“Who will guard the guards themselves?”

-Juvenal

In recent writings, I’ve been focusing on the events that led to the fall of the Roman Empire. I’ve been trying to wrap my head around the dynamics of politics and power in societies that are dominated by professional politicians as they finally hit their tipping point.

I have a profound respect for economic and political history, not because it’s ever the same, but because the patterns of human behavior often rhyme. I’m certainly not an expert on Rome pre 49BC when Julius Ceasar crossed the Rubicon, but in hindsight I can see as well as you can. The outputs of certain abuses of power become crystal clear.

One of the best parts about my job has turned out to be putting myself at the very heart of an exclusive network of thought leaders. Every morning I basically have an opportunity to inspire a debate. The more outside of consensus I get, the louder the feedback mechanism of the Hedgeye network becomes.

The aforementioned quote came from one of our many thoughtful subscribers. He’s studied the aftermath of what I have been writing about as of late. Juvenal was a Roman poet from the 1st century AD. I consider myself very fortunate to be privy to thoughts like these – it’s always important to consider what winners in this business are thinking. Collaborative thought is a critical driver of risk management.

Our subscriber wrote:

“Through his Satires of Juvenal, who once asked, “Quis custodiet ipsos custodes?” Effectively meaning, “Who will guard the guards themselves?” (along with other similar, idiomatic translations) the question posed by Plato and put to Socrates as the main character in The Republic, is as proper now as it was more than 2,000 years ago. With Fiat Fools and global government incompetence accelerating the journey down the Road to Perdition, every free market thinker should ask, and then answer for himself, this question.”

Sometimes it’s that simple – risk management, that is. Sometimes the best absolute performance is assigned to whomever is able to contextualize all that’s going on in this interconnected world and ask themselves the right question first.

Answering the question of “who will guard the guards” of the Fiat Fools becomes less and less clear by the day. Whether it’s Jean-Claude Trichet talking circles around the ECB’s bailout program this morning or Alan Greenspan doing his best to attempt to dislodge himself from the problems he perpetuated, this all seems to be heading the same way. The guardians of debt financed deficit spending are expediting their own demise.

This morning, Greenspan is making headlines by finally admitting that the US cannot Pile Debt Upon Debt Upon Debt in perpetuity. In a WSJ Op-Ed, he wrote: “Perceptions of a large U.S. borrowing capacity are misleading… Long-term rate increases can emerge with unexpected suddenness” and that the Big Government Keynesians of the world need a “tectonic shift” in the way that they have been purporting to guard their respective citizenries.

It’s US Open time, and even I will give Mr. Greenspan a golf clap for that. Well done. Listening to the facts and evolving the thought process is always a critical part of any risk manager’s evolution.

But will the guards who have been guarding Ben Bernanke and his Japanese style monetary policy hold the line? Do the guards of Washington’s Economic Officialdom care what the 84-year-old man of the money printing presses is saying this morning?

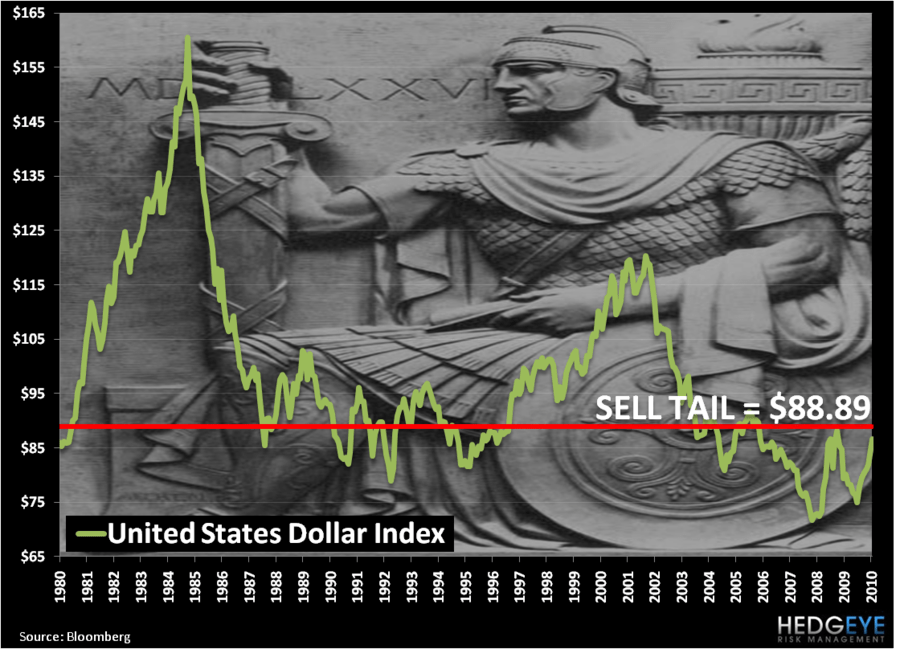

My risk management style isn’t to ask an academic like Larry Summers or Christina Romer in Washington for a leading indicator that might start answering these questions. I ask Mr. Macro Market. What we have seen in the last 3 weeks may not be a “tectonic shift” in the market, but it’s certainly a change on the margin. As Ben Bernanke and Tim Geithner refuse to address the debt and deficit problems in this country, the US Dollar has started to fall.

Since its highs in early June where we shorted it, the US Dollar has all of a sudden lost over -3% of its value. Now any currency trader (which John Maynard Keynes was himself) will quickly remind you that this is partly because the Euro has stopped going down. And I will, in turn, quickly agree – after all, market prices don’t lie; politicians do. All currency moves should be considered relative to each other.

This, importantly, only amplifies my point. As Europe admits that it has a deficit problem, implements austerity measures and, at the same time, the US Administration continues to maintain this ridiculous stance that America’s spending and debt problems are “different”, the Euro actually becomes relatively more credible than the US Dollar. Again, everything is relative between two fiat currencies that are manipulated by Fiat Fools.

Now I am certain that I will get a lot of emails on that statement, because it’s not patriotic to say the Euro is anything but a dog with fleas, but managing risk with your patriotism or politics only gets you in trouble so let’s take a step back and respect that in the last decade the Fiat Fools of US monetary policy have done nothing but debauch the value of the US Dollar. Pull up a 30 year chart of the US Dollar and the story is the same – a long term series of lower-highs and lower-lows.

Why is that? Where have the guards of fiscal conservatism gone? Who will guard the guards of the US currency debasement experiment from here?

Sadly, after seeing Ben Bernanke’s Fed add another $14 BILLION of mortgage backed security toxic waste to America’s liabilities this past week (taking the Fed’s balance sheet up to its highs of $2.35 TRILLION dollars!), there are fewer and fewer guards with credibility left.

My immediate term support and resistance lines for the SP500 are now 1099 and 1135, respectively. We remain short the US Dollar via the UUP.

Best of luck out there today and enjoy your weekend,

KM

Keith R. McCullough

Chief Executive Officer