Which companies are toughening up in this macro environment?

The most bearish data point for the restaurant industry came with Friday’s jobs report. Private payrolls added for the month of May was reported at an anemic 41,000 – the first marginal deceleration since December of 2009. There are a number of factors that drive incremental trends in eating out but, in the current environment, jobs take center stage. The biggest benefit to current top-line trends will be having more consumers collecting a paycheck.

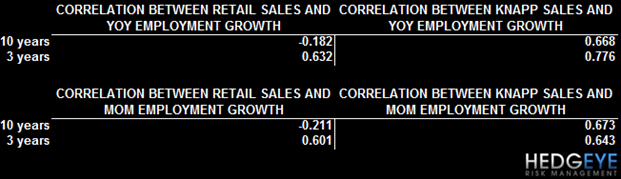

As you can see for the chart below, the casual dining industry is right to be focused on the employment trends. The Knapp figures correlate strongly with employment growth – more strongly, in fact, than retail sales figures do.

Right now it appears there are two key consensus calls in the restaurant sector. The first is that MCD will continue to dominate the QSR space. Second, Bar & Grill is an uncompetitive concept and will not be able to take share.

MCD is a power house and the absolute trends are very impressive. But it looks like expectations are ahead of current trends. The beverage initiative is an important initiative for the company and driving some improvement is current trends. Longer term it complicates operations and will not be a long-term driver of traffic. In May, two-year trends have slowed for MCD around the world. Lastly, GMCR is trading on rumors that MCD is going to buy them. I will say categorically, MCD will never purchase GMCR.

As for the Bar & Grille space, the negative sentiments can be summed up in two thoughts. (1) High-end brands will take significant market share from mass-market brands and (2) Convenience-based brands are more likely to see sales lag in a recovery than destination-oriented brands.

It’s a very difficult and often a losing proposition to pigeon-hole a certain company/brand/stock in a certain classification. In the early stages of the improving top line trends, the consumers with money went to places where they feel comfortable with the food and the service. Over the next 12-month the MACRO environment will be very challenging.

I continue to believe that it’s important to focus on those companies that are being proactive and changing the variable cost structure. Those that can create leaner, meaner cost structures will be better positioned to mitigate any margin erosion.

EAT is one name that is pursuing a proactive strategy and remains a core focus name.

Howard Penney

Managing Director