is quite benign over the next 4-quarters using prevailing FX rates. Check out the chart below. Prior quarters of major (-100bp+) GM erosion was the result of a -5%-7% FX hit. We’re not anywhere in that ballpark today.

- Another point is that the facts show that the company’s least reliable guidance metric has been gross margins – by a long shot. Check out the accountability grid below. It shows what they said vs. what they did. Not exactly predictable. Our strong view is that conservatism won over this time around due to global risk factors, and the fact that they’re just heading into their 1Q11 and want a hurdle that they can clear with their eyes closed.

NIKE: YouTubing Gross Margin Guidance

3) Acquisitions. For the first time ever, I am baking acquisitions into my Nike model – which normally goes against what I stand for. But there are four reasons why…

- NKE’s cash and short term investments are topping $5bn, or $10.50ps.

- We continue to see decoupling between ROIC and ROE, and both management and the Board knows it, and does not like it.

- Bernanke pandered yet again yesterday – in effect keeping the return on Nike’s hard-earned cash close to zero. While I don’t think they’ll relax standards, even an ROIC dilutive acquisition would be better than 0%.

- The acquisition strategy will be focused on buying licenses of brands it already owns and controls – as hinted at the analyst meeting. Converse outside of US/Canada is the best candidate. I’m assuming $500mm in acquisition capital spend by end of calendar year with a 10% yield. Then I’m assuming assuming $1.5 in repo and 25% growth rate in dividend.

4) Non-op income: Here’s another change to the model. With lower revenue and gross profit from FX (even though I am haircutting vs. the co’s guidance) we need to take up non-operating income due to higher marked-to-market on FX hedges.

5) Check this out... There has been only one quarter in the history of Nike where the cash cycle (Days Recievable + Days Inventory less Days Payable) has been less than 90 days. This quarter it came in below 75. No joke...

When all is said and done, I’m at $4.55 for this year, and $5.45 for next. That’s a dime below my estimate heading into the quarter. Though I suspect that by the time the Street is finished hitting plug-n-play on their models, I’ll end up 10-15% ahead.

As noted earlier today, one of my main concerns is any sort of ownership rotation this name goes through as there is a transfer of earnings from the gross profit line, to SG&A leverage and non-operating income as it relates to how the company manages risk in its business to keep plowing forward.

Yes, I’m disappointed by the revenue. The Street’s numbers will be all over the place based on the guidance. But quite frankly, I don’t know which one of those two I trust less. But there’s much to the components of the quarter that give me the confidence that Nike is executing on the core plan I think is necessary to create value for shareholders.