“I definitely know I’ve got it in me. I’ve just gotta focus on what I can control.”

-Stephen Strasburg

Winners just win. There are plenty of great leaders in this country who prove that where it matters every day. From Washington to Chicago this morning, they’ll be putting their Professional Politicians on mute. This is progress.

The Chicago Blackhawks won the Stanley Cup and in his MLB debut 21-year old Stephen Strasburg struck out 14 batters leading Washington National fans to hope that the future in the Capital could be brighter than the present.

Hope, as we like to say, is not an investment process however. Until we change the said leadership of everything American finance, we are going to be hostage to the gravity of analytical mediocrity.

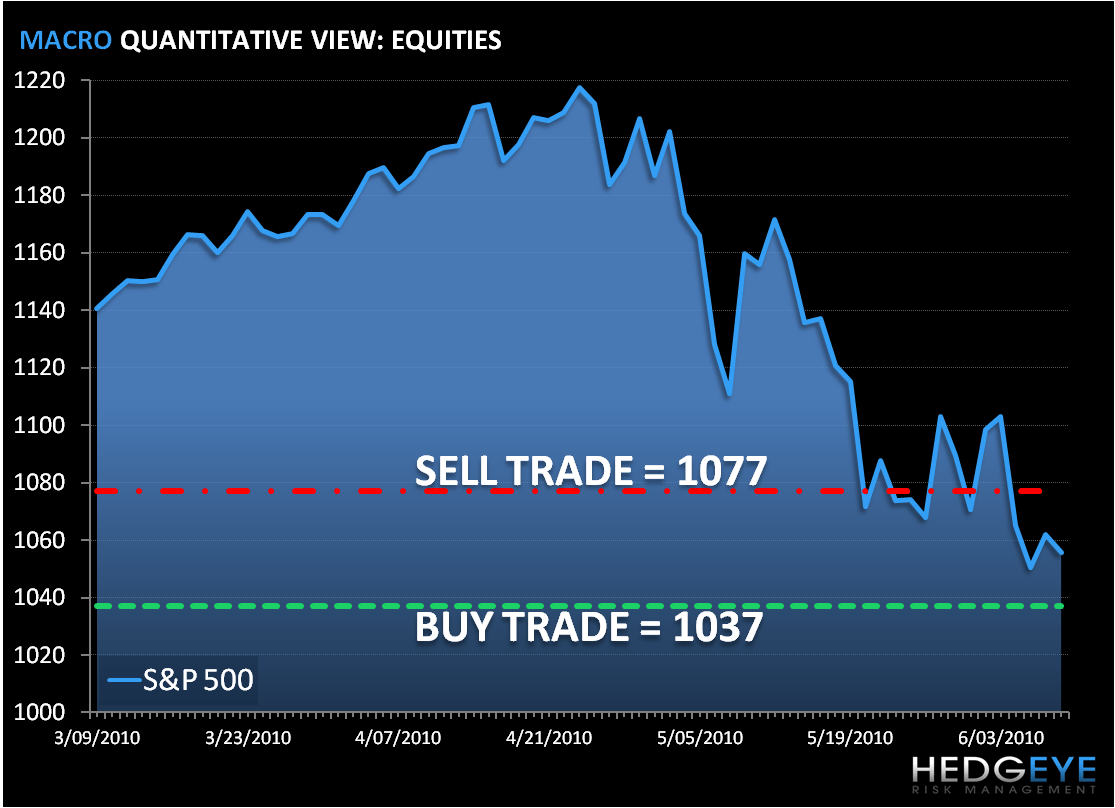

I was on a flight to Los Angeles while Ben Bernanke was testifying yesterday. Between his reckless forecasts and the Manic Monkeys on CNBC taking his word for it, I was left with one option – re-short the SP500 (SPY) on strength.

Not unlike professional athletes, our Hedgeyes believe in putting our market view on a tape for everyone to see, real-time. Our clients love it. Our detractors hate it. This is the New Reality of finance. I think Americans are sick and tired of pretend portfolio managers blowing their capital up in smoke and saying “everyone missed it” every time there is a major loss to reflect upon.

This isn’t to pump my own tires. This is to challenge any of these mouth pieces in the Manic Media to simply put it on the tape. Caution to the Jim Cramers of the world who tell you to buy Bear Stearns or BP obviously - a time stamp on everything you recommend will be held against you every day. There is nowhere to hide.

This is how a practical firm’s interpretation of Transparency and Accountability works. At 12:27PM yesterday we sent a message to our clients that said:

“Re-shorting what we covered profitably. We remain bearish and today's rally reminds me that consensus belief in Bernanke's forecasting ability is not yet Bearish Enough. KM”

You can look at the intraday chart from there and hold me to the score associated with that “call” – whether the call is right or wrong, no matter where I go at 230AM here in California as I write this, there it is…

“I definitely know I’ve got it in me. I’ve just gotta focus on what I can control.”

Think about that winner’s attitude. That’s what we need in this country. Not a bunch of group-thinkers who don’t do their own work and can’t focus on anything other than what the guy focusing on his job security next to him imputes in his forecasts. Do your own work. Have a process. Plan to change it when the plan is not working.

Back to Bernanke…

Here’s the written YouTube version of what he was forecasting yesterday, and we are going to hold him accountable to it:

- Double Dip? - “unlikely, but it can’t be ruled out”

- 2011 GDP forecast? - “3.5-4%, but it’s difficult to say”

- European Debt impact on USA? - “modest impact, but we will monitor it”

Ben, are you kidding me, man? You hold the precious value of the world’s reserve currency in the palm of your hands and everything you forecast is not only infrequently accurate from a risk management perspective, but everything you forecast has a sheepish “but”…

I haven’t had enough sleep, so take my tone for what it is this morning. I’m human too and I am finally at wits end with where the Perceived Wisdoms of Officialdom in this country is taking us. We are headed down a European road to perdition and someone needs to block the road.

Enough of my rant, here are the global macro Risk Manager’s answers to the same questions:

- Double Dip? - Post last week’s employment report and the SP500 losing -13.3% of its value since April 23rd, the probability of a rollover in the US economic cycle has gone up considerably. In probability speak, we’d call a double dip much more likely.

- 2011 GDP forecast? - I can say that it’s not difficult to say that Bernanke’s estimate is way too high.

- European Debt impact on USA? – It’s already marked-to-market so I’ll let Mr. Macro Market speak for himself on this front day-to-day. The answer to the question is obviously that there has been considerable impact and that rather than adhering to a Buy-And-Hope model based on Bernanke’s definition of “monitoring”, we maintain our ZERO percent asset allocation to US Equities in the Hedgeye Asset Allocation Model.

ZERO is the level of respect that Bernanke and the Fiat Fools from Japan to Europe have for the cost of capital. ZERO is the respect you get when you come to the game unprepared and then don’t hold yourself accountable to your performance.

Look on the bright side - if the European version of TARP turns out to be as big a loser as Hank Paulson’s was coming out of the gates, this is what the President of The European Fiat Union has to say about that:

“And if the plan were to prove insufficient, my answer is simple: in this case, we’ll do more.” –Herman Van Rompuy

Obviously Van Rompuy and Bernanke share the same views of accountability. Good thing they didn’t play sports. Ignore these losing ideologies and focus on what you can control this morning. You’ve got it in you.

My immediate term support and resistance levels for the SP500 are now 1037 and 1077, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer