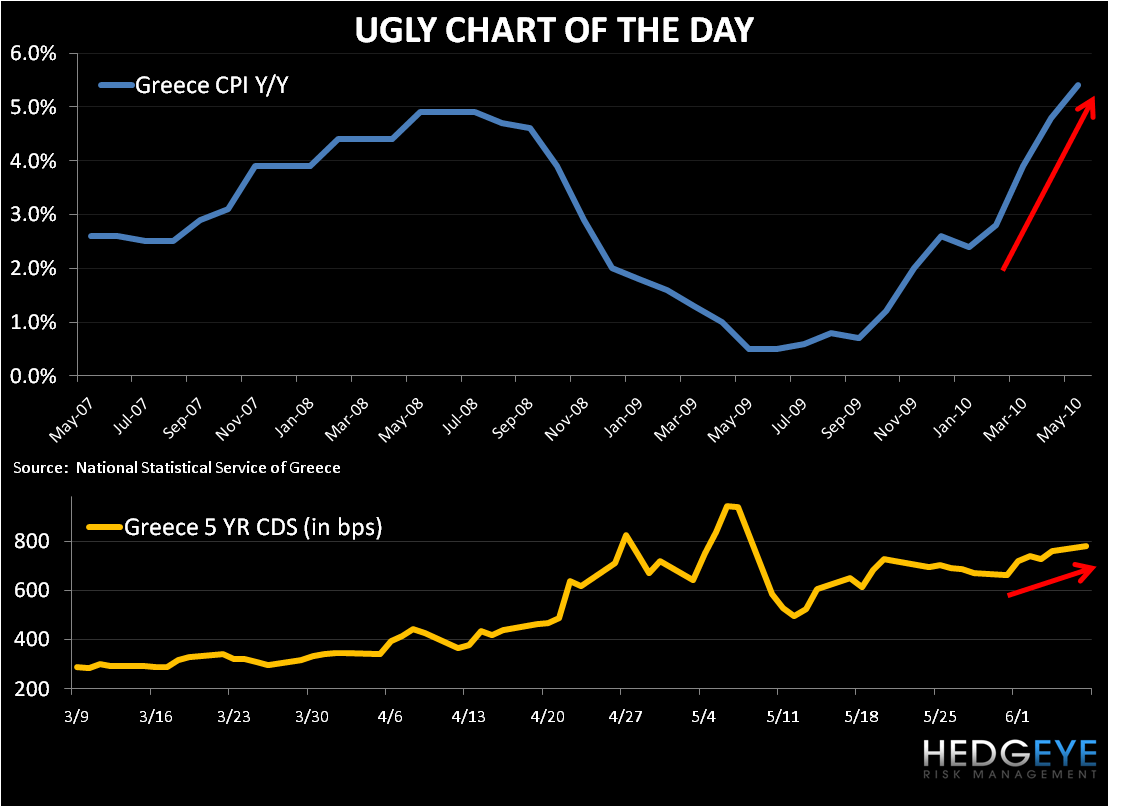

In our Ugly Chart of the Day we refresh both Greece’s Consumer Price Index and 5YR sovereign CDS. Both charts are heading in the wrong direction and both help confirm that neither the European led Greek bailout fund (€110 Billion) nor the €750 Billion loan facility will be a near or long-term solution to all of Europe’s economic ails.

Today, Spanish workers are on strike against the government’s decision to cut wages 5%. While the strikers may make a fine case that they were not responsible for the government’s mismanagement of the budget, someone has to bite the bullet—cutting the bloated wage inflation of many government positions in Spain (and largely across much of Europe) is a sensible move in our opinion.

Germany also picked up the austerity ball, announcing yesterday a €81.6 Billion package of tax increases and spending cuts, including levies on banks, air travel and nuclear-power plants from 2011 to 2014. For Germany, which has much lower levels of total debt and deficit spending as a percentage of GDP, the move underlines the country’s fiscal discipline and aversion to debt.

Matthew Hedrick

Analyst