This commentary was written by Dr. Daniel Thornton of D.L. Thornton Economics.

Greg Ip did an historical analysis of the Fed’s monetary policy and its effectiveness on the front page of the Wall Street Journal on January 16, titled “Weaker Fed Loses Grip on the Economy.” Unfortunately, his analysis is incorrect in a number of important respects. This essay explains why.

In a subsection of his analysis labeled “Modern times,” he correctly noted John Maynard Keynes argued that a situation could arise were firms could spend too little to keep everyone employed. He went on to suggest that during the quarter century following the passage of The Employment Act of 1946, monetary and fiscal policy were used to regulate the economy and that monetary policy and its effectiveness was “textbook”:

|

“…rapid economic growth and falling unemployment yielded rising inflation. The Fed responded by raising interest rates, reducing investment in building, equipment and houses. The economy would slide into recession, and inflation would fall. The Fed then lowered interest rates, investment would recover and growth would resume.” —WSJ, January 16, 2020, page A8. |

This is a nice rendition of the textbook story. Unfortunately, it’s not true.

For one thing, the Fed’s discount rate was a ceiling for the federal funds rate until the mid-to-late 1960s. When interest rates were rising the federal funds wouldn’t increase above the discount rate as other short-term interest rates continued to rise. The discount rate is set by the Board of Governors and not the Fed’s policy making body, the Federal Open Market Committee (FOMC). When short-term rates would go sufficiently above the discount rate, the Board would increase the discount rate. Indeed, my extensive research on the discount rate shows the discount rate has always followed rather than led market interest rates and changes in the discount rate did not signal a change in policy.1/

Moreover, Fed Chairman William McChesney Martin adopted a “leaning against the wind” policy, which meant the Fed would buy or sell Treasuries in order to stabilize inflation. From then until the late 1980s when the FOMC began using the federal funds rate as its policy instrument (see Greenspan’s Conundrum), the FOMC’s operating directive instructed the “Trading Desk” of the Federal Reserve Bank of New York to implement daily open market operations based on the “ease or tightness” in the money market (the market for short-term securities). The direction (purchase or sale) and magnitude of the operation was determined by a variety of factors and not just the behavior of the federal funds rate.

Furthermore, the Martin Fed adopted the “bills only policy,” a policy of only conducting open market operations in short-term Treasury bills in order to minimize the effect of open market operations on longer-term interest rates. The Fed deviated from this policy for a short period beginning in 1961. Specifically, the Martin Fed engaged in what was called “operation twist.” Specifically, the Fed purchased long-term Treasuries and simultaneously sold an equivalent amount of short-term securities in an attempt to reduce long-term rates, i.e., twist (flatten) the yield curve.

However, research showed the policy to be ineffective. Consequently, the Fed returned to conducting open market operations with only short-term Treasuries.2/ The Fed generally maintained this procedure until the Bernanke Fed attempted to move long-term rates by engaging in large-scale purchases of long-term Treasuries, mortgage-backed securities and agency debt, commonly known as quantitative easing (QE).

Then there is the problem that Keynesians (which comprised nearly all macroeconomic economists during this period) believed that monetary policy was ineffective. Surveys of businesses and empirical research indicated interest rates had little effect on spending. Keynesian’s stabilization policy focused on deficit spending to control “aggregate demand” and economic growth. Keynesians didn’t change their mind about the effectiveness of monetary policy until the Volcker Fed ended the Great Inflation in the early 1980s.

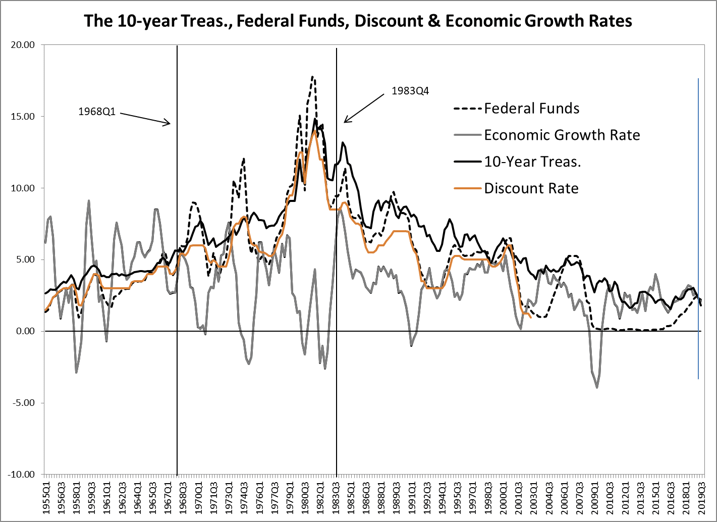

Mr. Ip’s textbook story that the Fed increased or decreased output growth by lowering or raising interest rates is not true. The figure above shows the 10-year Treasury and federal funds rates, the growth rate of real GDP and the Fed’s discount rate (discontinued in 2003) from 1955Q1 to 2019Q3. The figure shows the Treasury rate and the federal funds rate moved lower when output growth declined and increased when output growth increased before the period of high inflation, from about 1968Q1 to 1983Q4. This is hardly compelling evidence of effective counter-cyclical monetary policy Mr. Ip suggested happened during this period.

Indeed, classical economists saw this behavior of long-term and short-term interest rates as normal and expected. They argued during periods of slack economic activity, investment in real capital would decline reducing the demand for credit, which would cause interest rates to decline. The decline in the demand for long-term credit would produce an increase in the quantity of credit supplied to the short-term markets, so short-term rates would decline more than long-term rates. Precisely what the figure shows happened during this period.

Besides, as I noted previously, the federal funds rate was essentially capped by the discount rate during this period, so the federal funds rate increased slower during the latter part of the period than the Treasury rate. The figure also shows that the federal funds rate started to go consistently above the discount rate by the mid-to-late 1960s because large banks began using federal funds to finance part of their lending (see Meulendyke 1998, p. 38, second full paragraph (here) for a fuller explanation).

Mr. Ip’s “textbook” story appears to be true during the period of high inflation.

However, the behavior of interest rates (including the federal funds rate) during this period was due to large swings in inflation and inflation expectations, not to the FOMC’s monetary policy.

After 1983Q4, interest rates and output growth were again positively correlated as classical economists suggested. However, the Fed began using the federal funds rate as its policy instrument in the late 1980s. The federal funds rate tends to fall more relative to the 10-year Treasury rate than it did before because the FOMC was more aggressive in reducing the federal funds rate than the market would have been. Again, this is hardly compelling evidence of the effectiveness of the FOMC’s monetary policy.

Mr. Ip should also know better than to say “a central bank can always raise rates to slow growth in pursuit of lower inflation.” The FOMC has been able to control the overnight federal funds rate well since the late 1990s and very well after the FOMC began announcing the targeted rate in June 1999. However, there is considerable dispute in the profession about the extent to which the FOMC’s control of the federal funds rate spills over to interest rates that matter for spending decisions. The evidence is weak that changes in the federal funds rate have had an economically important effect on these rates.

I like it when well-known and respected journalists, like Mr. Ip, write about economics and, in particular, about the Fed and monetary policy.

However, they really need to do their homework to make sure they got it right.

EDITOR'S NOTE

This is a Hedgeye Guest Contributor piece written by Dr. Daniel Thornton. During his 33-year career at the St. Louis Fed, Thornton served as vice president and economic advisor. He currently runs D.L. Thornton Economics, an economic research consultancy. This piece does not necessarily reflect the opinion of Hedgeye.

- 1/ See: “The Discount Rate and Market Interest Rates: Theory and Evidence,” Federal Reserve Bank of St. Louis Review, August/September 1986, 68(7), 5-21; “Why Do T-Bill Rates React to Discount Rate Changes?” Journal of Money, Credit and Banking, November 1994, 26(4), 839-50; “The Information Content of Discount Rate Announcements: What is Behind the Announcement Effect?” Journal of Banking and Finance, January 1998, 22(1), 83-108; “Lifting the Veil of Secrecy from Monetary Policy: Evidence from the Fed’s Early Discount Rate Policy,” Journal of Money, Credit and Banking, May 2000, 32(2), 155-67.

- 2/ Empirical analyses of the effectiveness of operation twist by Modigliani and Sutch (1966) and (1967), American Economic Review, 56, 178-97, and Journal of Political Economy, 75, 569-89, respectively, found operation twist to be ineffective. Revisionist work by Swanson here used an event-study methodology and found small effects small effects of operation-twist announcements on the 10-year Treasury rate ranging 1 to -8 basis points. However, I have shown here that event study results can only be considered evidence if announcement effects can be attributed to the announcement, not other information, and if the announcement effect is statistically significantly, i.e., different from what would have occurred had there not been an announcement. Swanson’s operation-twist announcement effects do not meet this standard. Indeed, when I applied this standard to the 52 quantitative easing (QE) announcement used in the QE event-study literature, I found that only one QE announcement satisfied this requirement—the QE announcement the Fed made at the March 18, 2009 Fed meeting. However, the effect was short lived. More than half of the 50 basis point announcement effect on the 10-year Treasury rate was offset in one week and it was completely offset in a month. By June 24, 2009, Fed meeting the 10-year Treasury rate was 121 basis points higher than it was on March 17, 2009, the day before the announcement.