Here are the property specifics driving the 93% y-o-y increase in May Macau gaming revenues.

As we wrote about mid-month, May was likely to be a blowout month – and it was, up 93%. Yes, the casinos held well on the VIP side, but even if the hold percentage was normal in May 2009 and 2010 and if we adjust for higher levels of direct play, total Macau gaming revenues would still have increased 71%. While VIP was again the standout – up 121% - Mass did increase 44%, owing in part to a strong Golden Week. We estimate that direct play accounted for 8% of RC turnover in May vs 7% last year. A small part of the explanation for the explosion in VIP growth can also be attributed to last May's weakish hold (2.6%) and this May's relatively high hold of 3%. Assuming both period held normally at 2.85%, VIP revenues would have still growth 86% y-o-y.

In terms of market share, Wynn and MPEL were the clear winners while LVS showed the biggest sequential drop. Wynn obviously benefited from a full month of Encore while MPEL was able to grow its market share sequentially in both Mass and VIP. LVS lost share in both VIP and Mass. We remain concerned with the continued share losses by LVS but until market growth stops growing 60-95%, few are likely to care.

Y-o-Y Table Revenue Observations

LVS table revenues increased 82%, with growth coming from a 140% increase in VIP revenues (hold was very low last year) but only a 21% increase in Mass revenues.

- Sands grew 73%, driven by a 132% increase in VIP revenues and an 15% increase in Mass revenues

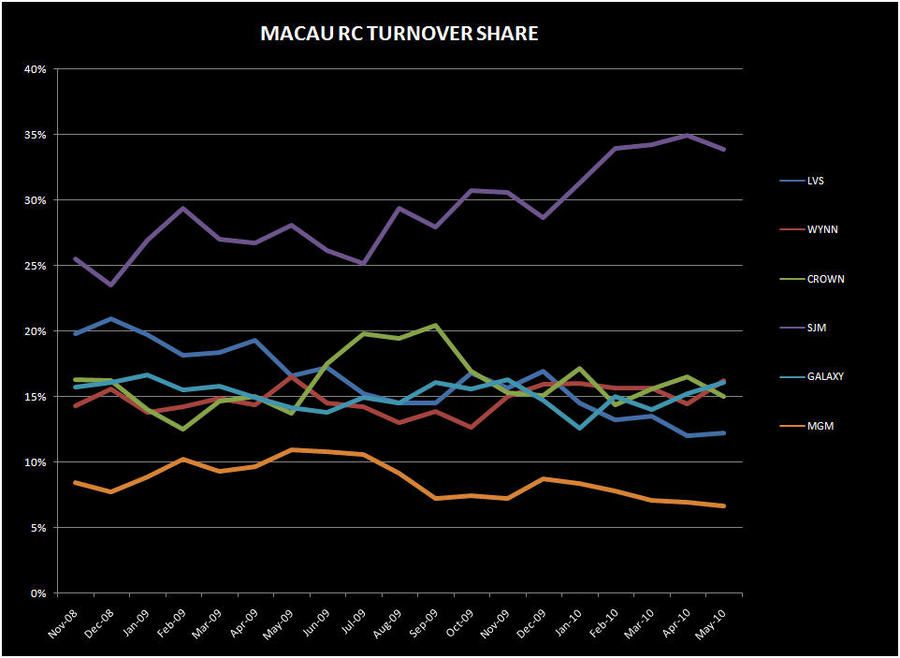

- Junket RC increased 77%.

- Hold looks high - roughly 3.1% compared with low hold last May of roughly 2.25%, assuming 12% direct play levels in both period.

- Venetian was up 61%, driven by a 95% increase in VIP revenues and a 24% increase in Mass revenues

- Junket RC decreased 10% y-o-y, however, hold more than made up the difference. Assuming 20% direct VIP play volume, we estimate that hold for May was 3.7%. Last May, assuming 16% direct play, the hold percentage was only 1.7%.

- Four Seasons was up 342% y-o-y entirely driven by 703% VIP growth and Mass growing a relatively small 30%

- Junket VIP RC increased 446% to $989MM. If we assume 35% direct VIP play then overall VIP turnover likely had a record month of approximately $1.5BN

Wynn Macau table revenues were up 78%, primarily driven by a 92% increase in VIP revenues and a 23% increase in Mass revenues.

- Junket RC volumes increased of 81%

- Assuming that direct play percentages increased by 20%, hold was similar to last May

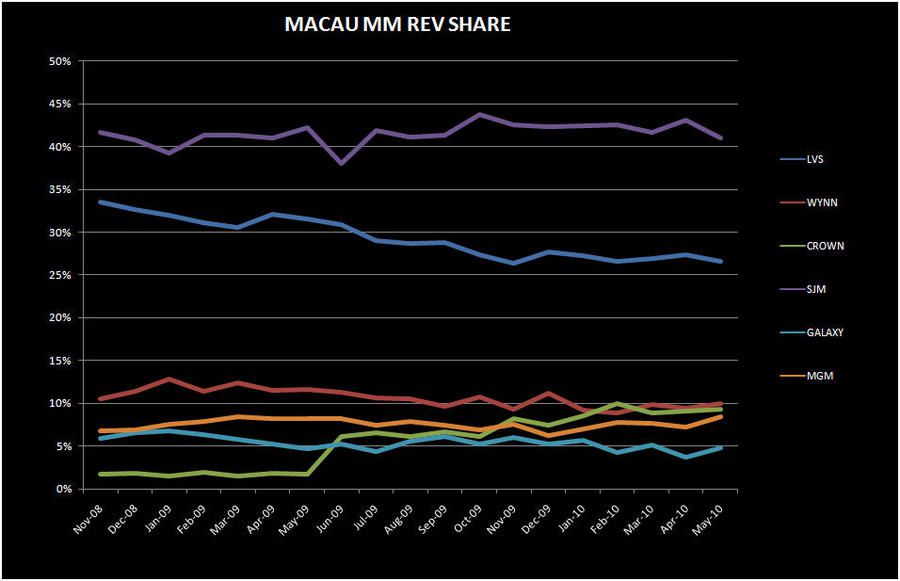

MPEL table revenues grew 159% with the growth fueled by 675% growth in Mass and 131% growth in VIP

- Altira was up 18%, due to an 18% increase in VIP revenues and a 19% increase in in Mass

- VIP RC was down 4%, but hold comparisons were favorable. For the second consecutive month, Altira seems to have held high at 3.5%, compared to normal hold of 2.8% last May

- CoD table revenue increased 40% sequentially, due to a 54% increase in VIP win and a 9% increase in Mass revenues

- Mass was $37MM

- Junket VIP RC increased 12% sequentially

- If we assume 18% direct play at CoD (in line with what MPEL said on their earnings call), then total VIP RC would be $4.5BN. However, hold in May hold appears weak at only 2.5%

SJM continued to grow above market growth rates for the 9th consecutive month, with table revenues up 106%

- Mass was up 40% and VIP was up 154%

- Junket RC volumes increased 123%

Galaxy table revenue was up 82%, driven by a 86% increase in VIP win and Mass increase of 47%.

- Starworld's table revenue was up 159%, driven by 165% growth in VIP revenues and 44% growth in Mass

MGM table revenue was up 83%.

- Mass revenue growth was 44%, while VIP grew 103%

- VIP RC grew 85%

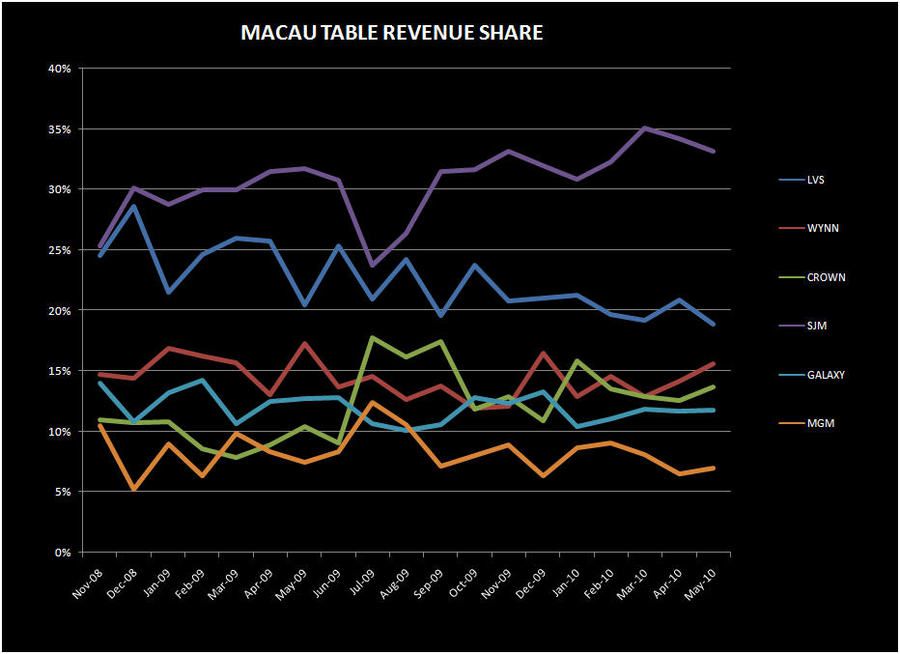

Table Market Share

LVS table share increased 200bps sequentially to 18.9% with most of the share loss coming from VIP. Despite impressive y-o-y results, May 2010 marked LVS's lowest table share since March 2008.

- LVS's share of VIP revenues decreased to 16.5% from 18.7% in April. LVS's share of Junket RC increased 20 bps to 12.2% from the lows of last month

- Mass share decreased by 80 bps to 26.6%

- Sands market share dipped to its lowest levels since we've been tracking the data (and likely an all time low) of 6.3% down 60bps sequentially. Sands lost share across both VIP and Mass.

- Venetian lost 60bps to 9.9% sequentially

- Venetian lost share across both Mass and VIP

- Junket RC fell 22bps to lows of 5.3% - Venetian's lowest share since opening.

- FS share decreased 85bps to 2.7% off of April's record share of 3.5%.

- After SJM, LVS still commanded the second highest share of the overall market (including slots) of 19.4%, followed by Wynn at 15.7%.

WYNN's share (including slots) increased to 15.7% from 14.4% in April.

- VIP revenue share increase 155bps to 17.3% sequentially while Mass revenue share increased 50bps to 9.9%

- Wynn's VIP share is second only to SJM at 30.8%, followed by LVS at 16.5%

- Wynn Junket RC share increased 177bps to 16.2%, its highest share since last May

Crown's market share increased by 110bps to 13.7% in May.

- CoD's bounced back to 7.5% and gained back what it lost in April due to low hold

- Altira's share increased to 6.3% from 6.2% in April. However, Junket RC share decreased by 110bps to 7.1% which is the lowest share Altira has garnered since July 2007

SJM's share (including slots) slipped by 110 bps to 32.3%.

- SJM Mass share decreased by 210bps to 41.1% sequentially, while VIP share slipped 40bps

Galaxy's share was flat at 11.7%, although Mass share increased while VIP share slipped a little

- Starworld's market share was decreased 30bps sequentially to 9.2%, due to a 90bps hold driven decline in VIP share which was somewhat offset by a gain of 60bps in Mass

- Junket RC share increased 20 bps sequentially to 13.1%

MGM's share increased by 50bps (including slots) to 7.2%.

- MGM's share gain can be attributed to a 1.2% sequential increase in Mass share to 8.5%, its best share since August 2008

- VIP share increased 20 bps to 6.5% despite a 30bps decline in Junket RC

Slot market commentary

- Slot win grew 29% y-o-y to $89MM

- LVS's slot win grew by 29% y-o-y to $29MM

- Wynn slot revenues increased by 11% y-o-y to $17MM

- Melco's slot win grew 118% y-o-y to $19MM

- MGM's slot win grew 16% y-o-y to $11MM

- SJM's slot win decreased 1% to $12MM

- Galaxy's slot win grew 25% to $2MM